Burned by the Fed? Bond Buyers Have an Unlikely Haven

(Bloomberg Opinion) -- Bond investors troubled by rising global interest rates and spreading defaults in China may find an unlikely haven in middle America.

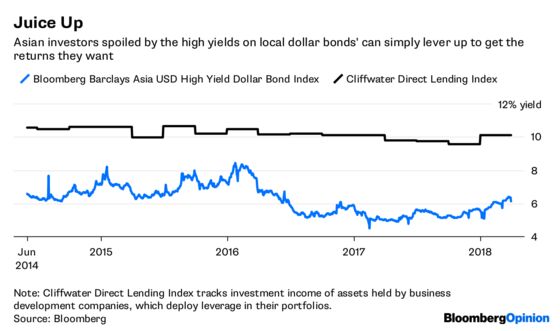

Private banks that were enthusiastic buyers of Asia’s dollar bonds in 2017 are feeling burned. The Bloomberg Barclays Asia USD High Yield Bond Index is down 3.2 percent this year, and there are whispers that worse is to come as more cases of financial stress emerge among Chinese borrowers.

Meanwhile, leveraged buyouts are booming in the U.S., and they need funding. So far this year, $356 billion of new loans were originated to finance M&A deals, a 35 percent jump over the same period of 2017 on the back of a series of jumbo transactions, according to data compiled by Bloomberg.

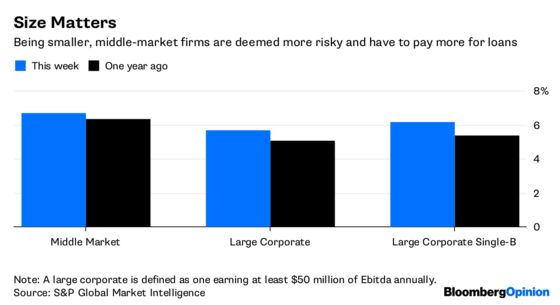

The middle market is the sweet spot. Typically backed by $10 million to $70 million in annual Ebitda, acquisition targets are too small to tap the corporate bond market, and therefore have to offer more to satisfy creditors. On average, new middle-market loans yield 6.68 percent, higher than the 6.4 percent that single-B-rated large issuers pay on corporate bonds.

Often, these loans are priced at floating rates, resetting every quarter to reflect changes in underlying benchmarks. In an environment of rising borrowing costs – three-month Libor has almost doubled in the past year to 2.33 percent - they look a lot more attractive than corporate bonds paying fixed coupons.

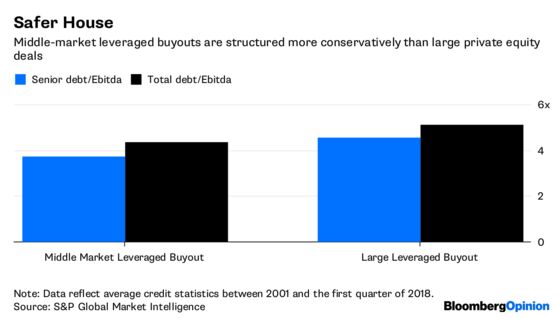

When interest rates rise, companies laden with debt – typical of those acquired by private equity firms, which use leverage to juice returns – can become distressed. But these middle-market loans are often senior and secured, a world apart from covenant-light corporate bonds. In addition, because of their smaller size, such companies can only borrow only up to five times their underlying cash flow, versus six times or more for larger firms, says Ken Kencel, president and CEO of Churchill Asset Management LLC, a specialist in the space with $4.4 billion of committed capital under management. As a result, default rates are lower.

So what’s not to like?

Liquidity is a problem. Investors who place their money with professionals such as Churchill can’t get it back until the fund closes. If they invest directly, these are essentially bank loans that can’t be traded or marked to market like corporate bonds.

But in this jittery world, the advantage of owning mark-to-market assets may be overrated, especially for wealthy clients at Asia’s private banks. In the past, they could obtain loans against bond investments at a 50 percent collateral ratio; now, lending is being curtailed. One complained to me that one of his high-yield holdings is no longer counted as collateral at HSBC Holdings Plc, even though there has been no market-moving news on the issuer. He is not only nursing paper losses but has had to deposit more money to avoid margin calls.

In these circumstances, a simpler buy-and-hold in the sleepier middle market may be a better option.

And if investors pampered by the average 7.2 percent return on Asian high-yield dollar bonds find middle-market loans aren’t attractive enough, they can always juice returns with a little leverage.

Business development companies that hold middle-market debt offered a 10.08 percent yield as of March, the latest data available. Those returns will increase after the U.S. passed legislation allowing the funds to increase their maximum leverage to two times equity, from once.

Asian investors are still smarting after being shoveled into SoftBank Group Corp.’s disastrous dollar bonds. Perhaps they should ditch the private bankers and retire to the stability of America's heartland.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

©2018 Bloomberg L.P.