European Bonds Need to Wake Up and Smell the Sake

(Bloomberg Opinion) -- Europe needs to wake up and smell the sake.

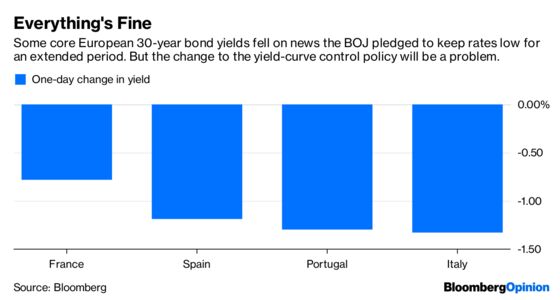

Some of the continent’s longer government bonds rallied on Tuesday as the fear that the Bank of Japan might reduce its QE stimulus proved misguided. But the relief really shouldn’t last.

True, the BOJ extended its monetary easing in its latest policy decision, including its highly successful yield curve control policy.

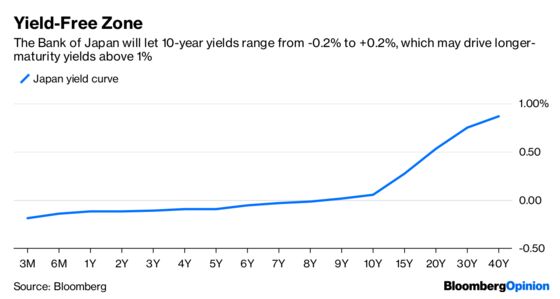

However, at the press conference following the decision Governor Haruhiko Kuroda announced an important tweak to the bank’s yield-curve control policy. Instead of a 10 basis-point cap on 10-year Japanese Government Bonds, officials will introduce a range, and allow yields to drift as much as 20 basis points above or below zero.

The point is to breathe volatility back into the world’s second-largest bond market. Trading volumes have ground to a halt as the BOJ’s yield-curve control proved to be just a little bit too controlling. This wider band may not sound like much of a difference, but the change will be magnified in ultra-long maturities, which are not subject to the policy.

This should make JGBs more attractive to domestic investors — who could then become less enamored of investing abroad. Core European bonds have been a favorite for some time, as on a currency-hedged basis they offer higher yields than what’s available from Japanese securities. The greater the yield pickup, the greater the weighting to foreign securities. That dynamic is about to be tested.

Japanese bond yields fell as the central bank introduced forward guidance, and a commitment to keep interest rates “very low for a while.” But given the change to the yield curve control policy, at some stage today’s rally will unwind. That’s likely to have a knock-on effect onto Europe.

A pickup in 10-year Japanese bond yields will likely push ultra-long JGB yields even higher. This curve steepening will encourage Japanese life insurance and pension funds — which are desperate for higher returns — to bolster their domestic allocations rather than look abroad for higher (but riskier) returns. As things stand now, with 30-year JGBs only yielding 0.75 percent, it is slim pickings at home. But something above 1 percent could well alter their calculations.

Earlier in July, French ultra-long yields dropped on hope the European Central Bank might introduce a version of “Operation Twist”

— where reinvestments of bonds maturing in its QE program might be skewed towards 30-year securities. However, ECB President Mario Draghi quashed this hope at the press conference following the July 26 policy decision by announcing that officials didn’t even discuss the time table for making changes to the redemption policy. The French yield curve has now unwound the flattening move.

With the Bank of Japan widening its yield curve control range, European ultra-long yields are facing another piece of bad news. But traders seem not to have noticed. If Japanese yields start to move higher, Europe will feel the pressure.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.