Grainger Is Caught Between an Amazon and a Buffett

(Bloomberg Opinion) -- The best performing industrial stock this year is … W.W. Grainger Inc.?

This is the same supplier of factory-floor basics that got pummeled last year as investors anticipated its imminent comeuppance at the hands of Amazon.com Inc., which is seeking to do to business-goods distribution what it did to retailers. But Grainger has taken a U-turn and is now leading the S&P 500 Industrial Index, with its stock closing near a record on Monday. It’s befuddling.

Grainger was a clear beneficiary of the tax overhaul and has historically proven adept at using inflationary environments to its advantage. Many industrial markets are healthy. But the secular challenges Grainger faces aren’t going away, and even if it survives Amazon’s encroachment, its business model is apt to be significantly less profitable.

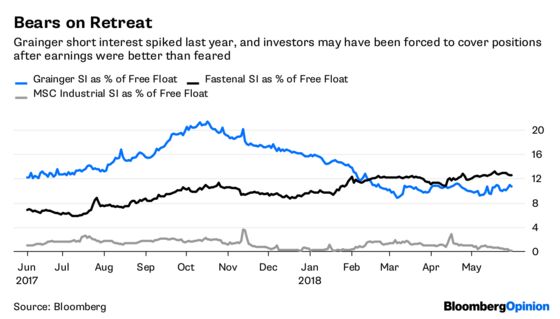

The stock’s meteoric rise is at least partly due to an unwinding of heavy short interest in the face of halfway decent earnings numbers. CEO DG Macpherson has attributed the company's above-average sales volume growth to the draconian price cuts it made last year as it grappled with the increased transparency ushered in by Amazon. Shockingly, when your products aren't overpriced, customers buy more of them.

The question is how sustainable Grainger's recent momentum is, and how profitable the growth that follows will be. It's a lot easier to notch a victory where you're lapping duds from the year before, as Grainger has been. The comparisons for the company get tougher once we get into the back half of the year. Only then will a strong performance really be proof that Grainger's plan is working and that it doesn't need to reduce prices further. Skepticism is warranted.

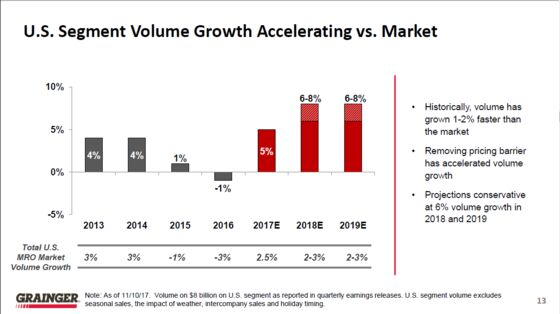

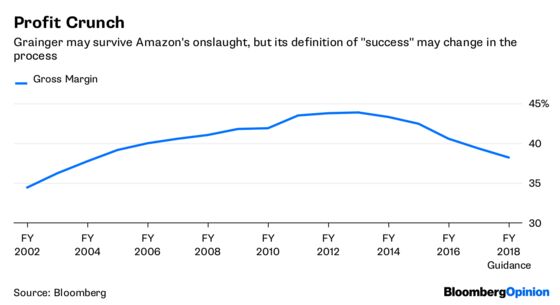

At an annual gathering of industrial CEOs last month, Macpherson got wishy-washy with Grainger's growth goals. He indicated the company is aiming for 6 percent to 8 percent volume growth over 2018 and 2019 collectively, he said. This is curious because Grainger had previously implied this was an annual target — or at least analysts took it that way. The rest of its long-term projections are tied to a more conservative 6 percent volume-growth goal, so this isn’t necessarily a cut, but Grainger seems to be giving itself extra wiggle room. Meanwhile, Grainger is calling for its gross margin to be flat in 2019 versus a decline to around 38 percent this year. Stabilization would be good if it happens, but that's still the lowest margin since 2004. And yet Grainger is trading at a premium to its historical price-earnings multiple, according to data compiled by Bloomberg.

Grainger has held its own better than I expected, but it's still not clear what differentiates the company in an e-commerce world for industrial odds and ends. Fastenal Co. and MSC Industrial Direct Co.'s business models are more ring-fenced by services and product offerings that would be expensive to duplicate. Grainger has its KeepStock inventory-management system, but most of its orders come in at about $300 a piece and a lot of its products are commoditized. While Grainger is competitive on price after its cuts, it’s not the cheapest option, says RBC analyst Deane Dray. Amazon can be vicious in price wars when it wants to be, and it seems keen on winning a bigger share of business-goods distribution.

Intriguingly, Grainger may now have other competition via Warren Buffett's Berkshire Hathaway Inc., which last year acquired Production Tool Supply. The deal wasn't publicized, but the company has since used it to launch Berkshire eSupply, a wholesale service business that aims to provide smaller distributors with access to e-commerce platforms, fulfillment services and a greater product offering than they’d otherwise be able to support. It's not clear if this offering in its current construct will make more than a marginal dent in Grainger's market share. What could make a difference is if Berkshire were to create a marketplace that listed its distributor customers' offerings alongside its own, said Alex Moazed, founder of platform innovation advisory firm Applico. Another option is a centralized landing page that directs clients to each distributor's individual website, he says, like OpenTable but for industrial goods.

Whether it's Berkshire or Amazon, Grainger has many battles left to fight.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.