Pimco Rains on the Junk Bond Parade

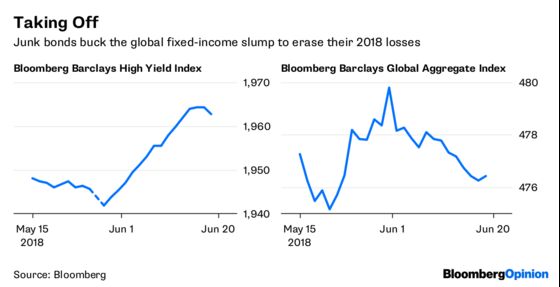

(Bloomberg Opinion) -- The market for junk bonds has come on strong this month. The Bloomberg Barclays U.S. Corporate High Yield Index has gained 0.89 percent in June through Tuesday, on track for its best performance since July and erasing its losses for the year. Going by those results, it would be easy to conclude that all is right in the world and that talk of trade wars, peak earnings and central bank policy mistakes are overblown. That would be a mistake, says Mark Kiesel.

The chief investment officer for global credit at bond behemoth Pacific Investment Management Co., Kiesel said in an interview with Bloomberg TV on Wednesday that investors should be “moving up in quality” and that bonds rated below investment grade, especially those that are deep into junk territory, “have rallied way too much.” Kiesel is not the first bond pro to express worry about this part of the debt market, but his track record (Kiesel sold his Southern California house in 2006 and moved to an apartment because he rightly thought the real estate market would tank) gives him more credibility. Kiesel isn’t calling for a crash, but his recommendation to become more cautious is warranted. At 45 percent of GDP, corporate debt is at its highest level of the current cycle and is equal to the peak of the previous expansion, Wells Fargo & Co. said in a report Wednesday. The firm also said that as of the first quarter, manufacturing companies had $505 billion of debt coming due in the coming year, a hefty 19.1 percent of their current assets when borrowing costs for all U.S. companies are hovering around their highest levels since 2011.

“High debt loads mean that debt payments coming due relative to current assets have far surpassed levels of the previous expansion,” Wells Fargo economists John Silvia and Ariana Vaisey wrote in the research note. To make matters worse, at least for bondholders, Moody’s Investors Service issued a report last week that found the covenant quality of corporate debt has remained at its weakest levels for a record 13th consecutive month.

BONDHOLDER RIGHTS TRAMPLED

With so much going on in the world, it was easy to miss some news out of Europe on Wednesday that should have grabbed the attention of both debt and currency investors. First, France and Germany issued a joint proposal that would make it easier to restructure bonds of euro-area nations that get into trouble. The motion would envision a strengthening of collective action clauses, which have been mandatory for sovereign bonds issued by euro-area states since 2013, according to Bloomberg News’s Nikos Chrysoloras. The new procedure would kick in when a member of the currency bloc seeks financial assistance from its crisis-fighting fund. Under current rules, holders of all the affected bonds voting together must approve changes, as must holders of each bond series separately. Replacing this “two-limb” voting procedure with a single-limb aggregation clause requiring a single vote by holders of the affected bonds would make it harder for holdouts to resist debt-restructuring attempts when the majority of investors finds it necessary. That sounds good in practice, but a rigorous debate among competing bondholders is a healthy process. Eliminating that would surely lead to detrimental outcomes. Second, the Bank of Portugal said U.S. money managers invested in European Union assets can’t expect equal treatment to rivals from within the bloc and aren’t subject to its principles of unfettered capital movement. The Portuguese central bank added that EU rules allow it to treat affected bondholders differently from other foreign, albeit European, creditors. Can’t say you weren’t warned.

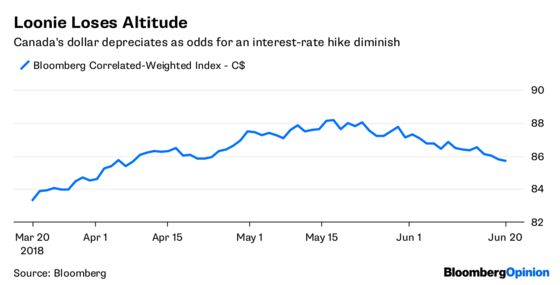

THE LOONIE NOSE-DIVES

It looks as if currency traders don’t think Canada will come out ahead in its own trade dispute with the U.S. The loonie, as Canada’s dollar is known for the aquatic bird on the nation’s C$1 coin, is the worst-performing major currency this month. It has fallen 2.68 percent to its weakest level in a year. U.S. President Donald Trump said Tuesday that America has been “treated horribly” by its northern neighbor. That’s certainly open to debate, but traders are piling into wagers that the Bank of Canada will turn dovish as erupting trade tensions shake market confidence in the outlook for future interest-rate increases, according to Bloomberg News’s Jacob Bourne. The central bank next meets on July 11, and it has made it clear that the North American Free Trade Agreement and trade are important sources of uncertainty but that it wants to gradually remove accommodation. Marc Chandler, the head of currency strategy at Brown Brothers Harriman & Co., wrote in a research note Wednesday that although trade uncertainty hasn’t been lifted, it has eased a bit. “A U.S. unilateral withdrawal from Nafta is less imminent than it may have seemed a couple weeks ago,” Chandler wrote. “The market may be underestimating the risk of a Bank of Canada rate hike and a recovery in oil prices.” One byproduct of a weaker currency is that it’s helping to boost stocks, with Canada’s S&P/TSX Composite Index closing at a record high on Wednesday.

