There’s a Bull Market in Rose-Colored Glasses

Although global equities and stocks may seem like they are doing well, a bullish market is forecast amid trade war.

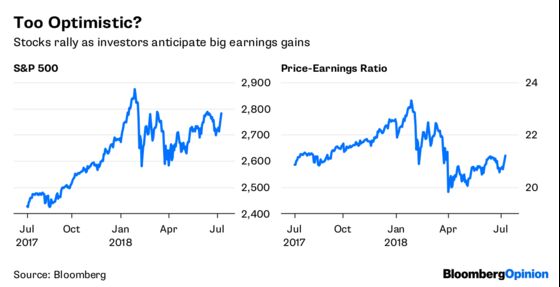

(Bloomberg Opinion) -- Stock investors started the week by pushing global equities to their biggest three-day gain since February, rallying 2.78 percent over the period. U.S. stocks led the way on optimism that companies will this week start reporting huge earnings gains for the second quarter, with profits forecast to be up 20 percent from a year earlier. But therein lies the problem.

At 21.1 times earnings, the S&P 500 Index is so richly priced that, as Bianco Research President Jim Bianco put in a research note Monday, “merely good results could be seen as a disappointment.” The risk for the bulls is that more companies follow German automaker Daimler AG and express a cautious outlook because of a budding global trade war. They key for investors is what company officials say about the potential impact of rising tariffs, the trend in labor costs with the unemployment rate at its lowest since 2000 and how manufacturers and others are coping with rising transportation costs, Peter Boockvar, the chief investment officer at Bleakley Financial Group, wrote in a research note Monday. More than a few prominent investors are saying it’s better to take the money and run, with Guggenheim Partners Chief Investment Officer Scott Minerd writing on Twitter that “markets are crazy to ignore the risks and consequences of a #tradewar. This rally in #stocks is the last hurrah!”

Minerd might be on to something. After all, first-quarter earnings came in about 23 percent higher than a year earlier, and yet the S&P 500 has struggled to a 4.1 percent gain this year. What about the benefits of tax reform? A new economic letter from the Federal Reserve Bank of San Francisco argues that such fiscal stimulus is less effective when the economy is expanding compared with its benefits when enacted during a recession, according to Bloomberg News’s Jeanna Smialek.

BONDS ARE OUT OF WHACK WITH STOCKS

The rally in stocks sapped demand for the safety of bonds, with the yield on the benchmark 10-year Treasury note rising as much as four basis points to 2.86 percent. Stock bulls better hope that the jump in yields stays as contained. That’s because a drop in the yield from about 3.13 percent in May had as much to do with the S&P 500’s almost 3 percent gain last quarter as did the outlook for earnings, according to DataTrek Research. “All the angst” over a potential global trade war “is keeping Treasury rates lower than otherwise,” DataTrek co-founder Nicholas Colas wrote in a research note Monday. “That acts as a buffer for valuations and dulls the impact of uncertainty over corporate earnings.” But if JPMorgan Chase & Co. is right, a boatload of money may be heading out of stocks and into bonds. JPMorgan strategists led by Nikolaos Panigirtzoglou wrote in a report Friday that losses in fixed-income assets this year have left the huge universe of nonbank investors, who invest in both bonds and equities, with a 45 percent allocation to equities, the highest since the Lehman Brothers crisis in 2008 and above the 40 percent average since then. On the flip side, these investors have just a 19 percent allocation to bonds, the lowest since Lehman and below the 21 percent average. In other words, get ready for a rebalancing that benefits bonds at the expense of stocks.

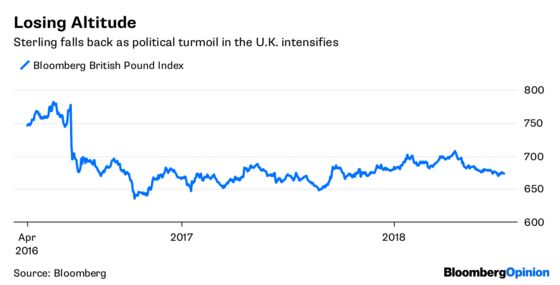

POLITICAL RISK POUNDS STERLING

The Bloomberg British Pound Index went from being up as much as 0.48 percent on Monday to being down as much as 0.59 percent after the resignation of U.K. Foreign Secretary Boris Johnson, the face of the campaign to leave the European Union in 2016. The gyrations underscore the weakness in the pound in recent months amid increasing signs of chaos in the government. While the Bloomberg gauge of the currency has dropped 4.76 percent since mid-April, it’s still some 6 percent above its post-Brexit low reached in October 2016. But if Johnson’s resignation, which followed the departure of Brexit Secretary David Davis and his deputy late Sunday, leads to a confidence vote in Prime Minister Theresa May, then there’s a chance of more political upheaval. In that case, the downside to sterling could be significant, according to BNY Mellon chief currency strategist Simon Derrick. He wrote in a research note Monday that the pound crisis of 1974-1976 could serve as a model, when neither the Labour nor Conservative parties held a sufficient number of seats to form a majority government after the 1974 election. The pound weakened some 40 percent against the German mark in those three years. During the Exchange Rate Mechanism crisis of 1992, the sterling dropped about 14 percent against the mark and 19 percent against the dollar.

