Market Rout? That Was So Yesterday

(Bloomberg Opinion) -- The Great Italian Crisis of 2018 lasted all of one day, at least judging by the financial markets.

On Tuesday, investors were in full panic mode over the notion that Italy's political situation had deteriorated to the point that it might lead to the breakup of the euro and throw the global economy into disarray. By Wednesday, though, it was blue skies for as far as the eye could see.

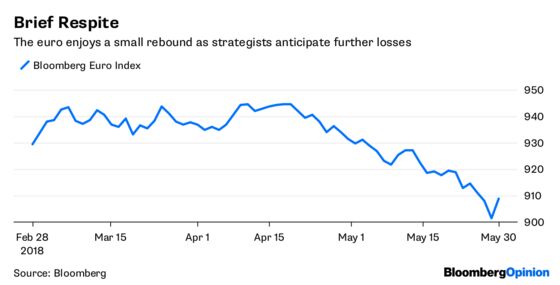

Here are the highlights: The Bloomberg Euro Index recouped all of its Monday losses to post its best gain since November; the S&P 500 Index rallied the most in seven weeks, also recouping all of its losses; U.S. Treasury notes were back to pricing in at least two more interest-rate increases by the Federal Reserve this year. Of course, nobody is really sounding the all-clear signal, but the whiplashy market movements seem to be coming with more regularity.

To some strategists, wild swings of the type seen this year are a glimpse of what's to come as major central banks join the Federal Reserve in loosening the hold they’ve had on financial markets since the global financial crisis. "All the Italian political headlines so far have occurred against a backdrop of incredibly easy monetary conditions, and should such events transpire in the future, their impact on markets will be even greater as the cushion against such shocks will be much thinner," the rates strategists at BMO Capital Markets wrote in a research note Wednesday.

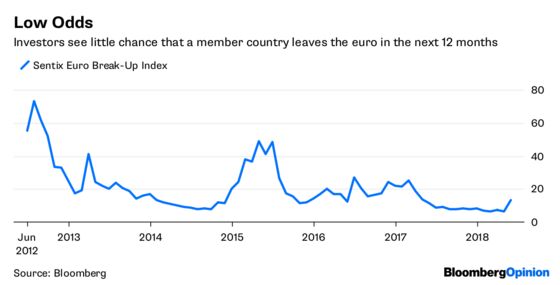

Then again, the rebound could just be a reflection of doubts that any country would ever leave the euro. The monthly Euro Breakup Index compiled by research firm Sentix shows few investors expect the euro to break up over the next 12 months despite the situation in Italy, where an effort by populist leaders to form a government collapsed after President Sergio Mattarella rejected their choice of a euro-skeptic candidate as finance minister. The Index, which was based on a poll of about 1,000 investors from May 24 to May 26, registered a reading of just 13 percent for May. That compares with the record 73 percent in July 2012 and the low of 6.3 percent in April.

EURO PESSIMISM

Even with the rebound in the Bloomberg Euro Index on Wednesday, it's been a tough year for Europe's common currency. The euro is down 1.88 percent after falling to its lowest level since July, and strategists can't reduce their forecasts fast enough. "Although we remain structurally positive on the currency, it has become difficult to envision significant appreciation over the near term," the currency analysts at Goldman Sachs Group Inc. wrote in a research report Wednesday. They now expect the euro to trade flat at about $1.15 over the next three months, and lowered their forecasts over the next 12 months to $1.25 from $1.30. The euro has dropped from about $1.24 in late April, and the strategists at Credit Suisse wrote in a research note Wednesday that they are revising their euro forecast lower in light of the latest political developments in Italy and the potential for the European Central Bank to back off its plan to pullback from its easy money policies by the end of the year. "This potential for ECB policy capitulation and related uncertainty with regards to its timing leaves us inclined to think that the recent downside pressure (on the euro) has scope to extend from here," they wrote in the report.

U.S. STARTS TO SHINE

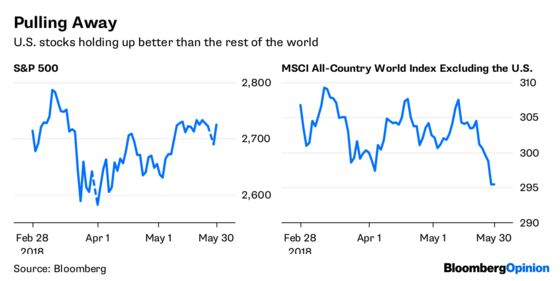

The rebound in U.S. stocks Wednesday is notable for a few reasons, not the least of which is the budding outperformance of American equities relative to their global peers of late. After largely moving in tandem this year, something began to change around mid-May in the relationship between the S&P 500 and the MSCI All-Country World Index that excludes U.S. shares. The former has managed to hold on to its gains for the year, while the latter has fallen into negative territory. The outperformance of U.S. shares is largely a reflection of expectations for continued strong earnings growth. Indeed, many economists on Wednesday beganboosting their second-quarter gross domestic product estimates following a government report that showed the nation’s merchandise-trade deficit unexpectedly narrowed in April to a six-month low of $68.2 billion. Analysts at Morgan Stanley raised their projection to a 3.3 percent annualized rate from 2.5 percent, while Macroeconomic Advisers by IHS Markit estimates the economy will expand 3.6 percent, up from a previous forecast of 2.9 percent, according to Bloomberg News' Shobhana Chandra. Michael Feroli, chief U.S. economist at JPMorgan Chase & Co., lifted his estimate by half a percentage-point to 2.75 percent and Amherst Pierpont Securities LLC’s chief economist Stephen Stanley boosted his projection to 4.2 percent from 3.8 percent.

