Dow Misreads the Economy in Kicking GE to the Curb

(Bloomberg Opinion) -- When the curators of the 122-year-old and most recognizable stock market index, the Dow Jones Industrial Average, looked at General Electric Co., they saw an aging industrial giant that the modern economy had passed by. So they dumped it. But their vision of the economy may be too shortsighted.

On Tuesday, S&P Dow Jones Indices’ index committee decided to remove GE, the only remaining original member of the index, from the Dow in favor of drugstore chain Walgreens Boots Alliance Inc. David Blitzer, the head of the index committee, said the switch, as he has said in the past, will result in the Dow better reflecting the economy in which “consumer, finance, health care and technology are more prominent today” than when GE joined the index in 1896 and again in 1907.

But is that right? GE has a health-care division that generates $19 billion in revenue, of which the company has only sold a small part in its effort to streamline its business. Walgreens’s revenue of $132 billion makes the index more health-care heavy. But all that revenue doesn’t come from health care. Walgreens sells batteries and candy in addition to filling prescriptions. And certainly GE derives more of its revenue from the tech sector than Walgreens does.

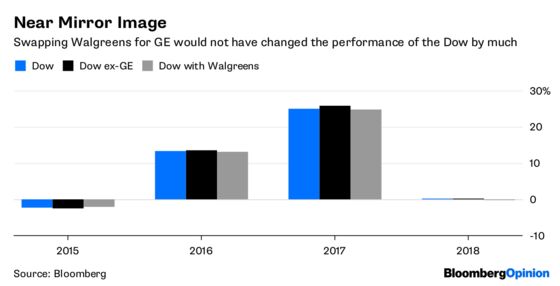

Also, it’s not clear the index’s performance would be any more reflective of the economy. If Walgreens had been in the Dow for the past year, the index would have fallen less, but not by much. GE’s shares in the past year have plunged 53 percent, including dividends. Walgreens’s stock is down 17 percent, but at $64 a share would have had a much bigger pull than GE’s $13 shares on the Dow, which is price-weighted. But the GE-included Dow is up nearly 19 percent in the past year, which seems to be pretty reflective of a good economy as well as the passage of a huge U.S. corporate tax cut. The Dow is flat so far this year, which again seems about right given the fears of rising interest rates and an incipient trade war but perhaps out of line with an unemployment rate that is below 4 percent. Walgreens, which is down 11 percent this year, wouldn’t have changed that.

The problem with the swap of GE for Walgreens is really a problem about indexes, which are the bedrock of passive investing. Someone still has to pick what stocks go in. (Unless you are going to include every stock, which some indexes do, but aren’t all that popular because it makes indexing more expensive.) And you can avoid the criticism that you are actively picking stocks, but in a slower way, by just saying you are calibrating the index to be more in line with the economy. But to do that, and make your index relevant for more than just the day you select the stocks, you have to make a call on what the economy is going to look like for the next five to 10 years, and hopefully more, or else you are going to have to become incredibly active to keep up with the economy.

Facebook Inc. or Amazon.com Inc. would have been a more defensible swap for GE. But Facebook, which many seemed convinced would be the next Dow inductee, was probably passed over because of its privacy troubles and the impact that might have on its stock price, which once again smacks of stock picking. Amazon was probably out because of its lofty stock price, highlighting once again why it’s time for the Dow to change its price-weighting formula.

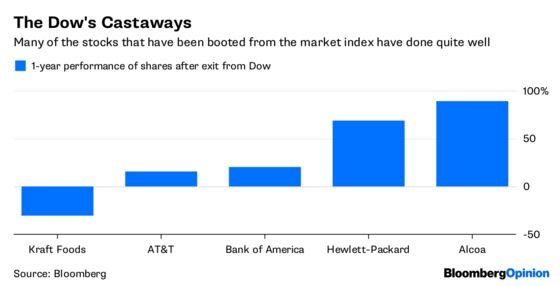

In 2015, the last time the index made a change, it dropped AT&T Inc., which has risen 15 percent since to a market cap of $237 billion and last week completed its $85 billion acquisition of Time Warner. It will be an immense player in America’s media sector as well as the information technology infrastructure, both of which are important components of the U.S. economy. In the switch before that, in September 2013, Bank of America Corp. was dropped from the index. Since then, shares of the bank are up 120 percent and banking is still a large, arguably too large, portion of the economy.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.