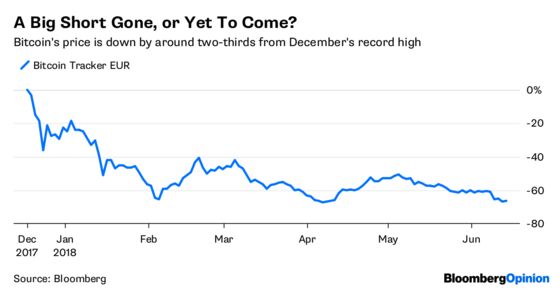

(Bloomberg Opinion) -- Bitcoin's price was supposed to go to the moon. Yet over the past six months, from high to low, the linchpin of the entire cryptocurrency craze has shed 66 percent of its value.

It's an unraveling almost on par with the Nasdaq index during the dot-com bust, or U.S. bank equities in the financial crisis. Thankfully, the wider economy has been spared deep pain — even if the full cost of scams and swindles, which by one measure totaled $670 million in a single quarter, has yet to be calculated.

It's tempting to believe that what you could call the "Big Short" moment has come and gone. With the price at about $6,500, the cryptocurrency crowd talks of a "screaming buy." Hedge fund Pantera and venture firm Blockchain Capital are predicting a rebound to $10,000 or $20,000 within the year. That's a doubling or tripling in months. It's happened before.

But such bullishness looks premature. It would mean finding a new population of incremental buyers, and keeping bearish bets at bay. To achieve both seems a stretch right now.

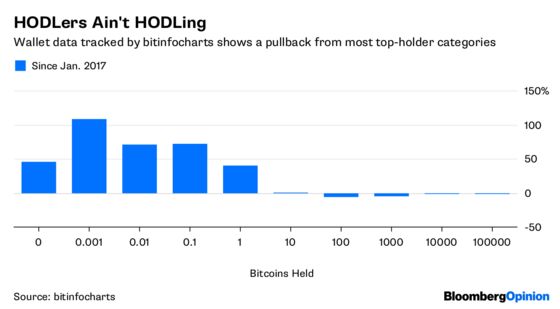

The historical record of Bitcoin suggests its greatest leaps are made thanks to speculation, rather than to any real progress in utility or technology. Bitcoin's rise to $19,000 from $6,500 at the end of 2017 was fueled by the belief that the price was only ever going to go up. There was no evidence of any increased adoption in the real world — if anything, the heuristics of Bitcoin trading called for hoarding, or HODLing, to sit on the gains.

Where is the fresh demand to repeat this feat? Most people know what Bitcoin is — and don't want to buy, given the risks. Worse still, old-time HODLers don’t appear to be sticking to their moon-shot. This column warned in December that the biggest holders were pulling back amid a boom in new arrivals, according to admittedly crude wallet data. That pressure is still there. What's missing is a new population of buyers to sell to.

Betting on Wall Street as a new source of demand is obviously tempting: A flood of institutional money looking for a gold-like store of value would be more lucrative and less fickle than consumers. With millionaires already stashing their Bitcoins in concrete vaults, and crypto futures trading on exchanges, the hope is that yesterday's get-rich-quick-scheme will become tomorrow's boring commodity market.

The problem is that it will take time, and a long-term track record of price stability, before Bitcoin is seen as a truly investable asset — let alone one that offers measurable relative or intrinsic value. The fact that regulators are only just beginning to clean out exploitable flaws and manipulations in cryptocurrency exchanges is also a red signal. We still don't know to what extent prices are being influenced by manipulative practices.

No doubt some of this confusion is keeping short sellers at bay. Steve Eisman, one of the architects of the "Big Short" of the subprime mortgage crisis, said last month that doing the same for Bitcoin was akin to debating how many angels might fit on the head of a pin. “I have no idea how to value it, and I don't think anyone else does either,” he told CNBC. No doubt hedge funds feel there are other trades out there to make at a lower cost.

But the longer these market doldrums continue, the greater the temptation to take a directional bet. Bitcoin has gone through boom-and-bust cycles in the past, but it has yet to really suffer a concerted "Big Short" moment. Screaming buys may yet become agonized sells.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.