Deutsche Bank's Quarter to Forget

Trying to fix a $1.8 trillion balance sheet is hard enough, the bank is still vulnerable to jittery counterparties

(Bloomberg Opinion) -- The sun is setting on the second quarter, and not a moment too soon for Deutsche Bank AG. In 90 days, the German lender has replaced its CEO, promised thousands of job cuts, seen its credit rating downgraded, and watched its share price plumb new depths. Flunking the U.S. Federal Reserve's stress tests was a final humiliation, albeit an expected one.

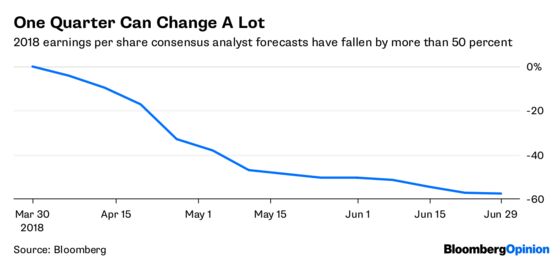

None of this is good news for the lender's underlying business, which has been unprofitable for three years running. Estimates for revenue and earnings have taken a tumble since the end of March, and not just because of problems specific to the lender. Trying to fix a $1.8 trillion balance sheet is hard enough without interest rates in the euro zone set to stay low until 2019, limited stock-market volatility, and trade tariffs weighing on economic growth.

Investors seem willing to test the proposition that all of these problems are now priced in. Deutsche Bank shares bounced as much as 4 percent on Friday. That seems bold.

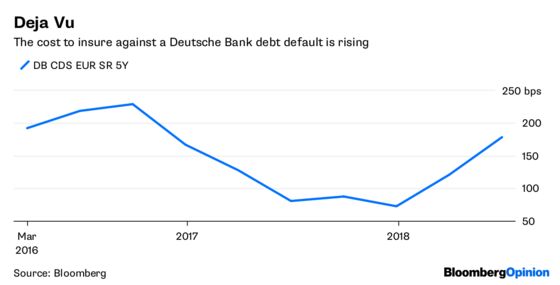

Plenty more could go wrong if performance continues to decline and management tries to muddle through. Not least, there's the risk of further credit-rating downgrades. The cost to insure Deutsche Bank's debt against the risk of default has jumped to levels not seen since late 2016. Back then, counterparties and clients were thinking twice about their exposure to the lender. Those jitters could easily return.

We know Deutsche Bank has plenty of options to try and turn things round, but none of them are cost-free. Tinkering at the margins in the hope things will get better over time risks repeating previous mistakes. Conversely, too radical an overhaul of the investment bank would hurt revenue and, by extension, profit, leading to a vicious circle.

But the current run of bad news, and the risks of losing the confidence of stakeholders and counterparties, should be a trigger for more concerted management action.

One recent heartening scenario, drawn up by UBS analysts, is that Deutsche Bank could halve the size of its investment bank, reduce revenue to about 22 billion euros from 27 billion euros, and reach a fair value of 21 euros a share – more than double the current market price of 9 euros. To get there, UBS makes a fair few assumptions – such as that costs will come down with revenue. Yet it at least suggests more can be done.

Deutsche Bank has lost market share and risks losing more. Its restructuring promises have fallen flat. Pledges to cut back on Wall Street in favor of its home market have been tempered with assurances it will stay committed to the U.S. market. There's no silver bullet, but it would surely be worth firing something into the air soon – rather than let the market force the bank's hand.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.