(Bloomberg Opinion) -- Share buyback promises are running higher than actual purchases. If that flips, it could create a problem, not just for policy makers who want to portray President Donald Trump’s tax cut as worker friendly but for investors as well.

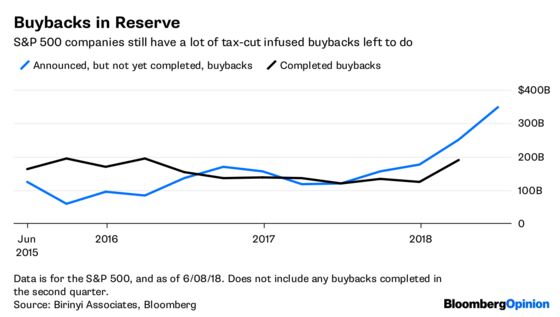

The Trump tax cut has certainly created a boom in buyback announcements. Companies in the S&P 500 have announced plans to repurchase just more than $500 billion worth of their own shares this year. That would already be a six-month record, according to data from Birinyi Associates Inc., and the second quarter still has a couple of weeks to go.

Actual buybacks, though, have yet to break any records. Second-quarter numbers, which could change that, won’t be available for another month or so. In the first three months of the year, companies in the S&P 500 Index bought back just less than $190 billion in their shares, a quarterly amount that has been topped twice in the past three years and is still well below repurchases of $224 billion in the third quarter of 2007.

The result is a growing mound of buyback dry powder, to borrow a term from the private equity world. Assume that most corporate buyback plans either get executed or expire after two years, then nearly $349 billion in buybacks have been approved but not completed, excluding purchases since March. That number stood at $252 billion at the end of the second quarter, which was already a record.

Investors cheer buybacks because they lower the number of shares outstanding, thus lifting earnings per share. They are loathed by some because of the belief that buybacks divert cash away from long-term investments or hiring workers. Even for investors, though, buybacks are not a pure positive. They can hide problems, like slowing business growth, and cause investors to overpay for shares, particularly when buybacks are not sustainable. The tax cut lowered the corporate income rate to 21 percent from 35 percent. A few months ago, I estimated that companies are spending nearly 40 percent of those savings on buybacks. Another portion of the tax law, which encourages companies to repatriate overseas profits with a lower rate, is more of a one-time boost for buybacks.

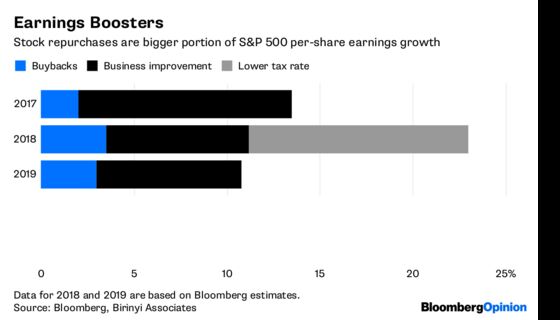

The distortion is not broad yet. The nearly $190 billion that was bought back in the first quarter only lowered the number of shares outstanding of S&P 500 companies by about 0.8 percent, boosting EPS by the same amount. Based on the current pace, buybacks could reach nearly $820 billion this year, up from $513 billion in 2017. The total impact on EPS growth would be about 3.5 percent. That’s meaningful but not going to move the needle that much this year. Bottom lines are pumping. What’s more, secondary offerings, and employee stock options, will most likely dilute some of the buyback gains. Overall, EPS for the S&P 500 is expected to increase nearly 23 percent this year. Still, take out the one-time tax boost, and real growth sinks to about 12 percent.

Next year is a different story. Overall earnings growth is expected to slow to 11 percent. But collectively S&P 500 companies will still have nearly $220 billion in buyback dry powder. Assume buybacks return to their pre-tax cut pace, and share repurchases could boost per-share earnings by about 3 percentage points in 2018, or roughly 27 percent of the overall expected EPS growth for the S&P 500. Again, this excludes any dilution from newly issued shares, which without buybacks would be a net drag on EPS.

At individual companies, the buyback growth distortion could be even bigger. PepsiCo Inc.’s $15 billion buyback plan, for instance, which was announced earlier this year and will be spread out over three years, could make up as much as 3.4 percentage points of the company’s expected 8.7 percent per-share earnings increase, or 40 percent, this year. Next year almost half of the drink maker’s earnings growth will be coming from buybacks.

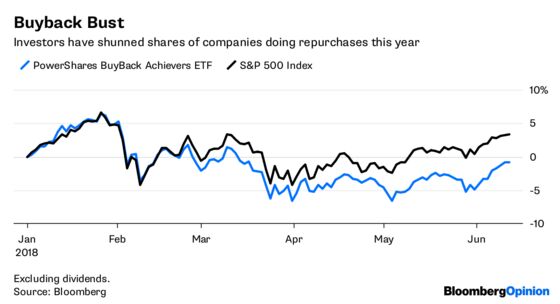

Indeed, investors should be mindful of the distortions. The PowerShares Buyback Achievers ETF, which includes shares of companies that have lowered their shares outstanding by at least 5 percent in the past year, is up just 0.2 percent this year, including dividends, compared with a 5 percent gain for the S&P 500. The harder it becomes for investors to see real growth, instead of bottom-line increases manufactured by buybacks, the more they will start looking elsewhere.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.