(Bloomberg Opinion) -- Samsung Group is showing how corporate governance reform in South Korea — despite what had seemed some initial momentum — will be like pulling teeth.

Samsung Life Insurance Co. is under pressure to sell its stake in Samsung Electronics Co., a holding that’s key to the Lee family’s control of the smartphone and semiconductor giant, Bloomberg News reported Thursday. New legislation may force Samsung Life to change the way it values the stake, pushing it over a regulatory threshold that bars insurers from putting more than 3 percent of their assets into stock or bonds of an affiliate.

At present, the Korean Insurance Business Act allows Samsung Life to value the shares at acquisition cost, or about 0.6 trillion won ($540 million), equal to 0.2 percent of total assets. The market value is 24 trillion won, or about 9 percent of assets. Another group company, Samsung Fire & Marine Insurance Co., has also used acquisition cost to value its stake in Samsung Electronics.

The possible sale is a contentious issue, with significant implications for South Korea’s regulatory system and shareholder rights.

For Samsung Life, the price of change would no doubt be high: Being forced to sell would mean paying taxes and the loss of dividend income from Samsung Electronics.

The company has hardly embraced the prospect. Management has said it’s thinking about selling down its Samsung Electronics holding — but only to stay within regulations that prohibit the financial arms of South Korean conglomerates from owning more than 10 percent of non-financial affiliates (changes to the Samsung Electronics shareholder base, such as cancellation of treasury stock, could cause its stake to exceed the threshold).

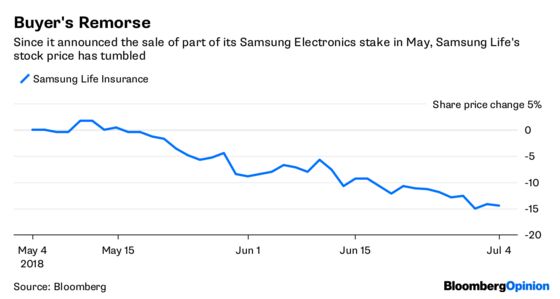

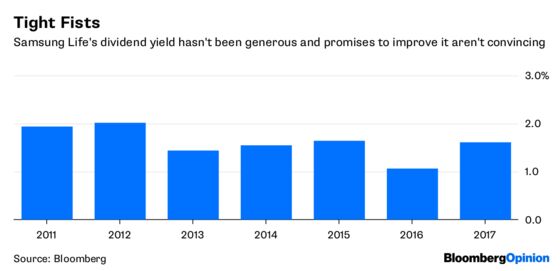

In an apparent show of goodwill, Samsung Life said any proceeds from a sale would go toward a dividend increase. That’s admirable, though shareholders haven’t bought into it. The insurer’s stock is down almost 10 percent since it said it would sell a small portion in May.

That may reflect recognition that a sustained increase in dividends wouldn’t be financially viable. Korean insurers are being pushed to boost their capital bases under new IFRS rules that come into effect in a few years. Higher payouts to shareholders — unless via a one-time special dividend — would do the opposite.

To follow through on its plan, the insurer would need to boost and then maintain an investment yield on assets of around 4 percent. It would have to add aggressive investments to meet that return and rethink its asset allocation. That’s just one of several financial issues that go into the calculus of selling down the Samsung Electronics stake.

If it decides to part with its old ways, Samsung Life could pare just enough to hit the market value threshold — an amount equivalent to 3 to 5 percent of its assets, considering shares that have already been sold.

If a sale does happen, the stake will likely be offloaded to Samsung C&T Corp., another group affiliate. Alternatively, Samsung Electronics could buy back the stake via a direct transaction. Or it could even use its free cash flow to buy a portion on the open market.

That would help the Lee family maintain its control over the web of Samsung companies, though would simply prolong the issue of chaebol cross-shareholdings rather than cleaning it up.

Regulators have so far put up a good fight. But the realities of unwinding stubborn South Korean chaebol are beginning to creep up on them.

The case of Hyundai Motor Group, where activist investor Elliott Management Corp. opposed a restructuring and put forward its own plan, is another example. Elliot pushed through some initial — and encouraging — change, but after Hyundai canceled a shareholder vote on its proposal in May, not much has happened.

The potential for long-term progress is real, even for Samsung. But like visiting the dentist, there may be some pain to get through first.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

©2018 Bloomberg L.P.