CHARTS RULE EMERGING MARKETS

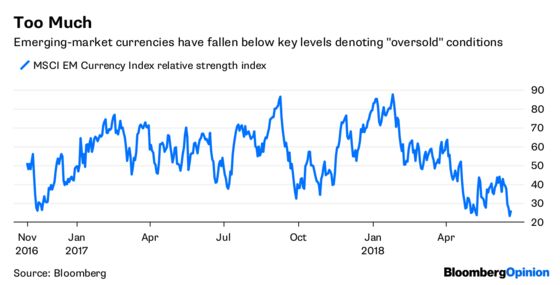

Emerging-market stocks snapped a five-day slide, with the MSCI EM Index jumping 0.67 percent in its biggest gain since June 4. It would be easy to pin the rebound from an eight-month low on a sudden rebound in confidence in emerging-market assets, but sometimes markets move for reasons other than fundamentals. In this case, the gains are more likely a recognition that emerging-market assets fell too far, too fast. On Tuesday, the 14-day relative strength index fell below 30, the threshold that technical analysts say denotes whether a security or market has become “oversold” and that rebound is imminent. Conversely, a level of 70 denotes something that is “overbought.” The relative strength of an MSCI index tracking emerging-market currencies has been in oversold territory since Friday. To some strategists, the recovery in emerging-market assets is just a chance for investors to catch their breath before the declines resume. “One red flag in chasing the EM sell-off is that short-term price action could be stretched,” Jason Daw, Societe Generale SA’s head of EM strategy in Singapore, wrote in a research note. “Unlike when we had similar signals back in the third week of May and recommended positioning for a reversal in the EM FX selloff, our preference now is for tactical long-dollar optionality.”

TRADE TIFF IS GOOD FOR SOLAR USERS

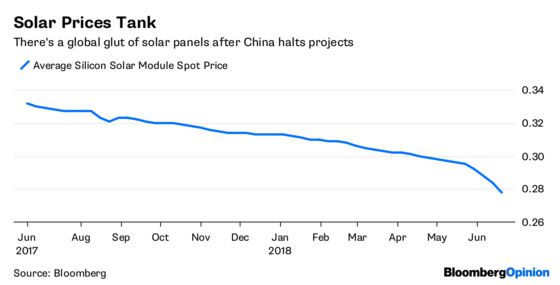

The U.S.-China trade tiff is good for solar-power users. Solar panels were already becoming cheaper this year, and then China pulled the plug this month on about 20 gigawatts of domestic installations. The result was a glut of global inventories, and prices are plunging even faster, according to Bloomberg News’s Christopher Martin. China, the world’s biggest solar market, on June 1 slammed the brakes on new projects that would have had as much capacity as about 20 nuclear power plants. With a global panel glut, it’s a buyer’s market and developers in other countries are delaying purchases, holding out for even lower prices, Martin reports. The average price for a polysilicon module slumped 4.79 percent since May 30, reaching a record low of 27.8 cents a watt Wednesday, according to PVInsights. That’s on track to be the biggest monthly decline since December 2016, the last time the industry was facing a global oversupply. China makes about 70 percent of the world’s solar components. “Chinese and international project developers are putting their orders on hold as modules get cheaper,” Yali Jiang, an analyst at Bloomberg New Energy Finance, said in a research note Tuesday. By the end of the year, she expects module prices will slide to 24 cents a watt, down 35 percent from 37 cents at the end of 2017.

TEA LEAVES

On April 16, the Bloomberg Pound Index closed at its highest since the U.K. voted to leave the European Union amid optimism that the economy was picking up and the Bank of England was poised to raise interest rates twice this year. Since then, though, sterling has faded fast, with the Bloomberg Pound Index losing almost 5 percent to its lowest point of the year. The Bank of England decided against boosting interest rates at its May 10 policy meeting, and now what was expected to be an increase in August could be in jeopardy amid some disappointing economic data and a new round of political uncertainty over Brexit. Investors and economists will get some clues Thursday when the Bank of England wraps up its latest monetary policy meeting. As of Wednesday, markets were pricing in about a 45 percent chance of a quarter-percentage point rate hike in August and an 80 percent chance of an increase by the end of the year, according to Bloomberg News’s Lucy Meakin.

DON'T MISS

Emerging Markets Have Many Tools, Few Good: A. Gary Shilling

Dow Misreads Economy in Kicking GE to the Curb: Stephen Gandel Unlike Peak Oil, Peaker Gas Has a Future in Energy: Liam Denning Erdogan Scares Off the Few Friends the Lira Had: Marcus Ashworth China Digs a Trench for the U.S. Trade Siege: David Fickling

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.