Markets Are on Edge, and So Are Bond Dealers

The global stock market as measured by the MSCI All-Country World Index fell as much as 1.71 percent on Monday

(Bloomberg Opinion) -- The global stock market as measured by the MSCI All-Country World Index fell as much as 1.71 percent on Monday, its biggest drop since March. Investors pinned the decline on concern that a budding trade dispute between the U.S. and its chief partners will steamroll into something much bigger that drags down the global economy. Perhaps cooler heads will prevail before it gets that bad, but those who control what is considered the most important market in the world don’t seem too optimistic.

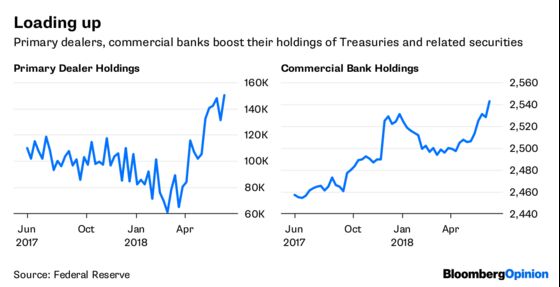

The 23 primary dealers of U.S. government securities, which are authorized to trade with the Federal Reserve and obligated to bid at the Treasury Department’s bond auctions, have built up their holdings of Treasuries and related debt to $150 billion, a record. Given their unique access to the central bank and the amount of trading volume that they experience daily, the surge in holdings begs the question of why dealers, whose members include JPMorgan Chase & Co., Goldman Sachs Group Inc. and Morgan Stanley, would be loading up on the safest investment in the world if they didn’t see some pretty severe storm clouds building in the global economy. Some might say that it’s just a byproduct of the growing amount of debt outstanding. Perhaps, but debt outstanding has been growing for years, and there has been no discernible correlation with dealer holdings. Plus, holdings of Treasuries and government agency debt by banks in general has started to rise again, reaching a record $2.54 trillion, based on Fed data released late Friday, after dropping this year through April.

More than a few investors and strategists feel that the global economy and corporate earnings are at a peak and have nowhere to go but down. Officials in both China and the European Union have said in recent days that unilateral trade actions like the kind sought by the U.S. risk pushing the world into a recession. And what about all that talk about a bear market in bonds? It seems more strategists are reconsidering. “We suggest investors buy 10-year Treasury notes outright,” Morgan Stanley global head of interest-rate strategy Matthew Hornbach wrote in a note to clients Friday. He was right, and the yield on the benchmark 10-year Treasury note dropped to 2.88 percent, moving further below the psychologically important 3 percent level.

STOCK HEADWINDS GET STRONGER

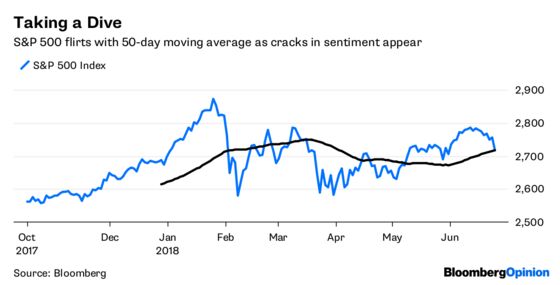

Many prognosticators have pointed to the outperformance of U.S. equities in recent weeks as a sign that investors think the Trump administration has the upper hand as trade tensions escalate. Maybe so, but that thinking was absent Monday as the S&P 500 Index fell in sympathy with its global peers. Regardless of whether you think the U.S. can come out ahead in a trade war, the headwinds are growing stronger for equities. Although Wall Street analysts project revenue growth in the second quarter to accelerate slightly to 8.7 percent from 8.5 percent in the first three months, according to DataTrek Research, earnings growth will slow to 19 percent from 24.7 percent. That’s still incredibly high, of course, but the point is that profit margins are eroding in a trend that’s not likely to sit well with investors already fretting about historically high valuations. On top of that, JPMorgan strategists led by Nikolaos Panigirtzoglou wrote in a report Friday that it appears this quarter’s gains in U.S. equities are due primarily to corporate stock buybacks. They figure that U.S. companies deployed the majority of the offshore cash that was repatriated in the first quarter, which totaled $217 billion, into buybacks. In other words, if companies stop buying back their shares with the money they are bringing home, watch out.

