Maybe the Future of Fund Management Isn’t So Bleak

(Bloomberg Opinion) -- Another week, and another consultancy firm is warning that the asset management industry faces a crisis in the coming years. I’m starting to wonder whether the apocalyptic warnings about the future of money managers underestimate the plasticity of the world of investment.

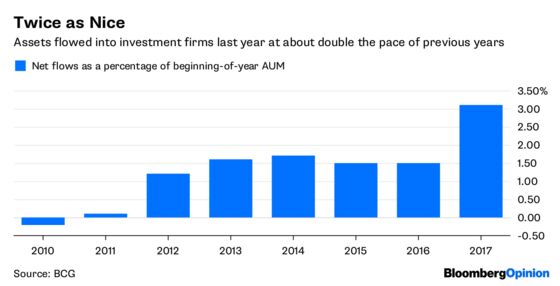

The global fund management industry enjoyed record net inflows last year, with total assets increasing by 12 percent to more than $79 trillion, according to a report released this week by the Boston Consulting Group. That could be a last hurrah, as the report argues. Or it could be evidence that firms are adapting well to a changing landscape dominated by the rise of passive strategies and increased scrutiny from market regulators.

Rising stock markets have encouraged individual investors to add to their holdings, with the retail component of global assets under management increasing to 39 percent last year from 37.5 percent in 2016, according to the report. The higher fees typically levied on retail accounts helped to defend the industry’s profitability.

The chart above shows those profits have been remarkably stable in recent years. But BCG, which surveyed 165 asset managers with $48 trillion of funds, warns that a decline in stock markets could reverse those inflows, triggering a drop in profitability. “At some point, a significant market reversal is likely, given the long period of gains that investors have enjoyed,” the firm says.

For sure, equities have already put in their weakest start to the year since 2011. The MSCI World Index is up by less than 2 percent, making it unlikely to match last year’s gain of 20 percent. But if BCG really has faith in its ability to time a stock market downturn, it should get out of consulting and into the investment business.

In the past five years, BCG estimates asset management firms have delivered total shareholder returns of 12.2 percent, handily beating the 9.5 percent delivered by companies in the MSCI World Index. That level of outperformance may prove unsustainable. But even if the squeeze on fees persists, so too will the trends that have driven the surge in assets under management.

The growth of an affluent middle class in emerging countries, especially China, combined with the shift toward defined-contribution retirement accounts, where individuals are required to manage their savings, should continue to swell the industry’s collective coffers.

After growing by more than a fifth last year, China is now the world’s fourth-biggest fund management market, up from eighth place five years ago. The International Monetary Fund estimates the country’s households save about 46 percent of gross domestic product, almost twice the global average of 26 percent. And BCG forecasts that assets under management in the region will triple by 2025, making China second only to the U.S. No wonder, then, firms including Anthony Scaramucci’s SkyBridge Capital, Ray Dalio’s Bridgewater Associates and David Harding’s Winton are seeking to expand in China.

BCG makes a big deal about the challenge that technology poses to asset managers, which have typically been slow to implement automation in their processes. But automation should make servicing customers easier and cheaper, with improved access to transparent data about fees and returns generating increased investor trust in the industry. And there’s enormous scope for personalized marketing that targets individual investment needs more precisely to attract extra business.

Moreover, BCG says automating back-office operations to reduce errors and anticipate “choke points” could deliver enormous efficiency gains, generating cost savings of more than 50 percent. There seems to be a lot of low-hanging fruit to pick.

The point is fees will probably continue to head lower, but so will costs. Markets will do whatever markets will do, but demographic shifts will continue to expand the number of customers who need to save for old age. And while they may have been complacent in the past, asset management firms are thus far proving to be rather resilient in the face of change.

And I’m sure the likes of BCG will be only too happy to guide them through their transformation into lower-cost service providers, benefiting either from economies of scale or from product differentiation — all for a fee, naturally.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.