Opec and Russia Best Not Poke the Shale Oil Bear

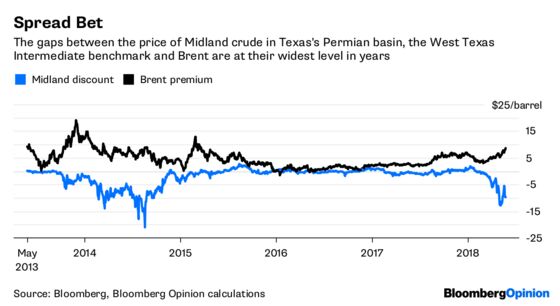

(Bloomberg Opinion) -- Here’s one underreported factor that may explain Russian and Saudi Arabian willingness to turn their backs on almost 18 months of Opec oil supply cuts — the spread between Brent crude and West Texas Intermediate has reached its widest level in three years:

The simple reason for this is that the shale oil boom has left crude sloshing around the U.S., resulting in a local oversupply. While Brent prices have risen some 14 percent over the past three months, WTI is up just 7.5 percent and Midland crude — the version of WTI priced in the booming Permian basin rather than the benchmark delivery point in Cushing, Oklahoma — is down 4.8 percent.

The last time we saw these sorts of spreads, there were sound legal reasons for it. The U.S. had forbidden almost all exports of crude oil for four decades until the end of 2015, so for many years its soaring shale oil production was trapped by the ban and the capacity limits of U.S. refineries that were able to convert it into exportable products.

The growing spreads now suggest that supply is pushing up against a different sort of bottleneck: a shortage of pipeline capacity between Midland and Cushing, and then a further shortage of pipeline and port capacity to get U.S. crude onto a hungry global market.

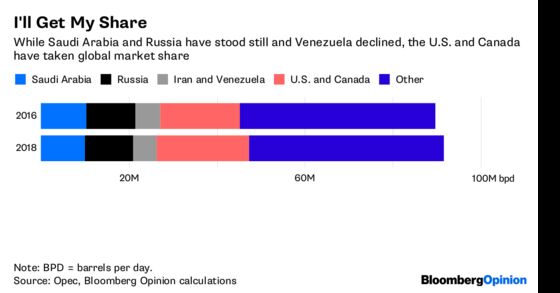

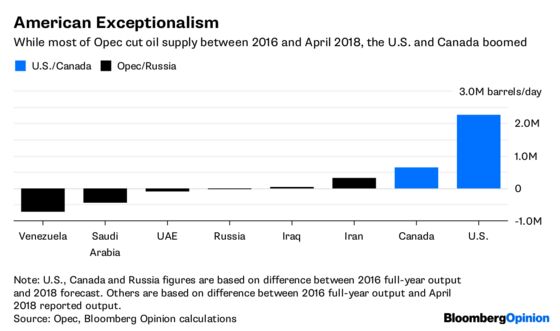

The most straightforward way of looking at the Saudi-Russian plan to lift oil production is that they’re essentially maintaining the status quo. The 713,000 barrel-a-day decline in Opec’s total supply between 2016 and last month can be accounted for almost entirely by the decline in Venezuelan output, which has fallen by about one-third — 718,000 barrels a day — over the period.

A further shoe may be about to drop, though: Iran, which added 308,000 barrels over the same period, is facing the prospect of U.S. and global sanctions that could sharply trim its output. A reversal of the 487,000 barrel-a-day cut by Saudi Arabia and Russia would help plug that looming hole in production.

There’s a further factor to consider, though, and it relates to what’s happening on the plains of Texas and Oklahoma. The latest period of supply restraint from Opec and Russia has in essence seen them give up market share to onshore North America. The 1.8 million barrels a day that they’ve taken off the market is almost entirely compensated for by the 1.53 million barrels a day of additional unconventional crude production from the U.S., not to mention 640,000 of additional daily barrels that have come out of Canada.

At the moment, infrastructure bottlenecks are keeping the U.S. shale boom almost as quarantined from global markets as legal restrictions did in the pre-2016 era. But, as my colleague Liam Denning has written, those widening spreads between delivery locations are driving midstream operators to seek profit from new export channels, from pipelines to the nascent capacity to load larger tankers from Louisiana’s Loop terminal.

Those constraints will take years to fix, but in the meantime one way to close those tempting spreads and nip such investments in the bud would be to dump some more oil in the non-U.S. market commensurate with the amount coming out of the Permian.

The potential of U.S. exports is a sleeping bear that could eventually menace the current bull market in crude. Opec and Russia would be wise not to poke it.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

©2018 Bloomberg L.P.