There’s a Special Place in Hell for Apple’s Suppliers

If you supply parts for the iPhone, there are two ways to mitigate the risk of Apple Inc. dumping you.

(Bloomberg Opinion) -- If you supply parts for the iPhone, there are two ways to mitigate the risk of Apple Inc. dumping you: create a component that’s difficult to replicate, or find some new customers.

Dialog Semiconductor Plc, which derives 77 percent of its revenue from the maker of the iPhone, appears to be taking the latter approach. It’s been discussing a combination with Synaptics Inc., a maker of touch-screen technology and fingerprint sensors far less reliant on Apple for sales.

The deal is a significant effort to untether from Cupertino, but only underlines the weakness of Dialog’s position. As Apple tries to bring more semiconductor design in-house, chipmakers that focus on silicon and get contract manufacturers (usually Taiwan Semiconductor Manufacturing Co.) to make the product for them are far more vulnerable than those with niche expertise.

Shares in Dialog have slumped after it emerged in November that Apple was preparing its own equivalent components. Last month, Dialog cut its forecast for sales of power-management chips this year saying demand from Apple is tapering more quickly than expected.

Synaptics, too, has been hurt after Apple decided not to use a fingerprint scanner underneath the screen of the next iPhone, opting instead to use front-facing 3-D sensors which unlock the device by scanning the user’s face.

The most promising opportunity for Synaptics looks to be Chinese manufacturers using the scanners in cheaper devices. Such deals won’t be as lucrative as supplying Apple, but they spread the risk of losing any one customer.

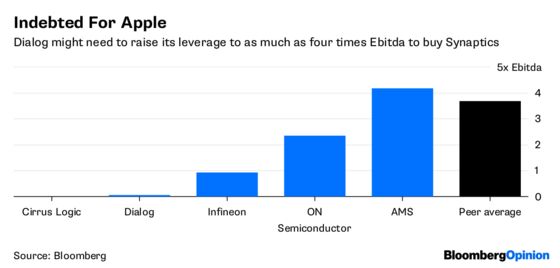

For the tie-up to work, Dialog will likely need to sweeten its offer: Synaptics rebutted an earlier $59-a-share cash offer from Dialog in March, according to CNBC. A purchase at even that level would take Dialog’s net debt to more than four times estimated Ebitda for 2019 — a significantly higher ratio than its peer group, according to Bloomberg data.

A contrast with AMS AG’s strategy is instructive. The Austrian chipmaker, which now has the highest debt ratio of Dialog’s peers, has in the past three years used that leverage to buy up a number of companies with expertise in 3-D sensors.

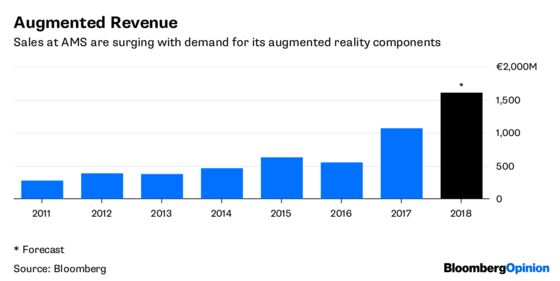

That effort is now paying off, with revenue this year set to be almost three times that of 2016. Instead of expanding in silicon-based technology, AMS turned to materials such as glass and gallium arsenide — giving itself far more protection against Apple making similar products.

Rather than investing in designs that are harder to mimic, Dialog seems to be unimaginatively seeking a way to reduce its Apple exposure. Dialog could support the additional leverage, but its willingness to use up that headroom to secure a single deal only underscores toward the grimness of its situation.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.