U.S. Housing Will Get Even Less Affordable

(Bloomberg Opinion) -- The U.S. housing sector has mostly recovered from the subprime mortgage-led collapse. The homeownership rate has started rising again, to 64.2 percent from 62.9 percent in mid-2016, and the gap between rental and mortgage costs has moved in favor of single-family owners. Also, first-time home buyers totaled 2.1 million last year, almost back to the housing boom peak.

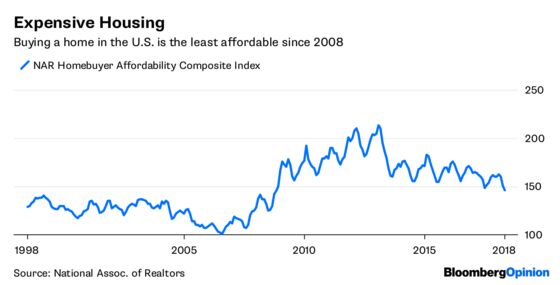

Still, buyers and realtors decry the lack of affordable inventory. The National Association of Realtors just said the inventory of available properties for sale tumbled 6.1 percent last month to the lowest ever for a May in the history of its data Why aren’t market forces filling this need? Single-family housing starts were at a 936,000 annual rate in May, half their 2006 peak level. But multi-family starts came in at a 414,000 rate, well above the 300,000 norm even though apartment vacancy rates have been rising.

These imbalances are due to both supply and demand issues. When the subprime mortgage bubble burst and single-family house prices plummeted 34 percent, homeownership collapsed from its 69.2 percent peak in the fourth quarter of 2004 as many foreclosed homeowners were busted back to being renters. So developers and builders concentrated on rental apartments, flooding the market.

Much of the single-family building in recent years focused on larger houses that appealed to upscale buyers who still had the necessary downpayment money and mortgage borrowing capability. Houses with nine or more rooms jumped from 12.5 percent of the total in 2007 to 16.5 percent in 2014, the latest data.

At the same time, investors, both individuals and increasingly institutions, bought legions of foreclosed single-family houses and turned them into rentals. Some builders constructed such dwellings to be used directly for rentals. As a share of total housing units, the portion geared to investors jumped from 30 percent before the housing boom to 34 percent today, an increase of eight million rental units. Investors are happy with their rental returns and tend to keep them longer than homeowners. That’s one reason why the median number of years that owners keep their properties has jumped from six before the housing collapse to 10 currently.

Lower turnover also results from postwar babies staying in their owned houses as they postpone retirement. The labor force of those over 65 is up 44 percent since the beginning of 2011 even though their number has increased just 29 percent.

Moderate-cost house construction is also restrained by rising building costs. Many of those Central American carpenters, masons and plumbers who facilitated the housing boom have gone home and tighter border controls are keeping out those who would like to work in the U.S. Construction industry wages have leaped 19.4 percent in nominal terms — 3.7 percent in real terms — since January 2010, when the unemployment rate in that sector peaked.

Materials costs are also jumping. Framing lumber in May cost 39 percent more than a year earlier due to the 20 percent tariff the Trump administration placed on Canadian lumber imports last year as well as forest fires and insect damages. Steel prices are up as well, with the new tariffs on imports. Homebuilding is further curtailed by stringent environmental and zoning regulations.

On the demand side, increases in home prices have outstripped income and asset gains of younger potential homebuyers. Many lack downpayment money as student debt soars. The Federal Reserve Bank of New York calculates that increases in college costs and student debt from 2001 to 2009 explains 11 percent to 35 percent of the 7.7 percentage-point drop in the homeownership rate of those in the 28 to 30 age bracket between 2007 and 2015. Those under 35 have median savings of only $1,500, and it’s just $5,000 for the 35-to-44 age group.

Those with poor credit scores and unreliable gig economy incomes face stringent credit standards, even for 3.5 percent downpayment loans from the Federal Housing Administration. Also, many prime-age men have dropped out of the labor force, lowering their homeownership chances. And, marrying later in life, low fertility rates and other lifestyle changes also cut demand.

Residential construction is a small but very volatile component of the economy, accounting for 3.9 percent of GDP in the first quarter. Still, it can have oversized effects on overall economic performance due to its volatility. As a share of real GDP, it fell from 6.7 percent in late 2005 to 2.5 percent in early 2011 during the subprime mortgage collapse. That decline of 4.2 percentage points in itself constitutes a major recession.

Housing activity is likely to recover further, but many of the supply and demand deterrents are unlikely to dissipate soon. As a result, residential construction is likely to be a much more subdued component of the economy for some time.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.