Why to Keep Your Inflation Anxiety in Check

(Bloomberg Opinion) -- For those feeling the vague pangs of inflation anxiety — nothing special, just the plain-old-run-of-the-mill cost of living price increases — this one is for you.

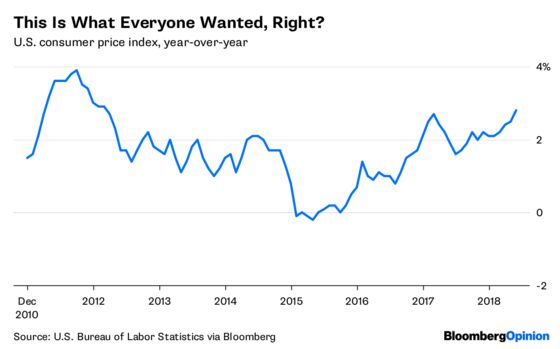

This week’s Consumer Price Index Summary showed signs that rent, health care, but most of all energy prices are rising. Year-over-year, the index increased by 2.8 percent, the fastest pace in six years as the following chart shows:

The key question: Is inflation becoming a problem that will force the Federal Reserve to act above and beyond the plan it has more or less laid out? “Not yet, but” is a fair answer, given this week’s Federal Open Market Committee statement. It notably did not contain a sentence that had been a regular part of its communications for what seems like years: “The Committee expects that economic conditions will evolve in a manner that will warrant additional gradual increases in the federal funds rate” (emphasis added), with “gradual” the key word in that sentence.

In other words, the Fed just put markets on notice that it stands ready to hike rates higher and faster than it had been previously discussing. However, recent trends imply the Fed isn’t behind the curve when it comes to inflation.

You have Milton Friedman to thank for the Fed being somewhat paranoid about inflation. He famously said, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” Only that turns out not to be the case. The Friedman thesis was tested by quantitative easing, when according to Friedman’s acolytes there should have been a big rise in prices. Some even sent a stern letter to then-Fed Chairman Ben Bernanke, warning of not just inflation, but of hyperinflation.

Only, not so much. Not only did hyperinflation not result from QE, even ordinary inflation failed to show up at the party. In a 2012 speech, San Francisco Federal Reserve Bank President John Williams called inflation “the dog that didn’t bark.”

Why didn’t the vast increase in monetary base even as output fell fail to cause the predicted Friedmanian spike in inflation? The forces of deflation — technology and automation, globalization and labor arbitrage, and the loss of negotiating power as labor union membership collapsed are all partly to blame. Perhaps the greatest manifestation of deflationary forces has been the falling velocity of money, showing how modest the number of times any given dollar is spent to buy goods and services per each unit of time. The pace has been declining for the past two decades, as the chart below shows:

Given those deflationary forces acting as a counterbalance to QE era, what then might cause an uptick in prices? Let’s consider the forces that could potentially goose inflation to levels that might force the Fed to act with more haste:

- Wages: We have been suggesting that they are poised to go up for several years now. The increases we have seen so far are only modest — mostly caused by minimum wage laws, competitive markets, and a lack of tech and science workers. If that shifts into a higher gear and wages rise significantly, it will drive up prices for both goods and services.

- Unemployment levels: After the financial crisis ended, there were six unemployed job seekers for every job opening. Today, that ratio is down to 1-to-1. With joblessness under 4 percent, a further decrease could force employers to raise wages faster, to either attract or keep workers.

- Rent: The decline in homeownership and increase in renting distorts how the shelter component of inflation is calculated. (See this and this.) But the biggest inflation-related problem in shelter has been the lack of homes for sale, sending prices up, which has led to the huge increase in demand for rentals. This has been a persistent inflationary factor.

- Energy: The biggest component of inflation of late has been energy prices. Crude oil was about $45 a barrel one year ago; today it is $75 down from $80 in May. This is the dominant component of that big year-over-year gain. If geopolitics causes a spike in prices, it could force the Fed’s hand.

My best guess is that we will see modest increases in payroll gains, even as unemployment falls more. I am less concerned about supply constraints for energy, as the oil-frackers tend to crank up supply in response to higher prices. Shelter, although a substantial portion of the total CPI basket, doesn’t appear to be running amok outside of a few urban hot spots.

The bottom line is that inflation is still only modest, with deeply entrenched deflationary forces, and a central bank ready to tighten first and ask questions later. They will cause a recession before they allow inflation to run amok.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

©2018 Bloomberg L.P.