(Bloomberg Opinion) -- There are few places for investors to hide when a global trade war is about to erupt and the U.S. Treasury yield curve threatens to invert. Japan may be one.

The nation’s stock market has been relatively calm this year, with the Topix index down less than 2 percent in dollar terms. This is noteworthy considering a third of revenue for Topix 500 companies comes from overseas. While some manufacturers have been spared from U.S. President Donald Trump’s steel tariffs, increasing trade tensions and a stronger yen have nonetheless dented sentiment.

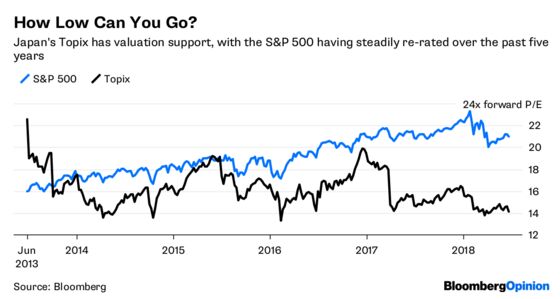

Valuations have provided some support. The Topix is trading at only 14.1 times forward earnings, below its five-year average of 16.2. The multiple for the S&P 500 Index, by contrast, has crept up steadily to reach a demanding 21 times.

Valuations alone aren’t enough, though. When global liquidity dries up, cash is the ultimate haven.

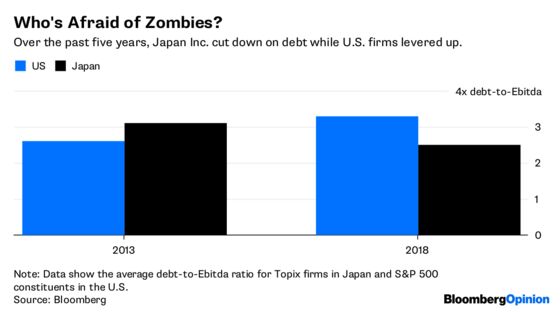

Whether because of the 2008 global financial crisis or the 2011 tsunami, Japan Inc. hasn’t taken advantage of the central bank’s torrent of easy money to boost leverage. The average Topix firm has narrowed its debt-to-Ebitda ratio to 2.5 times, from 3.1 times five years ago.

U.S. companies have done the opposite, issuing risky bonds and leveraged loans. Not surprisingly, the average S&P 500 member’s ability to service debt has deteriorated.

For the moment, the U.S. market is managing to churn on, with the S&P 500 in the green for the year. But the bearish cloud hanging over China’s A-share market offers a cautionary tale.

You might expect mainland China to be in the middle of a bull run, considering strong catalysts such as inclusion of the country’s shares in MSCI’s indexes this year. In fact, it’s among the worst performers in Asia. The main reason, as I have written, is tightened liquidity onshore. Defaults are popping up everywhere as firms struggle with refinancing.

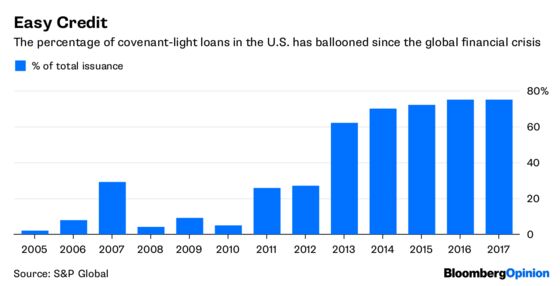

There are plenty of worrying signs in the U.S., too. Back in 2007 when financing conditions were loose, 29 percent of corporate loans were covenant-light; last year, the number was a staggering 75 percent, according to S&P Global Ratings. As a result, three-quarters of loans outstanding don’t give debt holders much protection. The picture in the bond market isn’t any better, Moody’s Investors Service warns.

Japan’s infamous zombie firms, kept alive by easy bank credit in the 1990s, used to be a popular topic of academic study for economists. Now, one can’t help but wonder if the U.S. has created its own breed of zombies.

When the Federal Reserve tightens further, these companies will have to raise equity, hold fire sales of non-core assets, or even enter bankruptcy. In any of these scenarios, shareholders will suffer. After all, if creditors are given little protection, what economic rights can shareholders expect?

To be sure, a risk-averse Japan Inc. is hardly cause for excitement. But shareholder pressure for improved returns is on the rise. The median return of 30-odd companies targeted by activist investors since last year is 17 percent, according to Bloomberg Intelligence.

When the music stops, cash-rich and conservative Japan may prove the safest of havens.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

©2018 Bloomberg L.P.