With Friends Like These, Who Needs Bankers? Not Ant

(Bloomberg Opinion) -- Congratulations, Ant Financial, on raising $14 billion. I’m happy for you.

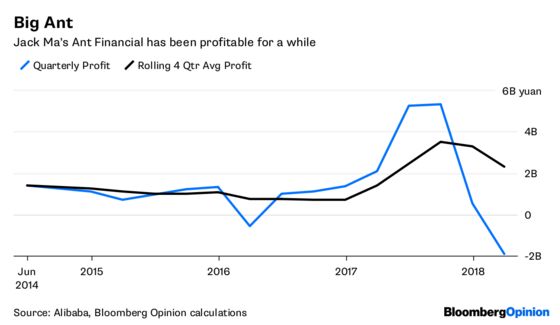

It’s not like Jack Ma’s payments and financial-services baby needs the money. The startup is already profitable (well, not in the latest quarter), and has its tentacles throughout the Chinese economy.

That didn’t stop the likes of Warburg Pincus LLC, GIC Pte., Temasek Holdings Pte. and Silver Lake Management LLC from piling in with more. With Ant being profitable, not really needing the cash, and still getting funded, it's as though an IPO isn't even warranted.

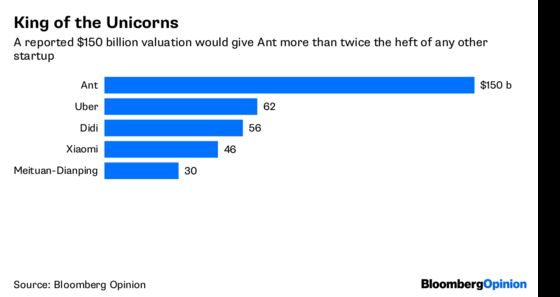

The danger with such mega-fundings is that big multiples through a public exit become ever more difficult. Xiaomi Corp. is an example: A $65 billion expected valuation upon an IPO this year is a tidy 40 percent upside from recent private-funding valuations, but that's hardly the kind of return VC investors often seek.

Diminishing returns on investment are sure to weigh on the $14 billion that Ant Financial announced Friday. But those VCs still need an exit at some point.

Enter Beijing.

Enter SOEs, to be exact. Just as state-backed funds figured prominently in Foxconn Industrial Internet Co.’s IPO earlier Friday, so too could they be a major force for Ant.

China’s government is concerned about the financial and systemic risks that surround Ant, yet it must also be quite impressed with how far the fintech startup has come in such a short time. That would make state-linked funds the ideal candidates to take some of those Ant shares off the hands of VCs as an IPO approaches.

By selling back to Alibaba Group Holding Ltd. and state-backed funds, VCs would get their exits without needing to worry about an IPO in which they'd be subject to lockup and liquidity challenges anyway.

A Hong Kong IPO will probably still happen. But the exit pressure would be alleviated by full, or more likely partial, sales to strategic investors.

Foxconn allocated 3 percent of FII’s shares to strategic investors in its IPO as part of a broader plan to curry favor with Beijing. The free float was a mere 5.7 percent. Those funds were handsomely rewarded by a 44 percent gain when the shares opened Friday in Shanghai. Since lockups span 12 months to 18 months, there’s every chance that FII will have a nice rise over the next year, thanks to government backing.

That’s the kind of support Ant could do with when it does eventually list.

Plenty of money has already been delivered by VCs, so an Ant IPO will be less a fund-raising event and more a coming-out party. And with Beijing as co-host, bankers won’t be so important for sending out invitations.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

©2018 Bloomberg L.P.