The Fed Has Enough Room to Combat the Next Crisis

(Bloomberg Opinion) -- The big news from Federal Reserve Chairman Jerome Powell last week was not so much that he still sees the need for further interest-rate increases despite signs of trouble in the global economy. Rather, the surprise was that he doesn’t believe the U.S. economy is poised to overheat. The takeaway for markets is that there is no impediment to the Fed shifting to a more dovish stance should the economy stumble.

A nimble Fed not tied down by immediate inflationary concerns greatly reduces the risk that trade wars or other shocks will send the economy into recession. Central bankers don’t need the room to reverse a recession. They just need the room to prevent one. Within this monetary policy framework, the relatively benign response of markets to rising external risks is understandable.

Powell also reiterated the Fed’s basic policy position, which is that the economy continues to power forward at a pace that exceeds its expected long-run growth. That growth keeps pressure on an already tight labor market and will soon send the unemployment rate down to a level not seen since the late 1960s. Given the threat of overheating the economy in this environment, the Fed thinks “the case for continued gradual increases in the federal funds rate is strong.”

It is natural to look at the current situation as analogous to the late 1960s and proclaim that inflation will soon accelerate to unmanageable levels. That is a risk. We don’t have many episodes of unemployment at these levels to serve as comparisons, which is why the Fed continues to raise interest rates. But the Fed is not yet overemphasizing these risks, and instead is looking to downplay them.

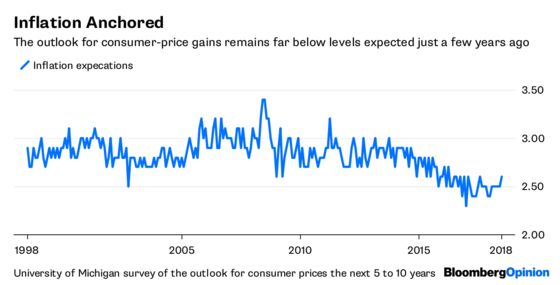

Indeed, Powell made a number of dovish points regarding labor markets and inflation in his recent speech in Sintra, Portugal. He noted the uncertainty of estimates of the natural rate of unemployment, suggesting the labor market is not yet at or past full employment. He highlighted the importance of stable inflation expectations and indicated that, if anything, those expectations have trended modestly downward in recent years. Powell views risks to financial vulnerabilities as consistent with longer-run averages. And he is willing to contemplate the possible supply-side benefits of running the labor market hot.

The totality of these remarks indicates he views the threat of overheating as relatively benign. In particular, if inflation expectations are well-anchored, the Fed can focus on the negative growth consequences from a trade war. Compare this with the Fed of the financial crisis, which was initially resistant to cut rates aggressively due to inflation concerns.

But does the Fed have the ammunition to cushion the economy from negative shocks? Commentators such as former U.S. Treasury Secretary Larry Summers like to focus attention on the lack of room for a traditional monetary response to a recession. In the past, battling a recession required 500 basis points of rate cuts, impossible to replicate when policy rates are in the 175 to 200 basis-point range.

The Fed has more than enough room to replicate the responses to the 1987 stock market crash or the 1997 Asian financial crisis. They even met the challenge of the 2015 oil price crash simply by scaling back expected rate hikes in 2016. Given the expectation among market participants that the Fed will continue raising rates over the next year, just pausing on rate hikes would be a powerful stimulus.

The likely willingness of central bankers to shift to a dovish stance may help account for the overall benign response on Wall Street so far to emerging threats from a more turbulent external environment. These include not only trade wars but also potential for financial crisis among emerging markets or the euro area. The risk these events pose for the overall economy would be bigger and more worrisome if the Fed felt its hands were tied such that they could not respond to a downturn. This is not the case. Market participants should know that the Fed is in a position to cushion the impact should these risks become a reality.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.