(Bloomberg Opinion) -- The benefits of low-cost index tracking for most investors are by now well-rehearsed, yet a disproportionate amount of money remains in the well-remunerated grip of active funds. Maybe the idea of achieving higher returns by investing passively just seems too good to be true — meaning stock-pickers will remain alive and kicking even if their performance after fees continues to destroy value for customers.

That’s the conclusion of a research paper released this month by J.B. Heaton, who’s about to become the law and business fellow at the University of Chicago Law School, and Ginger Pennington, an assistant professor at Northwestern University’s Department of Psychology.

We’re psychologically preprogrammed to believe the marketing hype behind active investing. “Despite clear evidence, it may simply be too difficult for a substantial number of investors to believe that superior returns are available by doing nothing but investing in an index fund rather than investing with active managers,” the paper says.

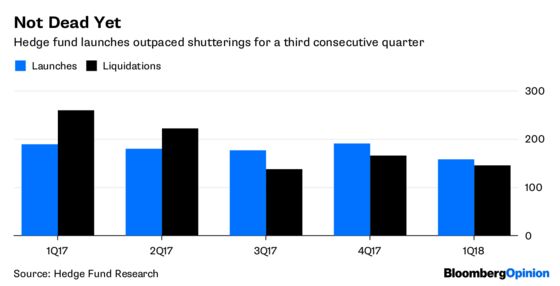

Investors continue to allocate increasing amounts of capital to exchange-traded funds, the bulk of which use low-cost passive strategies. But the hedge-fund industry has attracted new money for four consecutive quarters and saw $1.1 billion of net inflows in the first three months of this year, as my Bloomberg News colleague Katrina Lewis reported last month.

Moreover, the number of new hedge funds outpaced those being shuttered for a third consecutive quarter, albeit with the 158 launches declining to its fewest since the end of 2016, according to figures compiled by Hedge Fund Research.

Finance is a complicated business. So there’s an inherent bias to expect that “hardworking experts should provide superior outcomes,” according to the Heaton and Pennington study. Moreover, the magic of compounding seems just that — magical. Choosing active management allows fund buyers to shed any unease about winning on the stock market, by ceding culpability for those gains to seemingly sophisticated third parties.

And while opting for a tracking fund would also seem to delegate responsibility for making returns, that choice would conflict with our inbuilt desire to be in charge of our own destinies — a bias which active management seems to satisfy more fully.

The illusion of control has been shown to have harmful consequences for finance professionals. A study published by the British Psychological Society in 2003 tested 107 London traders from four investment banks. They were challenged to make the line on a graph rise as much as possible, and told that pressing Z, X or C on a keyboard every half-second might affect its development.

In fact, the chart developed randomly. And, when asked subsequently how much influence they thought their key-pressing had, those traders most convinced about the efficacy of their interventions turned out to be those who made the lowest profits for their firms and earned the lowest bonuses.

As part of their study, Heaton and Pennington surveyed about 1,000 individuals in the U.S., split roughly equally between male and female, all over the age of 30 and with annual household incomes in excess of $100,000. One of the questions posed was structured as follows:

ABC Fund invests in common stocks listed on United States stock exchanges. Which is more likely?

- ABC Fund will earn a good return this year for its investors.

- ABC Fund will earn a good return this year for its investors and ABC Fund was founded by a successful former Goldman Sachs trader and employs Harvard-trained physicists and Ph.D. economists and statisticians.

Despite the statistical trap — the much narrower universe encompassed by the second version drastically reduces the likelihood of both statements being true simultaneously — almost a third of the participants chose it as more likely. Moreover, respondents who agreed with the follow-up statement that “a person or business can achieve better results on any task by working harder than its competitors” were more likely to fall for the fallacy.

Our psychological make-up is pretty fixed, and will continue to resist logic, statistics and the evidence in favor of passive strategies. And active management seems, in the words of a European beer’s advertisements a decade ago, reassuringly expensive.

So Heaton and Pennington suggest the marketing material from the asset management industry should be forced to add caveats to its marketing materials echoing the health warnings on drugs and tobacco products: “Many active investment strategies under-perform more inexpensive alternatives. Ask your broker for more information.”

That seems like a good start to changing how investors view the investment landscape.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.