ANZ’s Bankers Were More Keystone Cops Than Criminal Cartel

(Bloomberg Opinion) -- What’s worse than calling a banker dishonest? Calling them stupid.

That may be the best defense of the former Citigroup Inc., Deutsche Bank AG and Australia & New Zealand Banking Group Ltd. executives who’ve been charged with criminal cartel offenses over a 2015 placement of A$2.5 billion ($1.9 billion) of shares in the Melbourne-based lender.

The country heads of Citi and Deutsche, and ANZ’s group treasurer Rick Moscati, are among the six named in the case brought by the Australian Competition and Consumer Commission – a shocking development in a country that, as we’ve argued before, has tended to take an indulgent approach to misconduct at the big end of town.

A shakeup of financial regulation in Australia is long overdue, and needs to go further in many ways than the current government is likely to take it. But here, the regulator may have overstepped the mark.

Full details won’t be released until the court case begins, but there’s enough evidence out there to get an idea of where the ACCC is going.

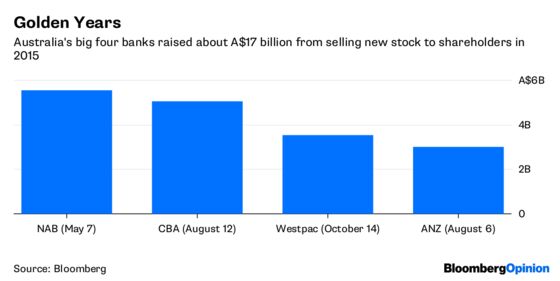

The case centers on a share placement on Aug. 6, 2015, at a time when all of Australia’s banks were topping up their balance sheets in the equity market. Citigroup, Deutsche Bank and JPMorgan Chase & Co. (which hasn't been charged) underwrote the issue at a price of A$30.95 a share, with the raising completed 24 hours after it was announced. At the same time, ANZ offered A$500 million in stock to retail shareholders – an issue that closed about a month later (oversubscribed but underpriced), with A$720 million raised at A$26.50 a share.

The Australian Securities and Investments Commission is also investigating whether ANZ’s announcement of the placement’s completion should have mentioned that the joint lead managers took up about 25.5 million of the 80.8 million shares issued, a shortfall of about one-third, ANZ said last week.

Part of the problem here is the nature of share placements, in that they create an in-group and an out-group of shareholders, and confer different rights on them. When they’re discounted – and the ANZ placement was priced 5 percent below the stock’s previous close – that’s particularly egregious, because one group of large shareholders is getting the opportunity to buy stock for less than it’s available to other investors.

Still, while share placements aren’t necessarily all that fair, they’re not illegal, either. The better grounds for a cartel case center on what happened with the shortfall that ANZ’s underwriters ended up with on Aug. 7. A video conference between the parties, purportedly discussing how to dispose of the excess stock without driving down ANZ’s share price, is expected to form the heart of the ACCC’s argument, the Australian Financial Review reported this week, without saying where it got the information.

On its own, even that behavior seems fairly harmless. The problem with cartels is the one outlined by Adam Smith:

People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices.

The world of equity capital markets doesn’t resemble that situation very closely. The key consumers for the most part aren’t an out-of-the-loop public, but a handful of buy-side investors who are quite as sophisticated about what’s going on as the sell-side. A fund manager who (say) bought a parcel of ANZ stock off Deutsche Bank in mid-August 2015, without suspecting it was part of the placement shortfall and pricing their bid accordingly, should rightly be out of a job.

Retail shareholders, to be sure, might deserve more protection – but even then, the idea that they’re basing their pricing decisions solely on regulatory statements and not the prices prevailing in the market doesn’t stand up to a lot of scrutiny.

Looking at the performance of ANZ’s share price after the placement was announced suggests any conspiracy was more Keystone Cops than Iran-Contra. The bank’s stock fell 7.5 percent the first day it returned to trading, and slumped another 8.3 percent over the month before the retail offering closed. If Deutsche Bank, Citi and ANZ were plotting to minimize the downside, they singularly failed to do so.

Indeed, the smartest guys in the room seem to have been the mom and pop investors. The A$26.50 they paid was just a sliver above the record intraday low reached during that period, and a full 14 percent below that paid by the hapless placement investors and underwriters. If there was a crime committed here, the real victims appear to have been the bankers who ended up shooting themselves in the foot.

As with previous scandals around foreign exchange and Libor, there may be more egregious details yet to emerge. And conspiring against the public is still cartel conduct, even if the public ends up outwitting the conspirators.

Still, the responsibility for clearing up the rules in financial markets should rest not with litigators, but legislators. If Australia wants to create a better environment for shareholders, its politicians must get on with passing the laws to create it.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.