(Bloomberg Opinion) -- Greece is approaching the threshold of a full return to the club of stable European countries that can issue debt at will. It can take a big step in that direction by issuing bonds. Officials have perhaps realized this, and they’re gauging investor demand with a U.S. roadshow on their economy. Hopefully, they also realize that the current friendly market conditions don’t have to last.

Yields on Greek bonds are right around their best levels this year. The terms resulting from the June 21 Eurogroup meeting are generous, with 8 billion euros ($9.4 billion) of extra cash and a 10-year extension on repaying its outstanding debt to the European Union. This paves the way for a smooth exit from its third bailout this summer. It now has a 24.1 billion-euro cash buffer, and any new bond deals would increase this further.

S&P Global Ratings raised its sovereign grade to B+ as a result, and has signaled a further one-notch upgrade may come if the country’s finances continue to improve. So the direction of travel is good, and investors buying now will do so in the hope of future rating changes.

A further prize awaits. The prospect of Greek debt qualifying at last for entry into the European Central Bank’s QE programs is finally in sight. As Greece’s credit rating is still well below investment grade, this will require the ECB to determine that its debt really is sustainable. What better way than a new bond deal to prove it? Investors could see this as an opportunity to get in before Greece makes its way into ECB heaven.

One of the country’s largest companies, Hellenic Telecom, tested the waters by issuing a 400 million-euro four-year note on Wednesday. And it was a big success, with an order book exceeding 1.8 billion euros. The 2.45 percent yield is 30 basis points less than what investors were originally offered. The demand really is there for Greek debt.

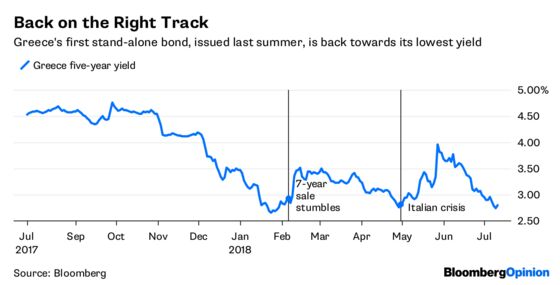

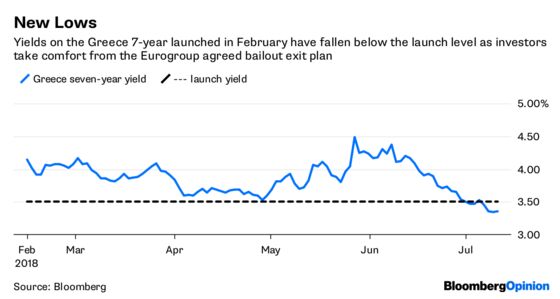

The sovereign should follow straight after. Though its cash buffer means it doesn’t necessarily need the money, it has long wanted to build a proper yield curve — a prerequisite for issuing debt without a roadshow and other investor hand-holding. It has made a start with this by issuing three billion euros in five-year debt last summer, half of which was new money, and a seven-year security in February.

Were it to issue now, a three-year note could attract strong U.S. demand, while 10-year securities would appeal more to European investors. Those maturities would fill out a basic yield curve — other outstanding Greek government bonds are often in small residual sizes after a series of exchanges, or in official hands such as the ECB, and very illiquid.

But that February sale really struggled after it priced. The 3 billion-euro size was too big, and the 3.5 percent yield was too low. After the launch, the yield soared above 4 percent. Not a good sign.

And then, as sentiment had started to improve, Italy’s political crisis erupted in May. The rout in Italian debt infected Greek securities. So Greece has been pretty much frozen out of the new issue market for five months.

But it’s opening up now — and it doesn’t pay to delay. Waiting until after the summer runs the risk of being blown out of the water by renewed Italian political turmoil — the nation starts its budget deliberations in September, and that is set to be extremely challenging for both officials and foreign investors.

The contagion from Italy is a reminder that Greece is still subject to wobbles that other European nations aren’t. It isn’t investment-grade, nor does it deserve to be at this point. The turnaround is real, but it doesn’t mean that investors can count on an easy ride.

But at least the wind is finally at Greece’s back. Completing a bond deal before the August lull hits properly would seal its return to the club of the dependables.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

©2018 Bloomberg L.P.