(Bloomberg Opinion) -- Rumors of the demise of medium-sized asset managers have proved to be greatly exaggerated, so far. But a combination of rising costs, a stagnant pool of profit and dwindling revenue in the next five years will hasten a divide in the industry between bigger firms enjoying economies of scale, and smaller specialists that can justify charging higher fees by excelling in niche markets.

That’s the conclusion of a report published this week by consultancy Bain & Co. which reckons firms facing a “valley of death” oversee about half of the world’s assets under management. Expect this to trigger a wave of mergers in the industry as firms try and bulk up to defend themselves. Expect also a parallel wave of marketing from smaller players claiming to have found the secret of generating alpha using algorithms or of fulfilling millennials’ sustainable investment needs without sacrificing returns.

Globally, Bain anticipates that assets under management will increase by more than 23 percent in the next five years, reaching almost 100 trillion euros ($117 trillion). But the shift toward passive funds will continue to accelerate: Assets allocated to trackers will grow by 66 percent, while the total of actively managed money will increase by a bit more than 10 percent.

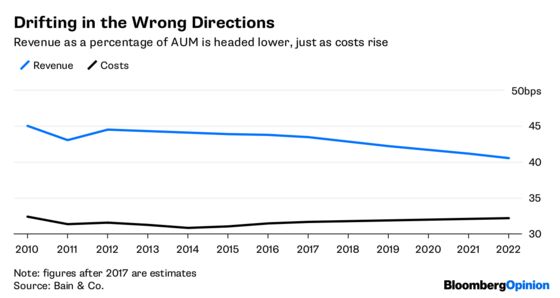

Costs will edge higher in coming years as regulators increase their scrutiny of the industry. At the same time, Bain estimates revenue will decrease as the downward pressure on fees grows ever stronger.

While assets under management have grown at a compound annual growth rate of 7 percent since 2012, profitability has declined at a rate of 2 percent. Bain expects profit will decline at a 7 percent pace in the next five years.

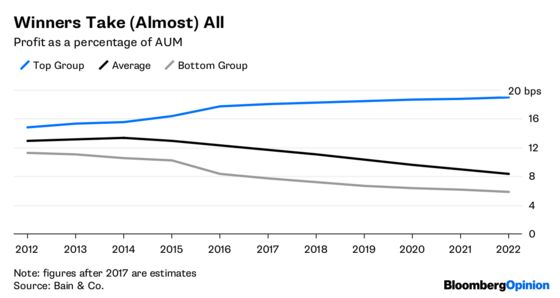

“A collapse of plain-vanilla, smaller or mid-sized firms with no competitive advantage, which we estimate represents about half of global AUM, is a highly likely scenario,” Bain says. “Winning firms with a few distinctive characteristics will benefit disproportionately from the shift of assets away from the middle.”

The word “disproportionately” is a heck of an understatement. According to Bain’s projections, there will be a profit pool of about 81 billion euros available to the fund management industry as a whole by 2022 — unchanged from 2007. But the strongest firms will capture a much bigger slice of the pie in the coming years, leaving the weak scrabbling for crumbs.

Among active managers, that probably means more mega-mergers, following the trail blazed by Janus Capital Group Inc.’s merger with Henderson Group Plc, the combination of Standard Life Plc and Aberdeen Asset Management Plc, and Amundi SA’s purchase of Pioneer Investments last year.

For passive managers, the U.S. market is dominated by BlackRock Inc., Vanguard Group Inc. and State Street Corp., which control more than 75 percent of the market for exchange-traded funds. That may make Europe and Asia more attractive destinations for firms seeking to expand their ETF offerings, either by buying rivals or adding new products.

For niche players, the growth of interest in funds focused on environmental, social and governance issues provides one specialism that’s likely to continue to command higher fees. Demand for infrastructure, private equity and real estate opportunities may also provide a lifeboat, as will the growth of interest in funds that can demonstrate expertise in harnessing artificial intelligence, big data and machine learning to generate alpha.

But for the middling asset management community, unable to differentiate either by size or specialty, the time to do or die may finally be about to arrive.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.