(Bloomberg Opinion) -- The cleverest corporate strategies can come unstuck when they meet reality. That may include the ambitious plan hatched by Japan's Takeda Pharmaceuticals Co. to buy the British drugmaker Shire Plc. This deal has got off to a bad start, and bad starts are often inauspicious in M&A.

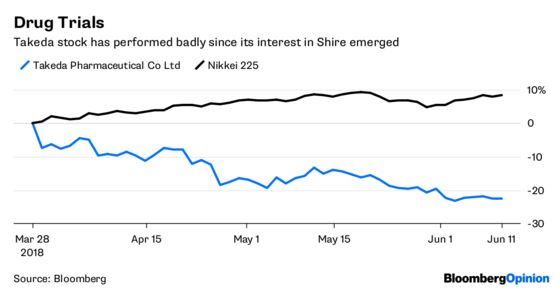

Takeda's stock fell 16 percent between its interest in Shire emerging and the agreement of terms in early May. It has since fallen another 5 percent, despite boss Christophe Weber having had the chance set out the full rationale.

The cash-and-shares offer was worth about 49 pounds per Shire share based on Takeda's closing share price as the deal was inked on May 8. That has fallen to 47.50 pounds per share based on Takeda's most recent share price. Shire itself is trading at about 40 pounds. This is a big discount to the offer price, even allowing for a year of regulatory uncertainty.

The gap is even wider if you consider that Takeda's offer would be worth 54 pounds a share at the buyer's stock price before the bid.

Weber is confident, nonetheless, that the deal will be approved by his shareholders. Perhaps. Yet that's not the only obstacle. The weakness of Shire's share price relative to the offer is a fresh invitation to a counterbid.

Takeda needs to lift its own share price, and thereby the value of its offer. The snag is that the deal just looks too big for the Japanese company – even though it is not obviously overpaying. Each side was worth around $40 billion before the takeover talks. The offer is worth about $60 billion, to be paid roughly half in cash and half in new Takeda stock, so much that its share count will double.

Many Shire shareholders won't want to hold Japanese paper, despite a planned U.S. listing. The stock market is worried that there aren't enough new investors interested in owning a large Japanese drugmaker to keep the share price at its former level.

The theoretical remedy would be to use more cash and less stock as payment. Given that the leverage on the deal will already be high, that would almost certainly require asset sales when it completes. Shire’s main attraction to Takeda is its oncology, gastroenterology and neuroscience franchises. The hemophilia and immunology businesses could be disposal candidates. They are worth a combined $34 billion in UBS's sum-of-the-parts assessment and their sale could provide a way of making the deal easier to digest.

Still, such divestments would be hard to arrange ahead of completion. Moreover, disposals would turn the takeover into a Takeda-led breakup. Weber would surely prefer to leave his options open for as long as possible by keeping the combined asset portfolio together.

He’ll be hoping that some more supportive investors come out of the woodwork, seeing as the deal may take until mid-2019 to complete. But right now, Shire has a “for sale” sign over it and the designated buyer has a problem. It's an opportunity for a gatecrasher to bid for all of Shire or make a cheeky offer to Takeda and Shire for part of it.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

©2018 Bloomberg L.P.