(Bloomberg Opinion) -- If you want to see how the Permian basin’s pipeline problems are hitting producers, where better to start than Pioneer Natural Resources Co.? Not only is it one of the largest E&P companies operating there; it’s also shedding other assets to make itself a Permian pure-play.

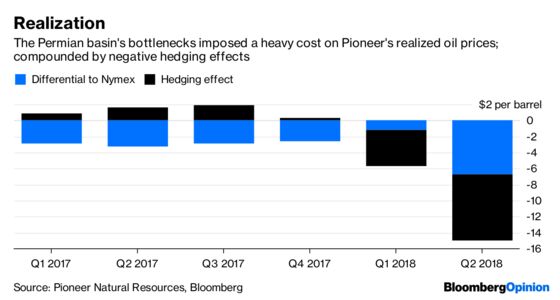

That’s gone from being a badge of honor to a drawback in recent months, and Pioneer’s second-quarter operating update, released Tuesday, showed why. Pioneer reported a realized price for its oil of $61.20 a barrel, nearly $7 lower than the average Nymex oil futures price for the quarter. A year before, that differential was just $3.28, showing just how much of a bite Permian logistical constraints are taking out of Pioneer’s revenue. Using the midpoint of Pioneer’s guidance, the spread in the second quarter cost Pioneer about $108 million of potential revenue.

Compounding this was the effect of hedging. Tim Dove, Pioneer’s CEO, talked about this on the first-quarter earnings call in May, noting that a heavy hedging program would blunt the benefit of higher oil prices this year. Hedging effects took off almost $4.50 a barrel in the first quarter, but that blew out to more than $8 in the second.

The stock fell slightly on the news Tuesday, largely because it has fallen about 12 percent already since concerns about the Permian hit in mid-May.

And there are reasons for optimism looking ahead. Hedges aside, Pioneer is actually better positioned than many of its peers in terms of contracted pipeline capacity from west Texas to the Gulf Coast, where pricing is better. It also ships a lot of its associated natural gas production west toward California, which mitigates some of the local glut in that fuel, too.

And on hedging, the share of oil production covered by Pioneer’s program drops significantly next year, with only around 7 percent locked in as of the end of March, versus almost 80 percent for 2018’s output, according to data compiled by Bloomberg New Energy Finance.

Indeed, relief may come a little sooner than that. Paul Sankey, analyst at Mizuho Securities, notes Pioneer contracts for its sales to refineries and for exports about two months ahead of expected deliveries. Given the recent narrowing of the spread between domestic West Texas Intermediate crude oil prices and the international Brent benchmark, that should mean stronger realizations coming through in the current quarter.

One thing Tuesday’s figures hammer home, though, is the shadow the Permian will cast over the E&P earnings season just beginning.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.