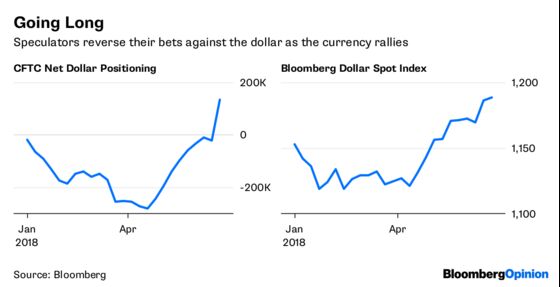

DOLLAR REGIME CHANGE

The big rally in the dollar starting in mid-April that caught most everyone by surprise is running out of steam. The Bloomberg Dollar Spot Index has weakened for four consecutive days after surging 6.28 percent between April 16 and June 19. The idea that the Federal Reserve would raise interest rates while most of the developed world stood pat dominated strategists’ explanations for the dollar’s ascent. Maybe the better one was that the rally was due largely to a sort of short squeeze in the dollar. The dollar’s move largely tracks positioning of hedge funds and other large speculators as measured by the U.S. Commodity Futures Trading Commission. Positioning reached its most bearish in mid-April before traders began unwinding what had been lucrative bets until then on the dollar’s decline. Those wagers have been steadily unwound since then, coinciding with the dollar’s rebound until finally CFTC data released late Friday showed that net positioning in the dollar was bullish for the first time since the end of 2017. Goldman Sachs is one firm that doesn’t recommend jumping on the dollar bandwagon just yet. In a report late last week, the firm's foreign-exchange strategist wrote that the greenback is likely to depreciate in the second half of the year.

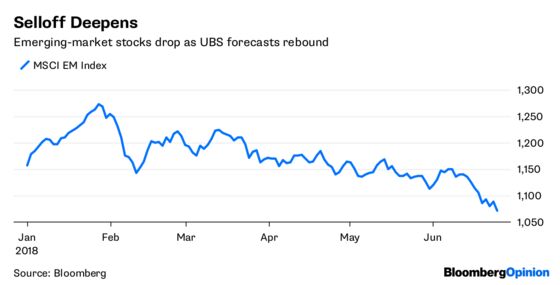

EM SELL-OFF LURES UBS

Emerging-market financial assets slid again on Monday, with the MSCI EM Index of equities dropping to its lowest since August and a separate MSCI index tracking their currencies plumbing is lowest levels of the year. Outside of some minor respites here and there, developing-market assets have steadily declined this quarter. All along, plenty of big name firms have suggested that the sell-off was overdone and have been proved wrong. Now, UBS AG is throwing its hat into the ring, with the firm’s wealth-management unit saying that these assets are poised to rally in the second half of 2018, with stocks potentially set for a 15 percent gain, according to Bloomberg News’s Ben Bartenstein. Like the Goldman Sachs strategists, UBS emerging-markets chief investment officer Jorge Mariscal expects the dollar to weaken, which will take some pressure off of developing-nation equities, bonds and currencies. Plus, Mariscal told Bloomberg News that he expects the trajectory for interest rates to become clearer and trade threats to die down. There may be something to that outlook. Although JPMorgan on Friday cut its year-end target for the MSCI EM Index to 1,230 from 1,300, that’s still above the 1,071 level where it was trading on Monday.

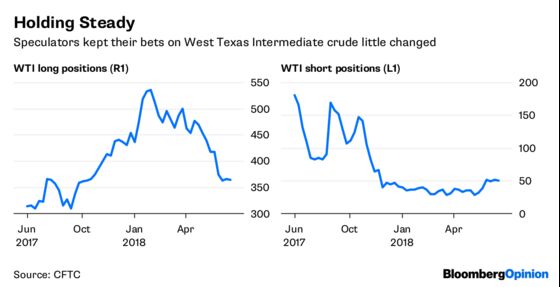

OIL MARKET LACKS CONVICTION

After surging on Friday by more than 3 percent on the decision by OPEC and its allies to boost production by only a small amount, oil prices gave back 0.8 percent of those gains on Monday as the dust cleared. But here’s the thing: It’s still unclear how much more supply will actually be poured into the market despite the group saying it will add 1 million barrels to daily supplies, and which countries will be responsible for it, according to Bloomberg News’s Jessica Summers. “This is a market lacking conviction, leadership and any sense of what’s going to happen next,” Walter Zimmermann, chief technical analyst at ICAP-TA, told Bloomberg News. “If anything, we’re ending the day with more questions than we began the day with.” Several ministers said that, in reality, the accord would add a smaller amount of oil to the market — about 700,000 barrels a day — because several countries are unable to raise their output. Going into the meeting, hedge funds kept their West Texas Intermediate net-long position — the difference between bets on a price increase and wagers on a drop — little changed, cutting it by only by 0.4 percent to 313,867 futures and options during the week ended June 19, CFTC data show. Longs dipped 0.6 percent, while shorts fell 2.1 percent.

TEA LEAVES

The Conference Board will release its monthly report on consumer confidence Tuesday, and the consensus among economists surveyed by Bloomberg is that June’s report will remain near the highest levels since 2000. But beyond the headlines, some interesting trends are developing in the data that suggest consumer sentiment may soon be headed lower. First, although the survey’s present situations index has soared, the index measuring consumers’ outlook for the future is little changed this year. As a result, the gap between the two has trended wider, just as it did in the late 1990s just before the economy entered a recession. Bloomberg Intelligence economists Carl Riccadonna and Niraj Shah wrote in a Friday report that although “such a pattern can persist for an extended period” and “is not a foreboding signal of an imminent downturn,” it is “typical of the middle-to-later stages of an economic cycle.”

DON'T MISS

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.