LOSING STREAK ENDS

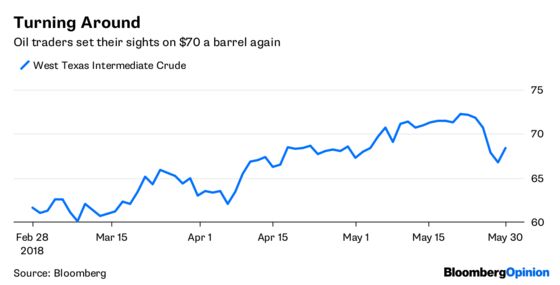

Oil snapped a five-day losing streak to stage one of its biggest rallies of the year Wednesday, gaining as much as 2.67 percent to $68.51 a barrel. Oil has become a key barometer of inflation expectations in recent weeks as prices rose above $70 a barrel in early May for the first time since 2014. In turn, those higher inflation expectations have weighed on the bond market, boosting borrowing costs for the government, companies and consumers as traders price in more Fed rate hikes between now and the end of the year. The big move higher in oil Wednesday was pinned on the weaker dollar, the potential for heightened trade tensions between the U.S. and China, and a weekend meeting between producers including Saudi Arabia and Kuwait in Vienna, according to Bloomberg News' Jessica Summers. In the U.S., crude inventories are seen contracting, further providing a boost to oil’s rally. The Vienna meeting of oil producers might reveal a change to OPEC’s current plan to limit production, Summers reports. Saudi Arabia and Russia have a difficult month ahead, according to Nordine Ait-Laoussine, president of Geneva-based consultant Nalcosa and former energy minister of Algeria. He said the de-facto leaders of the coalition that masterminded a recovery in oil prices have just three weeks to persuade their allies to change tack and boost output.

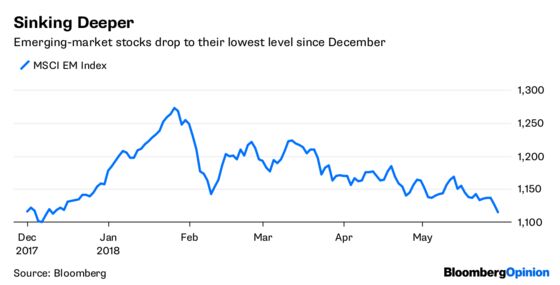

MOODY'S IS DOWN ON EM

Emerging-market investors decided not to participate in the broad recovery in riskier assets on Wednesday. The MSCI EM Index of equities dropped as much as 1.40 percent to close at its lowest level since December. The bulk of the losses came in Asia, followed by Eastern Europe. The Institute of International Finance issued a research reporting noting that $19 billion has flowed out of emerging-market stocks and bonds between April 16 and the end of last week. Moody's Investors Service said it now expects emerging-market economies to expand at a slower pace, with growth decelerating to 5.2 percent this year and next from 5.3 percent in 2017. "Ongoing financial market turbulence in emerging market countries poses risks of a broader negative spillover effect on growth for a range of countries beyond Argentina and Turkey, while there is a risk that high oil prices will weigh on purchasing power and present an upside risk to inflation," Moody's Senior Credit Officer Madhavi Bokil wrote in a research note. In a sign of pessimism over emerging-markets, the extra yield investors demand to own bonds from non-investment-grade borrowers rather than their higher-rated peers is about 2.91 percentage points, heading for the biggest monthly increase since September 2015, weeks before the Fed raised rates for the first time in almost a decade, according to Bloomberg News Lyubov Pronina.

TEA LEAVES

The Trump administration maintains that all Americans will benefit equally from the tax reform enacted at the end of last year, not just big companies. That might ultimately turn out to be true, but so far consumer spending is looking pretty anemic. The Commerce Department said Wednesday that spending by consumers grew by just 1 percent in the first quarter. Not only was that the smallest gain in almost five years, it was also below the Commerce Department's initial estimate of 1 percent and below the 1.2 percent forecast by economists. Are consumers really that gloomy? And if so, why do various surveys show near-record high consumer confidence? Perhaps some answers may come Thursday, when the government provides data on personal incomes and spending for April. Overall, spending is forecast to have risen at a decent 0.4 percent in the month. But after accounting for inflation, spending likely only increased 0.2 percent, which is hardly the stuff of animal spirits.

DON'T MISS

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.