Goldman Sachs Shouldn’t Be Able to Jawbone the Fed

(Bloomberg Opinion) -- In the Trump era, bankers and regulators were supposed to get along just dandy. In the wake of this year’s stress test, there is some hope that might not be the case.

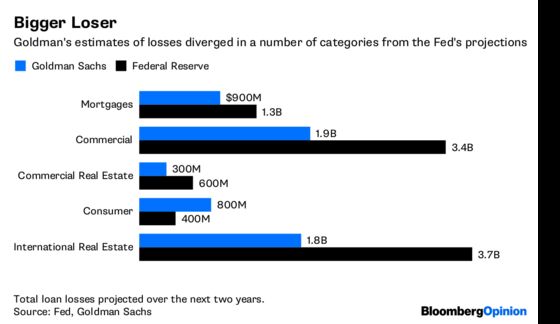

On Thursday evening, after the release of the first stage of the annual bank stress test, Goldman Sachs Group Inc. put out a statement indicating that it was unhappy with the results and said that it planned to air its grievances with the Federal Reserve. The bank said its estimate of how much it would lose in an economic downturn “diverged” from the Fed. And it suggested that after a talk with the Fed, the regulators were sure to see things Goldman’s way. “The [Dodd-Frank Act Stress Test] ratios that are published today may not represent our firm’s actual capital return capacity, which may be higher than this year’s test would otherwise indicate,” Goldman said in a statement.

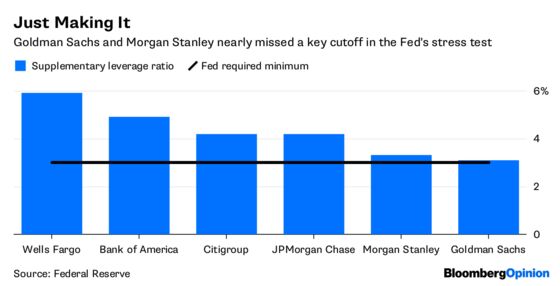

Goldman passed the test along with every other bank that was examined. But on a key metric for the big banks, the supplementary leverage ratio, Goldman passed by the slimmest margin of all the banks, 3.1 percent compared with a minimum requirement of 3.0 percent. Morgan Stanley eked by on the metric as well. The critical issue is that those slim passing grades may limit how much the Fed allows the banks to pay out in dividends or spend on share buybacks when it releases the second stage of the stress test next week. Morgan Stanley indicated that it, too, expected a more positive outcome next week.

But the divergence between the banks and the Fed is an important part of the stress test. Indeed, the headline number is a measurement of the losses the banks could face under a worst-case economic scenario and whether they would have the resources to weather that downturn. Another important point, however, is to gauge the risk controls of the banks to determine their proficiency at identifying those potential losses and estimating their size. If Goldman thinks it has a better idea than the Fed — which has looked into the books not only at Goldman but at all the banks — of how it will do in a downturn, that could be a problem. Having a divergence should result in more points being taking off, not fewer. The Fed has seemed to indicate that in the past.

The one wild card is that it’s not clear just how indicative this year’s stress test is of the regulatory future. The Volcker Rule that prohibits proprietary trading, and the Dodd-Frank financial overhaul law, have been watered down somewhat. There has even been some hints that the stress tests could go away entirely. So it’s difficult to know whether this year’s stress test, which was harsher than in the past, is a reflection of what is to come or just the last vestige of the Obama post-financial crisis era. If Goldman and Morgan Stanley get their way, it will be clear it is the latter.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.