(Bloomberg Opinion) -- Rakesh Kapoor likes to play a long game. When it comes to consumer healthcare, the Reckitt Benckiser Group Plc boss’s patience may be about to pay off.

GlaxoSmithKline Plc is weighing a spinoff of its consumer healthcare arm, according to the Financial Times. In a statement on Monday, the drugmaker didn’t exactly rule the idea out, saying its “No. 1 priority” is improving the performance of its pharma operation. Its current three-prong structure “is subject to each business continuing to perform competitively and having access to capital.” So the door is open, at least in the longer term.

For Kapoor, the maker of Panadol painkillers would be just the medicine he needs after walking away from buying a similar business that Pfizer Inc. had put up for sale.

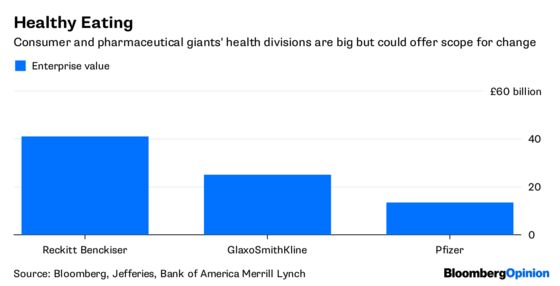

The snag is that the GSK division is big, with an enterprise value of about 25 billion pounds ($33 billion), according to analysts at Bank of America Merrill Lynch. It might be a stretch for Reckitt to buy it outright, particularly after its acquisition of infant formula maker Mead Johnson in 2017 ratcheted up borrowings.

That the Pfizer business came onto the market so soon after the Mead Johnson purchase was one of the reasons that Reckitt walked away. But the integration is now more advanced, with Mead recently showing some signs of improvement in performance. Reckitt still throws off cash, so borrowings should also be coming down too.

Kapoor can afford to wait.

In the meantime, he could offload some of Reckitt’s hygiene and home unit, which includes brands such as Vanish and Airwick. While suffering from lower growth, the cash generative operation could appeal to a private equity buyer. It has an enterprise value of 16 billion pounds, according to Martin Deboo, an analyst at Jefferies. That would go some way toward offsetting the cost of acquiring the Glaxo unit.

Given the size, he would probably have to structure the deal as a merger of Reckitt’s consumer and health business with that of GSK. If executed carefully, this could eventually put the combined company in a good position to snap up other consumer healthcare divisions being offloaded by the likes of Pfizer.

With growth in their traditional strongholds sputtering, consumer goods giants like Reckitt and Nestle SA are trying to ramp up their offerings of health products. For Kapoor, who sprinkled the Reckitt magic dust on brands such as Nurofen, there’s an opportunity to perform some radical surgery in the industry. If he doesn’t, someone else such as an ambitious private equity group or even Nestle CEO Mark Schneider might.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2018 Bloomberg L.P.