(Bloomberg Opinion) -- If the answer is a bond tantrum, then we’re probably not going to get asked the question twice.

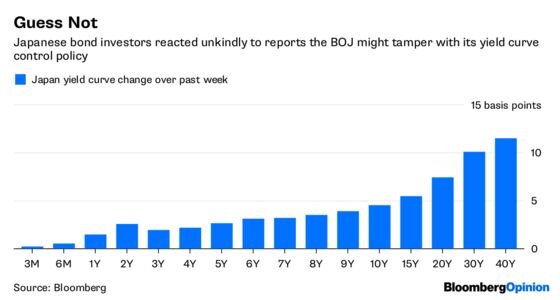

Several press reports over the weekend suggested the Bank of Japan might, at its next policy meeting, debate lifting the yield curve control cap it has imposed on 10-year bond yields. Currently, officials aim to keep yields “around zero” — which as a practical matter means it only takes action if they rise above 0.1 percent. Governor Haruhiko Kuroda said he knew of no basis for these reports.

This policy has been around since September 2016, and has been hugely successful. So why change it?

The answer lies in concerns about transmission of monetary policy. Perhaps some officials on the BOJ’s nine-member policy committee believe that raising the cap would steepen the yield curve, thereby boosting bank profitability and spurring loan growth. Surely this is a desirable goal, given that inflation has utterly failed to embed itself into the Japanese economy.

But this approach is a massive risk. It would take a long time for a change to feed through to inflation, and meanwhile the near-term impact would only be to drive bond yields higher just as inflation is cooling. A nasty side effect would be that it would encourage domestic investors to buy more Japanese securities. This would drive the yen higher, which would destroy the impact of the last 10 years of stimulus.

Bloomberg Economics’ Yuki Masujima said these reports seem to be a trial balloon. If they were, investors gave a clear answer. The yield curve steepened by about than 10 basis points, which is a huge move — Japanese government bonds rarely move more than a basis point during a day’s trading. Hedging by primary dealers ahead of a 400 billion yen ($3.6 billion) 40-year JGB auction on Tuesday probably exacerbated the reaction.

The Bank of Japan stepped in on Monday by offering to buy all 10-year bonds tendered by the market at 0.11 percent. This had the desired result of capping yields, and in fact the central bank didn’t wind up having to buy anything. This illustrates the power of the policy — it’s a big stick, and since it was introduced the BOJ has only had to buy bonds once (it’s issued threats on four separate occasions). Officials have kept a lid on yields for so long that other central banks can only look on with envy.

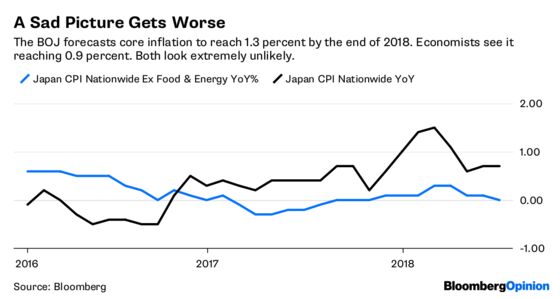

So the BOJ is not going to sway from this policy anytime soon. The brutal fact is that it is nowhere near achieving its goal of inflation above 2 percent, and in fact, economists’ forecasts for price gains are far below what the BOJ is currently expecting.

It’s a fair point that something more needs to be done. And it makes some sense that this idea is getting kicked around. But the answer to Japan’s economic problems should not involve the one policy that’s really working.

A better solution would be for officials to pin down yields on shorter maturities, most likely five years, just as they have 10-year yields. Only then should officials risk allowing longer yields to rise. There will surely be a comprehensive review, and there could be other measures that merit scrutiny, but whatever officials decide upon, they shouldn’t do anything that would weaken the power of the current yield curve control program.

Investors have endured a number of these little scares about the policy’s force, and the result has always been that the BOJ has the final word. It’s just like the hiccups with the bond buying program — any market panic about a reduction in purchases soon dissipates once everyone remembers that the central bank won’t let yields rise.

Traders are always going to try to smoke out the next move by central bank officials. They should bear in mind that Kuroda and his colleagues aren’t going to be rushed.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.