Looking for Stranded Oil? Start With OPEC

60 percent of the world’s oil comes from outside OPEC, produced in countries where costs are often much higher.

(Bloomberg Opinion) -- The oil market is weird.

Imagine two widget-makers, WidgetKing and Standard Widgets. Their product is generic as can be. Standard Widgets, however, is lucky enough to have its factory built next to a major port and rail terminal, keeping distribution costs low, while WidgetKing’s founder loved the mountains and thought trains would never catch on. Thus, Standard Widgets can undercut its rival on price every time. We all know who ends up controlling the widget market and who goes belly-up.

Oil doesn’t work like that. More than 70 percent of the world’s proved oil reserves are held by OPEC countries, according to BP’s statistical review. By and large, those are also the lowest-cost barrels to produce in the world (due to geology rather than logistics). And yet roughly 60 percent of the world’s oil comes from outside OPEC, produced in countries where costs are often much higher.

In keeping lower-cost barrels off the market, OPEC helps keep prices higher than they otherwise should be, thereby funding its members’ societies (the “social cost” of their oil production). In the past this dovetailed with the theory that, as oil demand would keep growing and resources were finite, an OPEC barrel kept in the ground would appreciate in value like money in a bank.

Lately, though, the notion of “peak demand” and the revival of U.S. oil production from tight rock have challenged that view. The impetus of dealing with climate change adds to the risk for oil producers of stranded assets, or barrels that never get produced at all. This actually isn’t a controversial notion. Last year, BP PLC estimated there was enough oil available to cover demand through 2050 twice over just using today’s technology.

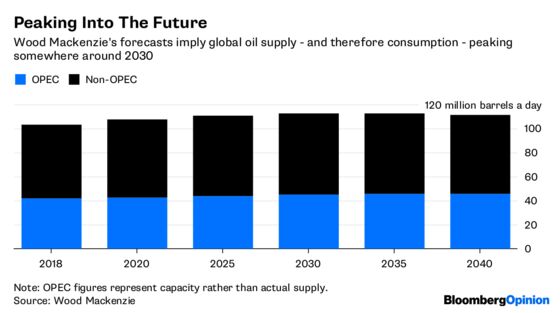

The latest long-term outlook from research firm Wood Mackenzie, released this week, supports this implicitly. Here are its forecasts for supply from non-OPEC countries and OPEC’s capacity (which is distinct from actual supply):

Woodmac’s forecasts imply a peak in global oil supply — and, therefore, demand — around 2030, with supply/capacity rising by about 9.3 million barrels a day.

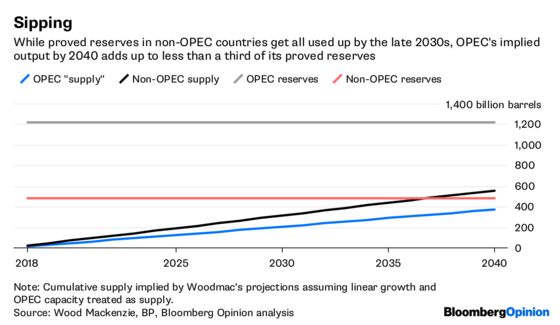

Taking these figures at face value, treating the OPEC figures as actual supply, and assuming linear increases and decreases between the five-year markers implies total production of 930 billion barrels through 2040. That equates to just 55 percent of the world’s proved reserves at the end of 2017 of 1.7 trillion barrels, as shown in BP’s statistical review.

That doesn’t equate to 770 billion barrels that never get produced; Woodmac’s projections may end in 2040, but it isn’t saying oil demand does as well. Still, the further into the future one goes, the greater the risk that things such as vehicle electrification mean a portion of those barrels never see daylight.

Moreover, such barrels look more likely to remain buried under OPEC’s soil rather than elsewhere. The group’s implied cumulative output through 2040, 372 billion barrels, could be covered by Saudi Arabia and Iraq alone, in theory.

Here’s cumulative output for OPEC and non-OPEC countries, based on Woodmac’s projections, versus proved reserves:

This picture actually underpinned OPEC’s thinking for decades. It’s just that OPEC expected other sources to dry up way before the 2030s. If there were no structural impediments to ever-rising demand, then even this chart would be attractive to OPEC, since it would imply the value of those hundreds of billions of untapped barrels would rise through 2040. As it is, though, this picture suggests stranded-asset risk resides largely within OPEC itself, rather than elsewhere — turning the old wisdom on its head.

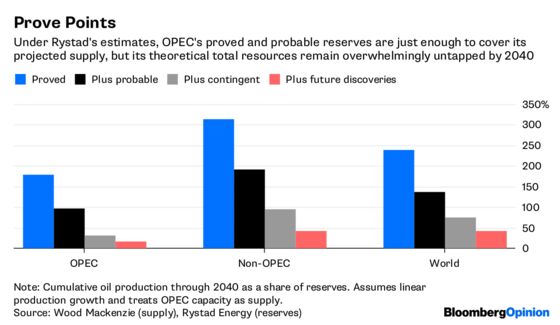

The reason lies in the detail of those proved reserves. As I wrote here, proved reserves for a country such as Venezuela are akin to imaginary numbers at this point given the above-ground obstacles to actually developing and producing them.

Rystad Energy, another research firm, recently estimated recoverable oil reserves by country that differ markedly from BP’s figures. These came in four flavors, ranging from most conservative to most speculative: proved; proved plus probable; proved plus probable plus contingent reserves in existing discoveries; and all that plus a risked estimate of future discoveries. The chart below shows production through 2040 (based on Woodmac’s projections) as a percentage of reserves under those four Rystad estimates:

Non-OPEC countries clearly require more investment in developing new reserves to meet their anticipated obligations in terms of supply. Yet the experience of the past decade not only in the U.S. but also Brazil, Canada, Russia and elsewhere suggests the industry is up to the task. When resources are abundant, things like financing, technology, execution and flexibility start to matter more relative to mere location.

OPEC, meanwhile, clearly has huge existing and potential resources. But the Rystad data emphasize how unevenly they are distributed in terms of barrels that look viable in terms of actual production. While a few members may still choose to withhold or release supply, the limitations on OPEC’s contribution to the market have become increasingly involuntary; a result of policy failure rather than policy per se.

Non-OPEC supply looks more secure through the 2020s; and beyond that the risk of demand disruption looks much higher. So it is no accident that OPEC’s de facto leader, Saudi Arabia, is making investments not merely in developing reserves and refining assets, but also more esoteric things like carbon capture and more-efficient internal combustion engines.

With the old certainties gone and competition having intensified, Saudi Arabia must both maintain or grow production and work hard to underpin demand. It must, in other words, ensure barrels keep getting sold and, in particular, its barrels get sold first. If its nominal partners end up leaving much of their oil miring underground, so much the better.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.