Jaguar Heads for an Indian Pothole

Wrong roads always comes with the risk of hitting a pothole. And Tata Motors is right to be cautious.

(Bloomberg Opinion) -- Big trucks are all the rage in India, but Tata Motors Ltd.’s fortunes are still riding on a luxury marque that isn’t quite built for the subcontinent’s roads.

Medium and heavy-duty commercial vehicles have been the fastest-growing segment of India’s rapidly expanding auto market, with sales up more than 60 percent in May from a year earlier as transport companies upgrade fleets. That’s been a tailwind for Tata Motors, one of the country’s biggest truck manufacturers: The company reduced net losses at its local operations in the financial year ended March 31 and managed to expand still-slim Ebitda margins, despite large one-time restructuring charges.

That's a stark turnaround from what CEO Guenter Butschek called a “crisis situation” less than a year ago. Yet investors haven’t been impressed. Tata Motors stock has fallen around 7 percent in Mumbai since it announced results in May.

They’re right to be cautious. Tata Motors’ previous attempts to boost its India business haven’t worked out so well. When the automaker started ramping up its consumer finance arm to back purchases of trucks, it ended up with non-performing assets equal to 25 percent of the loan book. In September, the company completely wrote off a portfolio of loans on which it had provided guarantees in an effort to boost sales.

With truck sales back in an up-cycle, Tata Motors Finance Ltd. has returned to growth mode: Loan disbursements grew 66 percent over the past year and, worryingly, its corporate lending book doubled.

Still, if the India trend turns against Tata Motors again, there’s always its crown jewel, Jaguar Land Rover. The U.K. unit contributes most of the company’s value anyway: On a sum-of-the-parts valuation basis, it accounts for more than 70 percent of Tata Motors’ value per share. The trouble now is that Jaguar’s value is being eroded.

The British automaker is doing what most car companies have so far shied away from: spend. Others such as Toyota Motor Corp. are squarely in cost-cutting mode or, like General Motors Co., leaning on deep-pocketed investors like SoftBank Group Corp. to steer forward their dreams of electrification and autonomy. It’s impressive then that Jaguar has plowed more than 4 billion pounds ($5.4 billion) into new products and technology, or north of 16 percent of revenue. At the same time, that investment is necessary because the company remains highly exposed to diesel fuel and sagging auto markets.

Despite the cash burn, Jaguar has continued to send dividends up to its parent – averaging 150 million pounds a year. The payout increased to 225 million pounds this year, around a fifth of Jaguar’s net income, and will rise further to a quarter of the unit’s profit.

The quantum isn’t large in absolute terms, but raising the dividend when Jaguar needs to preserve cash begs the question: why now? Especially since the Indian business has started generating free cash flow for the first time in five years, as CFO P. B. Balaji boasted last month. (Admittedly, its balance sheet is still weak, with cash equal to about 40 percent of short-term debt.)

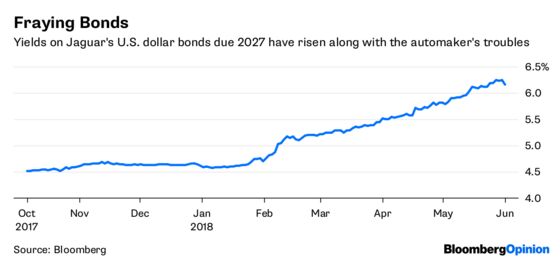

Bond investors haven’t liked the maneuver: Jaguar’s bonds due 2027 are trading at 88 cents on the dollar after dropping more than 10 percent this year. For all the halo of security that a parent provides, Tata Motors doesn’t guarantee or assume any liability for the British carmaker’s notes. The Mumbai-based company exerts significant control over any matter that requires shareholders’ approval, Jaguar’s bond prospectus states. That would include bigger and bigger dividends (though these are capped at 50 percent of Jaguar’s net income or cumulative profits since 2011).

Further cash demands from Tata Motors may threaten Jaguar’s ability to raise finance for future investment needs. The unit’s profitability is squeezed and it has pinned its hopes on China. Tata Motors could also imperil its plans to leverage the premium brand’s technology to put mass-market cars on India’s roads. One option would be to spin off Jaguar into a listed company, but with the Indian business still relatively weak, that might be too much for Tata Motors to accept.

Luxury vehicles offer a smooth and comfortable ride. Drive them on the wrong roads, though, and there’s always the risk of hitting a pothole.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

©2018 Bloomberg L.P.