Beijing’s Foxconn Embrace Has Tinge of Desperation

By having state firms buy into the IPO, Foxconn is hoping some Taiwan technology fairy dust will rub off.

(Bloomberg Opinion) -- Just look at that list of investors in Foxconn Industrial Internet Co.’s IPO.

Forget BAT. It was obvious that Baidu Inc., Alibaba Group Holding Ltd. and Tencent Holdings Ltd. would take minor stakes in the Foxconn Technology Group affiliate’s blockbuster Shanghai listing. Those three are in the bottom tier of cornerstone buyers anyway.

Leading the lineup is the Shanghai State Development & Investment Corp., which is subscribing for 73 million shares, or 3.7 percent of those expected to be sold. Central Huijin Investment Co., China Railway Investment Co., China Structural Reform Fund and China Life Insurance Co. round out the top five.

Note the pattern: All are state-owned enterprises. In fact, the list of 20 strategic placements is dominated by state-affiliated investors. The top 14 have shorter lockup periods – half of the shares can be sold after 12 months, half at 18 months. Those lower on the totem pole, like Shanghai Oriental Pearl Group Co. and the BAT collective, are stuck for 36 months.

I don’t imagine Foxconn boss Terry Gou had a lot of choice in the allocation, but he’s a savvy political operator and would probably have come up with a similar list himself.

This isn’t so much a case of companies being called in for national service – Taipei-based Foxconn and its FII listing would have done just fine without state help – as ensuring Chinese flag bearers join the spoils, and maybe even learn a thing or two about the business of technology.

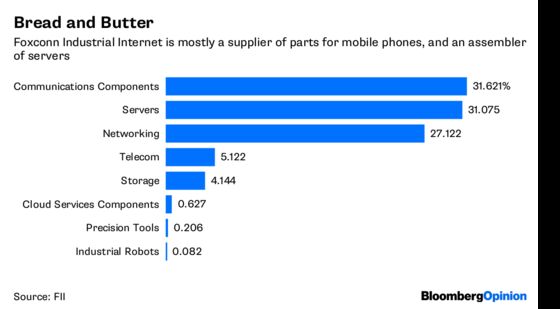

Foxconn is pitching FII as a leading-edge company at the forefront of future trends. In reality, it’s a more mundane manufacturer whose bread and butter is making metal iPhone casings and internal frames, while industrial robots barely show up in its revenue data.

Nevertheless, maybe just standing close to a Foxconn unit will allow SOEs to be sprinkled with some of that high-tech fairy dust. It does make Apple Inc. phones, after all, not to mention supplying to Amazon.com Inc. and Cisco Systems Inc.

China needs a few more hardware heroes, so co-opting one from across the Taiwan Strait plays well into two core Xi Jinping policies: building technological capability, and limiting Taiwan’s independence.

The billions of dollars China has thrown at the technology hardware industry – notably semiconductors – has done little to dent the dominance of U.S., Japanese, Korean and Taiwanese companies. Huawei Technologies Co. is a notable exception, while the case of ZTE Corp. – whose survival was threatened by a ban on buying U.S. components – merely highlights the gap.

Foxconn’s Hon Hai Precision Industry Co. is Taiwan’s second-largest company, behind Taiwan Semiconductor Manufacturing Co. Luring FII to list in Shanghai, with a Shenzhen domicile, is a great coup for China. It allows Beijing to claim FII as a Chinese company – not unlike the approach taken to Taiwan as a whole.

Cries of hollowing out are a little overplayed: Taiwan gave up on manufacturing decades ago. China may assemble most electronics devices, but don’t forget that all of Apple’s assemblers are Taiwanese companies with Taiwanese executives dominating the top layers of management.

FII shows the closest Beijing can get to matching Taiwan in technology is to buy into a rare mainland IPO and hope to find some leverage, while picking up some business tips along the way. Dealing with Terry Gou though, it may learn that you can’t outfox the Fox.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

©2018 Bloomberg L.P.