(Bloomberg Opinion) -- Lots of people want to invest like elite university endowments, but securities laws don’t allow it. It’s time to remove those barriers.

But it’s worth asking whether investors should aspire to the so-called endowment model in the first place. According to numbers compiled by the National Association of College and University Business Officers, universities with the biggest endowments generated an average return of 9.7 percent annually over the last 30 years through June 2017 — the longest period for which annual returns are available — slightly edging out the S&P 500 Index’s return of 9.6 percent, including dividends.

Admirers of the endowment model are quick to point out that it’s less volatile than the stock market. The better comparison, they say, is a traditional 60/40 portfolio of stocks and bonds. That mix, as represented by the S&P 500 and the Bloomberg Barclays U.S. Aggregate Bond Index, returned just 8.6 percent over those three decades, or 1.1 percentage points a year less than endowments.

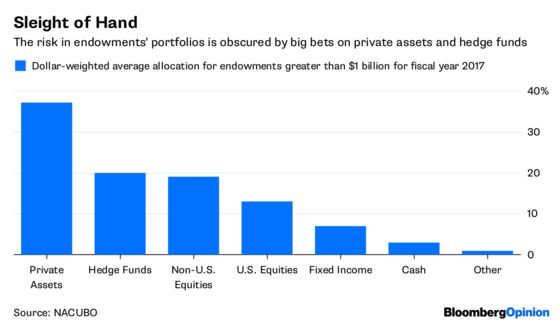

That overlooks some important details, however. For one, the endowment model is far more aggressive than a traditional 60/40 portfolio. On average, large endowments allocated roughly 90 percent of their assets to stocks, private assets and hedge funds and just 10 percent to bonds and cash, according to the 2017 NACUBO-Commonfund Study of Endowments. That’s consistent with allocations used by elite endowments for decades.

Also, that 90 percent packs more risk than the stock market. Endowments hire active managers who try to beat the market using well-known strategies such as value, momentum and quality. Their investments in hedge funds, venture capital, private equity and real estate are often illiquid and highly levered. Endowments rightly expect those investments to pay a premium over time, but it’s no free lunch.

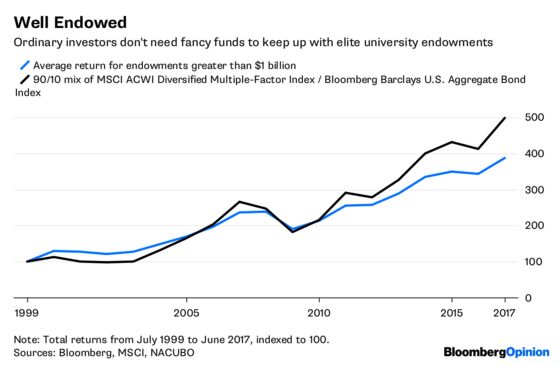

When those risks are accounted for, endowments no longer look impressive. The MSCI USA Diversified Multiple-Factor Index, for example, replicates a variety of active strategies such as value, momentum, quality and size. A 90/10 mix of the MSCI index and the aggregate bond index returned 8.5 percent annually from July 1999 to June 2017, the longest period that overlaps with the NACUBO data. That’s 0.7 percentage points a year better than the average return of large endowments over those 18 years.

Investors willing to venture overseas could have done even better. A 90/10 mix of the MSCI ACWI Diversified Multiple-Factor Index— which includes stocks from 47 developed and emerging countries, including the U.S. — and the aggregate bond index returned 9.3 percent annually from July 1999 to June 2017, or 1.5 percentage points a year better than endowments.

And investing in indexes doesn’t require a team of high-paid analysts or fancy connections. Both MSCI indexes are available through low-cost index funds.

There’s just one catch: Investors trying to outpace endowments using index funds are in for a bumpier ride. The average standard deviation of the big endowments was 11.7 percent from July 1999 to June 2017. By comparison, the standard deviation of the 90/10 mix using the MSCI USA and ACWI factor indexes was 13.5 percent and 14.5 percent, respectively.

The reason is that only a small portion of endowments’ portfolios are exposed to the swings of the stock market. Private assets aren’t publicly traded, of course, and many hedge funds are designed to dampen volatility. Large endowments allocated an average of 57 percent to private assets and hedge funds in fiscal year 2017.

A smoother ride appeals to many investors, but only rich ones are permitted to invest in venture or private equity or hedge funds. And the justification is weak. One argument is that ordinary investors are less able to bear the risks associated with those investments. That ability depends on the amount invested, however, not the type of investment. A better idea would be to grant access to all investors with guardrails around how much can be invested as a percentage of income or net worth.

A related argument is that ordinary investors could lose all their money in private assets and hedge funds, which is true. They can also lose their money buying individual stocks or cryptocurrencies, and there are no rules against that.

And the most ridiculous argument: Ordinary investors aren’t sophisticated enough for big-boy investments. But how are they to become more sophisticated when so many investments are closed to them?

I prefer index funds to the high-priced investments favored by endowments. I also suspect that the golden age of private equity and hedge funds is over. Still, all investors should be free to make those judgments for themselves, even if it means making painful mistakes along the way.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.