(Bloomberg Opinion) -- It doesn’t feel all that long ago that Australian banks were the envy of the world.

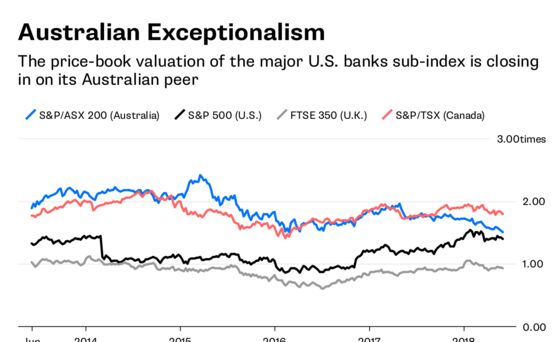

In March 2009, when stress-testing of U.S. financial institutions drove the final spasm of the previous year’s credit crisis, you could have bought all the shares in Citigroup Inc., Royal Bank of Scotland Group Plc and Barclays Plc with their $8.4 trillion of gross assets for less than you’d pay for the equity of Westpac Banking Corp., with $347 billion of assets.

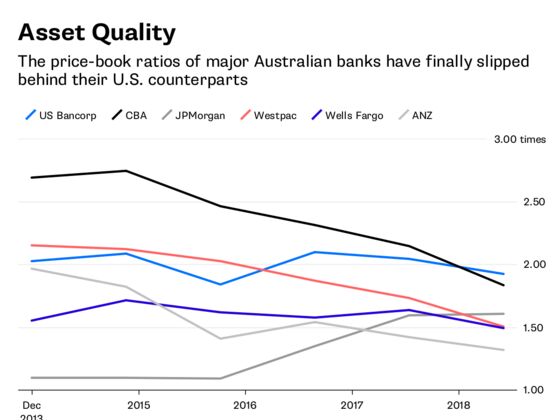

Commonwealth Bank of Australia’s share price peaked six years later just a sliver south of three times the value of its net assets, an extraordinary level in a business where price-book ratios have struggled to break above one times over the past decade.

With the current Royal Commission inquiring into practices in the country’s financial services industry and a slew of court cases, those high-flyers have come to earth with a bump. CBA on Monday agreed to pay A$700 million ($533 million) to settle a money laundering case in which it admitted that a software update allowed about 54,000 reportable transactions to go unreported over a period of almost three years.

On Friday, Australia & New Zealand Banking Group Ltd. and local units of Deutsche Bank AG and Citigroup announced they were facing possible criminal cartel charges over their handling of a A$2.5 billion placement of ANZ shares in 2015.

Having executives hauled up before government inquiries and paying out hundreds of millions in court settlements isn’t great for headlines, but it would be a mistake to see the declines in Australia’s banking sector as purely a result of this.

When your annual net income is in the region of A$10 billion, as CBA’s is, a A$700 million charge is more than just a rounding error. But the 1.2 percent jump in the company’s stock after the settlement was announced Monday is an indication that the cost is worth less to shareholders than the benefit of putting the issue firmly in the past.

The greater risk to Australia’s banks lurks not in the papers of regulators and inquisitors, but on the streets of the country’s sprawling suburbs.

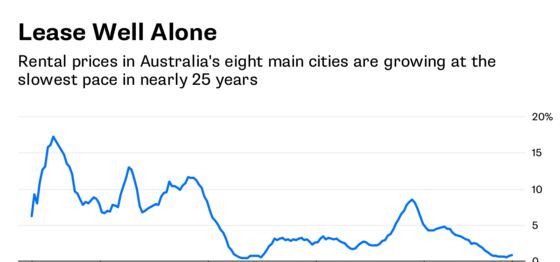

As we’ve argued before, the most ominous indicator to watch is also a favorite one of the Reserve Bank of Australia. Rents, as measured by the country’s statistics bureau, have been increasing at less than 1 percent for nine consecutive quarters , the worst performance for the measure since the housing crash of the early 1990s.

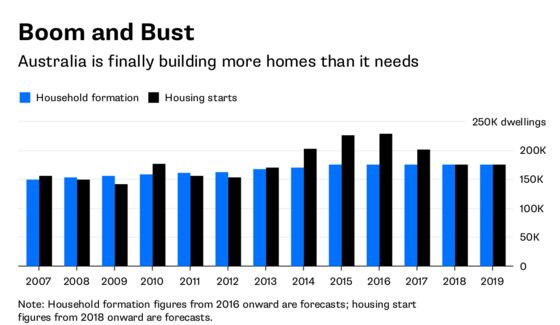

There’s a simple reason for that: Australia is finally building enough dwellings to contain its growing population. After years of undersupply, housing starts outpaced household formation in each of the past five years and will hold more or less level this year and next. That will leave the country with about 164,000 surplus dwellings relative to 2012 when the most recent slump reached rock bottom, equivalent to about a year’s supply.

In the past, episodes of such generous housing supply have tended to coincide with periods when mortgage credit was widely available too. That’s meant that the easy availability of loans has allowed the market to keep on its headlong pace of growth – but this time is different.

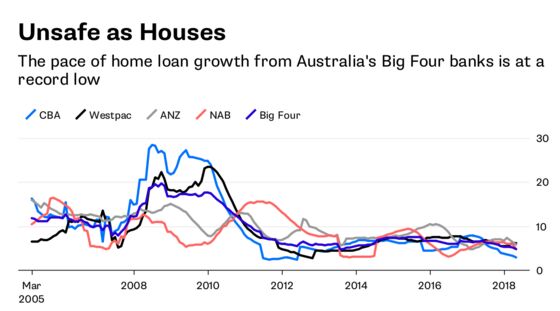

Thanks to a crackdown on credit standards by the Australian Prudential Regulation Authority, lending is expanding at the slowest pace in years. Across the Big Four banks, the value of owner-occupied and investor home loans rose at an annual pace of just 4.8 percent in April, the only month in data going back 13 years where it failed to crack 5 percent.

The effects are showing up already. In Sydney, house prices slid 3.4 percent year-on-year in April. In more exclusive suburbs, the falls are as deep as 10 percent, according to Business Insider. The share of houses sold at auction last weekend is heading toward the 50 percent levels typically considered to herald a downturn, according to the Australian Financial Review.

That, rather than bad publicity and headline-grabbing fines, is the real reason Australia’s great banking boom is over. The housing phenomenon that’s sustained profits for a generation is sputtering out, and with interest rates on the country’s hefty household debt piles forecast to start rising toward the end of this year, the worst may be yet to come.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.