Absolute Power Disrupts Absolutely in Silicon Valley

Dual-class shares, other “founder-friendly” investment terms have done too much damage in Silicon Valley and beyond.

(Bloomberg Opinion) -- No one has learned any lessons.

That’s the discouraging takeaway from a Wall Street Journal article on Tuesday about the nearly unchecked power held by founders of many young technology companies. The people bankrolling those companies are responsible for providing oversight, too, but don’t seem to be doing much of it.

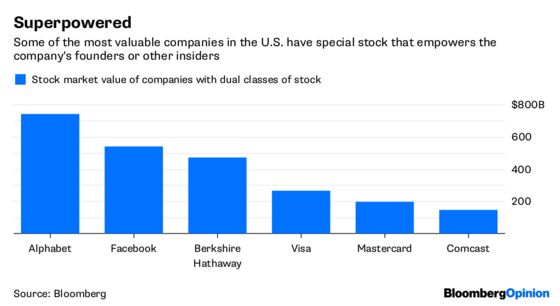

The Journal reported that two-thirds of U.S. startups with venture-capital investors that went public last year had special stock giving insiders more votes than other shareholders and therefore disproportionate power over the company’s direction. These terms aren’t unusual in the technology and media industries. Google parent Alphabet Inc., Facebook Inc. and the New York Times Co. have dual-class shares that in theory allow executives to pursue important initiatives without inference from investors pushing for a quick buck.

That sounds sensible, but dual-class shares and other “founder-friendly” investment terms have done too much damage in Silicon Valley and beyond. There was, of course, the boardroom brawl at Uber Technologies Inc. over ending the voting control of co-founder and CEO Travis Kalanick. Theranos founder Elizabeth Holmes had near absolute authority over a startup that proved to be far less than she claimed. I wonder how public market investors feel now about Snapchat stock that leaves them without any power at all to overrule young leaders that have proved to be inept.

And yet many founders still have near absolute authority over their young companies. A particularly disheartening example in the Journal article was the real estate startup WeWork Cos., whose co-founder and CEO is one of only two members of the board’s compensation committee. In short, it’s possible the WeWork CEO is helping determine compensation for himself and other members of his executive team.

It’s ironic that the other member of WeWork’s compensation committee is from Benchmark, the venture-capital firm that led efforts to eliminate Kalanick’s voting power over Uber after he proved to be a toxic presence who shrugged off oversight from his investors and others.

The prevalence of startup executives with near-absolute power is the result of economic logic. Now more than ever, there’s a huge supply of capital for the most promising young tech companies, and those investors are often chasing a small startup elite. The imbalance enables executives of superstar startups to demand whatever terms they want from investors, and they often want the ability to make decisions without interference.

The problem is there have been so many examples of young companies stumbling — with disastrous effects — when founders are left to run wild. In addition to Uber, there were several scandals involving improper workplace behavior at startups including Social Finance Inc. and Zenefits Inc. that made me wonder whether backers of young tech companies feel they can’t ask too many tough questions about employment conditions or dodgy financials for fear of being shut out of potentially lucrative investments.

Lax oversight and overpowered founders from the earliest days of a company can enable corporate rot that takes years to root out. Tesla CEO Elon Musk sure looks like he could use more oversight from his own board. Turmoil at Viacom and CBS is a cautionary tale about the ill effects of perpetual insider control.

It’s hard to imagine that tech startup financiers are going to push back against founders who demand absolute authority. Startup economics simply have swung too much in founders’ favor. But there is one cudgel that public and private investors can employ to mitigate the danger of over-entitled founders: sunset provisions on superpower stock.

This idea is a favorite of corporate governance advocates including Lucian Bebchuk of Harvard Law School, and a member of the Securities and Exchange Commission recently advocated for dual-class shares to expire after a period of time. The theory is that the executives of young companies can have more authority over a company when it’s still young, but built-in defenses should fall away as it matures and strengthens.

Yelp Inc. ended its special class of stock in 2016, more than four years after its IPO, thanks to a built-in kill switch that flipped when special shares held by the CEO and other insiders fell below 10 percent of all Yelp stock. The company also had provisions that would have ended the supervoting shares seven years after its IPO. This multitrigger sunset clause should be a model for every young tech company.

There has already been some backlash in capital markets against perpetual founder power. The overseer of the S&P 500 Index said recently that it wouldn’t permit companies with dual-class shares to join. That’s a good idea. Boards of private tech startups should also show the tiniest glimmer of backbone by forcing their young charges to adopt a sunset provision for supersized voting shares. It’s not a panacea to prevent startup disasters, but it’s a good start.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.