(Bloomberg Opinion) -- Can’t code, or speak Bahasa? Didn’t go to school with a CEO’s son or daughter? A robot will take your trading seat. Read on if you want to save your job.

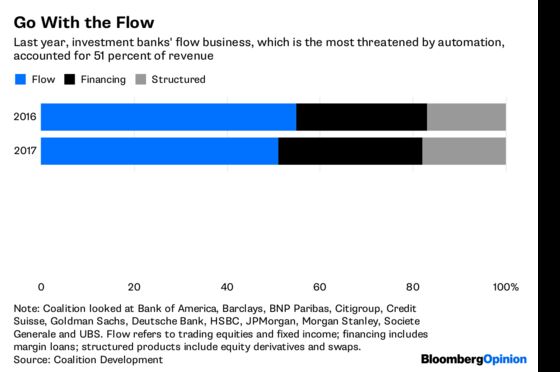

The threat from automation is in the flows part of banks’ global markets business, the most important chunk of the biggest division of investment banking. Investment banks garner 70 percent of their revenue from global markets, made up of trading stocks and bonds, as well as structuring derivatives products and financing; the remaining 30 percent comes from advisory services like shepherding M&As or helping companies raise equity and debt.

The higher-margin areas within markets — from structuring to swaps — is relationship-oriented, and therefore (relatively) safe from robot overlords. And it happens to be a big contributor to the 70 percent pie, especially in Asia, where commissions on equities and fixed-income trades are sinking fast, and language and client connections play a big role. Good news? Read on.

With the flows business comprising 51 percent of banks’ global markets revenue of $109.8 billion last year, according to Coalition data, automation of even vanilla trades is no small threat. Besides, the 30 percent advisory pie of investment banking revenue outside global markets only pays well when banks counsel on large cross-border transactions or underwrite big IPOs.

In Asia, the former is largely a Japanese game since China pulled the plug on deal-making by its overly ambitious conglomerates. And large share sales only happen in a few markets. India may be the second-biggest destination for cheap Xiaomi phones, but the Chinese firm’s Hong Kong IPO probably made more for banks than the entire Indian equity advisory industry will earn in fees this year, as a senior finance executive told one of us.

Desks have already shrunk, and will get smaller still. A decade from now all trading will be electronic. Last year, JPMorgan Chase & Co. Chairman Jamie Dimon famously boasted of a currency trader that made a $100 million bet via a cell phone. That’s the shape of things to come.

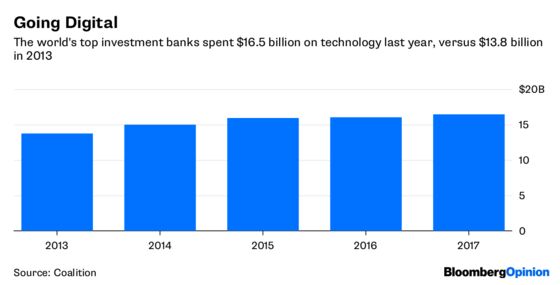

In contrast to the early days of the 2008 financial crisis, when tech was culled to cut costs, digital upgrades are now seen as both an operational necessity and a strategic differentiator. Tech spending in global-markets divisions of investment banks has risen to $16.5 billion at the 12 institutions Coalition canvassed, from $13.8 billion in 2013. A chunk of that is maintenance of bulky legacy systems, but Amrit Shahani, a London-based research director at Coalition, says large Wall Street and European banks are each spending around 10 percent, or a giddy $1 billion of their annual revenue, to stay relevant.

Chief technology officers are pushing for even bigger budgets. Their teams are the financial coders who’ve created bespoke systems for Goldman Sachs Group Inc. and the like and who are increasingly sitting on trading floors so that precious minutes aren’t wasted talking to someone in Bangalore when a huge deal blows up. Contract workers from third-party firms like PageGroup Plc’s Michael Page and Robert Walters Plc are getting seconded for a few years to help run trading floors smoothly. Headhunters say a $155,000 salary (excluding bonuses) for someone with eight years’ experience isn’t uncommon in Hong Kong, for instance. It’s not exactly banker comp, but it’s rising much faster.

Beyond the coders are the bankers-cum-traders-cum-tech thinkers.

Nomura Holdings Inc. in February hired Jezri Mohideen, a former senior trader at Royal Bank of Scotland Group Plc and Brevan Howard Asset Management, to be its global chief digital officer for investment banking. Based in Dubai, part of his job is to set up artificial-intelligence labs and merge the old and new worlds of asset custody.

Talk to any senior banker or trader and they’ll tell you there’s a lot of soul-searching going on amid threats from fintech and blockchain. The challenges are even more pressing for consumer and private banks, as well as in some corners of corporate lending such as trade finance.

Barclays Plc’s wealth management and investment operations head in the U.K. is Dirk Klee, previously at UBS Group AG’s wealth arm in technology and digital services. Singapore’s DBS Group Holdings Ltd. CEO Piyush Gupta is using open-application-programming interfaces to blur the boundaries between payments and commerce. If he doesn’t do it, Ant Financial’s Alipay or upstarts such as ride-hailing service PT Go-Jek Indonesia surely will. In trade finance, using blockchain to retire paperwork older than Shakespeare’s “Merchant of Venice” is a project both Singapore and Hong Kong are working on.

None of this is to say that investment banking is immune. Right now, there’s a rush to hire geeks — so they can make other humans irrelevant. Most banks are struggling to recruit because they “need people who not only have the new technology backgrounds but can also see how these can disrupt financial services processes and models," says Ian Woodhouse, an associate partner at financial services consultancy Orbium.

So here’s what we think in a nutshell: If you’re trading vanilla fixed-income or cash equities, you’ll only have a job in five years if your dad owns the firm. If you’re a paan-chewing, vaping kind of investment banker (the FT’s delicious description of Rajeev Misra, who built Deutsche Bank AG’s credit derivatives business), you’ll need to impress someone like SoftBank Group Corp.’s Masayoshi Son with your structuring skills. (Robots lack chutzpah.)

If you’re somewhere in between, learn to code. Or at a minium, think tech disruption on a very large scale.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.