Greyhound Buses Take a $3.5 Billion Ride to Nowhere

(Bloomberg Opinion) -- When a board rejects a takeover as “fundamentally” undervaluing their company, you kind of expect them to quickly demonstrate the real worth of the business to prove they know what they’re talking about.

Britain’s FirstGroup Plc, the railway and Greyhound bus operator that dismissed two approaches from private equity firm Apollo this year, did just the opposite on Thursday. It announced a 296 million pound ($395 million) yearly loss and the departure of CEO Tim O’Toole.

In fairness, we don’t know the terms Apollo was proposing before it opted not to make a formal offer. They probably weren’t generous. But after Thursday’s dreadful earnings update, Apollo’s decision looks wise – particularly given the political sensitivities involved in running British railway lines.

Contrary to expectations, FirstGroup didn’t reinstate a dividend scrapped five years ago. Instead, there was a 277 million pound impairment of Greyhound’s goodwill, plus a 106 million pound “onerous contract” provision related to a U.K. rail franchise. Shareholders sent the stock down as much as 15 percent. At about 97 pence, it’s roughly where it was in 2013 when it had to raise capital.

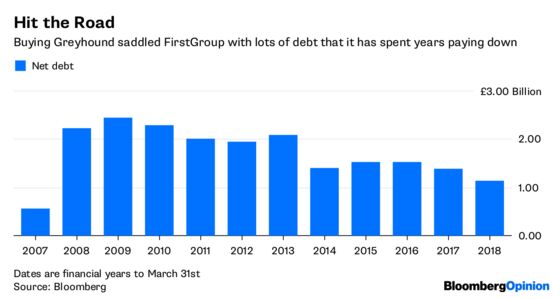

True, the writedowns clear the decks for a successor. But parting company with O’Toole is the simple bit. The group, whose assets straddle the U.S. and U.K., is too complex, and its thirst for capital means there’s not much cash left to pay down debt and to fund a big pension deficit. Finance director Matthew Gregory has announced a review of Greyhound. But fixing it, or selling it for a good price, won’t be easy.

FirstGroup bought Greyhound in 2007 in a $3.5 billion acquisition that included a network of yellow school buses, whose performance has been better. The purchase was made at the top of the market and contributed to a quadrupling of net debt, which the company has been struggling to eradicate.

Greyhound may be an “iconic” American brand, but FirstGroup realized too late that passengers aren’t sentimental. Many prefer to fly instead. A surge in new airline capacity has kept flight fares competitive and connected more cities directly. Tighter immigration checks have taken a toll on Greyhound traffic near the Mexican border.

Greyhound is struggling to cut costs because its aging fleet needs maintenance and a driver shortage has led to higher wages. Scrapping routes is also difficult without losing one of the bus network’s chief appeals: being able to find connections. Like-for-like sales fell in the financial year to March and the adjusted operating margin shrank to 3.6 percent. The next year could be tougher still.

Greyhound is sitting on some valuable inner-city property. But if FirstGroup decides to sell, it’s unlikely to fetch anywhere near the price paid in 2007. The accounts show a carrying value of 313 million pounds.

Investor anger is natural, and there will doubtless be talk of a breakup of the company. But the U.K. rail business is hardly a golden asset. FirstGroup’s provision for anticipated losses on its TransPennine rail contract suggests it was too optimistic about passenger growth. That could augur badly for its other rail concessions.

So what about a takeover? FirstGroup chairman Wolfhart Hauser told analysts on Thursday that he wasn’t opposed to a bid, so long as it provides value to shareholders. With the CEO gone and management seemingly bereft of ideas, perhaps the board would listen more carefully if an Apollo called again.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

©2018 Bloomberg L.P.