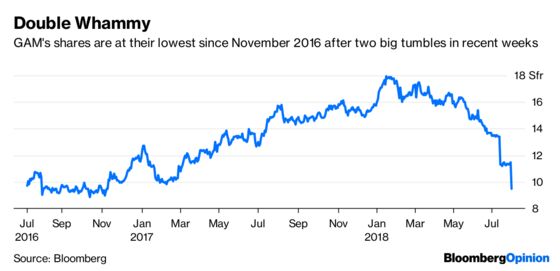

(Bloomberg Opinion) -- It’s been a terrible couple of weeks for GAM Holding AG. But the outlook for the rest of the year looks even bleaker for the Swiss asset manager — and its investors.

Earlier this month, GAM said it was writing off $59 million of goodwill from its acquisition of hedge fund Cantab Capital Partners, for which it paid $217 million in October 2017. On Tuesday, it announced the suspension of Tim Haywood, the portfolio manager of its flagship absolute return bond fund, after investigating “some of his risk management procedures and his record-keeping.” Clients are likely to withdraw money as a result, GAM said.

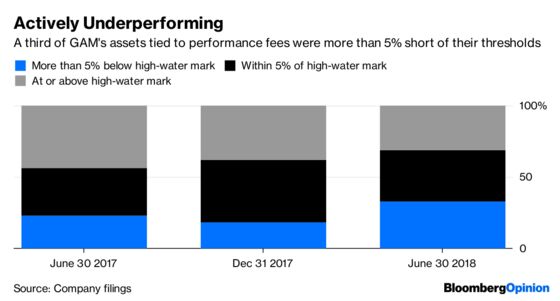

But it’s the dismal outlook that GAM sees for markets and its own performance in the coming months that will make investors and clients even more twitchy. In its first-half results published Tuesday, the Swiss firm said one-third of its assets that are eligible for performance fees — worth a total of 15.5 billion francs ($15.5 billion) — failed to get within 5 percent of those preset thresholds. That’s up from 18 percent at the end of 2017, and from 23 percent in the middle of last year.

GAM blamed “volatile and directionless market conditions” for its lack of returns. Net inflows of 2.6 billion Swiss francs in the first six months of the year were offset by a 3.2 billion Swiss franc drop in investment performance. When you chuck in 600 million Swiss francs of foreign exchange moves, the investment management division’s assets were unchanged at 84.4 billion Swiss francs.

Moreover, that environment is “likely to continue in the second half of this year, which may affect clients’ risk appetite and the group’s flows,” the firm said. In other words, there’s little prospect of the fund making money, and customers will probably withdraw funds. That’s not a good combination.

GAM says it “continues to see opportunities for high-performing active asset managers to capture growing investor demand for strategies that offer true diversification versus traditional asset classes and broad market trends” — by which it means electronic and passive funds.

Well, what else can it say? It’s hard to capture any growing demand when your performance is this bad and you’re having to get rid of one of your top managers. Investors gave their own response by pushing the shares down as much as 20 percent on Tuesday morning.

If the fund manager’s clients come to a similar conclusion, there could be worse times ahead for GAM.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.