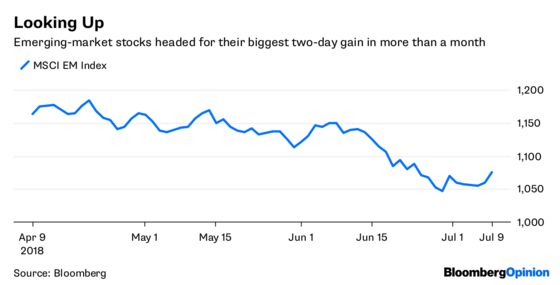

EMERGING MARKETS TURNING POINT?

The long sell-off in emerging markets that began in January may be running out of steam. The MSCI EM Index of equities rose as much as 1.55 percent on Monday to post its biggest back-to-back gain since early June. The MSCI EM Currency Index also rose for the second consecutive session, jumping as much as 0.60 percent. At about 13 times earnings, emerging-market stocks at the end of June were trading at their lowest valuations since late 2015 and down from about 16.6 times in January. Goldman Sachs Group Inc. came out with a research note on Monday saying that “EM assets now offer relative value” and that it expects “EM assets to outperform” in the second half of 2018 “as growth data stabilize (led by domestic demand and a nascent recovery in EM investment) coupled with the market's already-lowered growth expectations.” Likewise, Citigroup Inc. issued a report Monday that said it favors EM equities on “EM’s growing resilience to external shocks as well as attractive valuations.” Foreign-exchange reserves for the 12 largest EM economies excluding China topped $3.2 trillion for the first time in April, rising from about $2.85 trillion at the end of 2014 and less than $2 trillion in 2009, according to data compiled by Bloomberg. Morgan Stanley isn’t a buyer. The firm issued a report Monday saying that “we don't believe this is the start of a sustained recovery in EM and recommend reducing risk into strength. Cheap valuations should help EM to lower sensitivity to DM weakness, but not decouple.”

COPPER REMEMBERS HOW TO RALLY

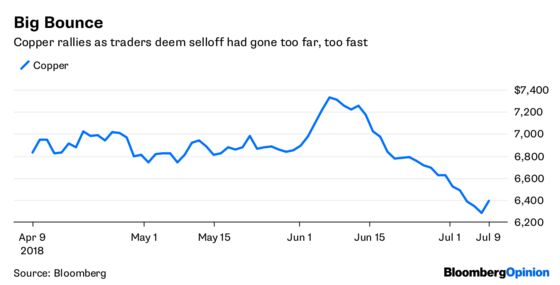

Copper posted its biggest gain in more than a month on Monday, with prices for delivery in three months climbing 1.9 percent to $6,400.50 a metric ton in late trading on the London Metal Exchange. But rather than a referendum on the metal or the global economy — copper is frequently called the metal with an economics Ph.D. because it often tracks the health of the world economy — the move appears more due to technical factors. Copper prices had fallen about 13.5 percent between June 7 and Friday in an almost uninterrupted decline. As such, the metal’s 14-day relative strength index finished last week at its deepest oversold level since late 2015. The rally in copper tracked a broad surge in base metals Monday, with aluminum, nickel and tin all jumping. Copper prices had lost more than $1,000 a metric ton since touching a four-year high on June 7 as trade tensions between the U.S. and China escalated. “Metal prices have dropped tremendously in the past few weeks, and investors are very nervous about whether this will escalate into a full global trade war,” Casper Burgering, senior sector economist at ABN Amro Bank NV, told Bloomberg News on Friday. “That nervousness is reflected in the copper price especially, given its role as a barometer of the global economy.”

TEA LEAVES

As Europe’s largest economy, Germany and its investors are often seen as a barometer for the euro zone. As such, Tuesday's report on German investor confidence by the ZEW Center for European Economic Research in Mannheim should get some special attention. The part of the survey that polls investors on their expectations, versus current conditions, has been dropping like a stone. The center’s index of expectations fell to minus 16.1 in June from minus 8.2 in May, the fourth monthly decline this year. The median estimate of economists surveyed by Bloomberg is for another drop for July, to minus 18.1, which would be the lowest since 2012. U.S. President Donald Trump is threatening levies on German cars after having slapped duties on European aluminum and steel earlier this year. The International Monetary Fund warned last week that risks to Germany’s economic outlook are tilted to the downside, citing rising protectionist trends and geopolitical uncertainty, according to Bloomberg News’s Jana Randow. The IMF predicts growth of 2.2 percent this year, down from 2.5 percent in 2017.

DON'T MISS

Trade Wars Risk Spurring Currency Devaluations: Komal Sri-Kumar

Bond Market Signals Boom Times Will End Soon: Brian Chappatta

David Who? Brexit Is a Sideshow Next to Dollar: Marcus Ashworth

Emotions and Economics Explain Stagnant Wages: Michael R. Strain

Trade War Muddles China's Battle to Curb Debt: Daniel Moss

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.