(Bloomberg Opinion) -- Even the most sorry tale can have something like a happy ending.

That looks to be the case with BHP Billiton Ltd.’s misbegotten foray into onshore U.S. oil and gas. With the announcement Friday that the company will sell its assets in the Eagle Ford, Permian and Haynesville basins to BP Plc for $10.5 billion, the company’s U.S. oil unit will be sticking to the deep seas.

The price looks better than many had been expecting. At the time Elliott Management Corp. started pushing for a divestment of the assets in April last year, brokers valued them at an average of $6.5 billion. First-round bids for the business from BP, Chevron Corp. and Royal Dutch Shell Plc had come in between $7 billion and $9 billion, people familiar with the matter told Kiel Porter and Dinesh Nair of Bloomberg News last month.

By BHP’s own numbers, net operating assets in the three basins were worth about $9.5 billion at the end of December — although the gross value was pegged Friday at $10.9 billion, or $13.9 billion including goodwill.

Of course, things have changed over the past 15 months. The Permian is currently the hottest oil patch on the planet, with output up by almost half since last April to 3.5 million barrels a day — about a third of the total output from Saudi Arabia or Russia, and considerably more than the United Arab Emirates or Kuwait — and the number of rigs exploring for more rising by about 40 percent.

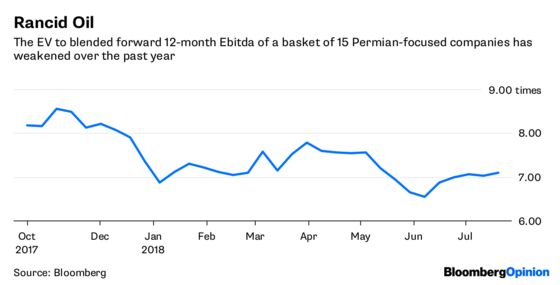

Even so, those numbers have yet to translate into more earnings, or even significantly higher valuations. The median Ebitda multiple of Permian-exposed U.S. oil producers fell to 7.1 last week from 7.9 six months ago, according to a Bloomberg-compiled market-weighted basket of 15 companies. That reflects pipeline constraints that have kept Permian production locked up onshore and trading at a sharp discount to benchmark West Texas Intermediate at Cushing, Oklahoma.

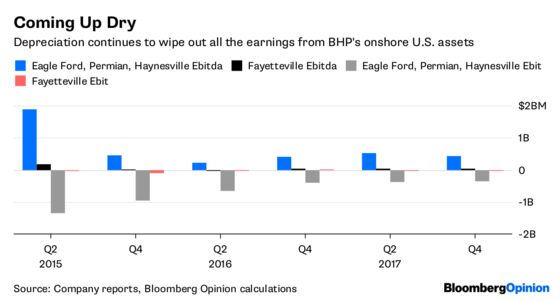

The cap on output is reflected in the financial numbers, too. The businesses BP is buying haven’t turned a profit in years, and still lost $356 million in underlying Ebit in the six months through December. Excluding depreciation and amortization those numbers look better — but depreciation is a real cost for fast-depleting shale plays, and can’t be wiped out by accounting trickery if you buy an asset close to book value.

The advantages to BP are longer-term. The company skulked away from the Permian by selling its assets to Apache Corp. in the wake of the Deepwater Horizon oil spill in 2010. With pipeline capacity from the region set to improve next year and in 2020, there’s a decent chance too that the current mismatch between production strength and valuation weakness will close. In terms of acreage, that’s already happening: The price is a discount to the $12.5 billion that UBS AG estimates the assets are worth, based on the value of recent transactions.

BHP’s foray into the U.S. onshore shale market was a disaster that opened up a $20 billion hole of writedowns, losses and wasted capital spending. Remaining disgruntlement with that outcome will be considerably muted by the promise from Chief Executive Officer Andrew Mackenzie to return the proceeds of the sale rather than reinvest them. Whether that’s enough to placate Elliott remains to be seen.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.