Emerging Markets Have an Overlooked Strength

(Bloomberg Opinion) -- There’s a chorus of talking heads predicting a crisis in emerging markets, some quite stridently. Nobel Prize-winning economist Paul Krugman went so far as to say the current slump bears some resemblance to the Asian financial crisis in the late 1990s that roiled global markets.

If that sounds familiar, it should. Plenty of smart people said the same thing back in late 2014 and 2015, when the MSCI EM Currency Index tumbled 15 percent as the Bloomberg Dollar Spot Index soared 22 percent. Then, as now, the fear was that the stronger greenback would make it impossible for borrowers in emerging markets to pay back the trillions of debt they borrowed in dollars, sparking mass defaults and triggering a global crisis.

But that never happened. In fact, emerging markets rebounded, with the currency index going on to soar 20 percent from its low at the end of 2015 to the highs it set earlier this year. Emerging market stocks and bonds followed a similar path. It was just last month that investors were referring to EM assets as “havens” amid the trade and geopolitical turmoil in developed markets. Although it's unlikely that emerging markets will rebound as strongly as they did after the last downturn, the current slump is likely to blow over without inflicting too much damage.

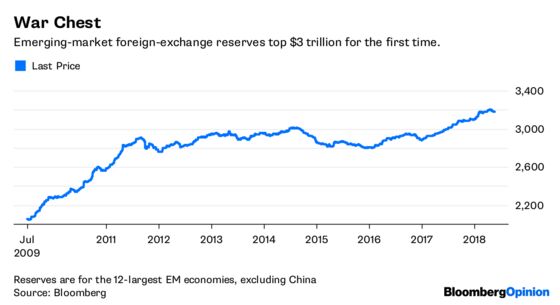

For one, the slump isn’t nearly as bad. The MSCI EM Currency Index has only declined 3.12 percent from its peak this year on April 3, while the Bloomberg Dollar Spot Index has only increased 4.50 percent starting its move in mid-April. Second, developing-nation economies are in a better position than ever to defend their currencies. Foreign-exchange reserves for the 12 largest EM economies excluding China topped $3.2 trillion for the first time in April, rising from about $2.85 trillion at the end of 2014 and less than $2 trillion in 2009, according to data compiled by Bloomberg.

Yes, emerging markets have borrowed heavily following the financial crisis. The Institute of International Finance in Washington estimates that total EM debt rose to $63.4 trillion last year, or 210 percent of GDP, from $21 trillion, or 145 percent, in 2007. Borrowings in non-local debt markets are much less, at $8.3 trillion.

But here’s the rub: Many companies that sold dollar-denominated debt are exporters that receive foreign-currency revenue in exchange for their goods, creating a natural hedge against local currency fluctuations. With weaker exchange rates, these borrowers’ incomes rise when converting the dollars they earned into local currencies, offsetting the rise in debt costs. That’s largely why EM came through the 2014-2015 collapse relatively unscathed, firms including Barclays Plc and Goldman Sachs Asset Management said at the time.

Many borrowers that don’t have overseas revenue often buy currency hedges in the derivatives market to protect themselves. The latest triennial survey of the foreign-exchange market conducted by the Bank for International Settlements in 2016 found that the daily turnover of currency swaps had climbed 6 percent to $2.4 trillion from three years earlier. Among dealers based in emerging markets, currency derivatives accounted for the majority of their outstanding notional positions, in some cases over 80 percent, compared with 10 percent to 20 percent for dealers in advanced economies, according to the BIS.

This doesn’t mean there’s nothing at all to worry about. From Turkey to Argentina, and from Brazil to Indonesia, it’s hard to find an emerging market that doesn’t have a lot of question marks, especially when it comes to politics. Also, there seems to be a perennial concern about high leverage levels among Chinese companies. In addition, the IIF says refinancing risk is approaching a peak, with $2.9 trillion of emerging-market bonds and syndicated loans come due through the end-2019. But these concerns are always hanging around, which is why investors demand a premium to own emerging-market assets.

Don’t forget that emerging markets are highly correlated to the market for raw materials, which are breaking out to the upside. The Bloomberg Commodity Index jumped this month to its highest level since 2015. And in April, the International Monetary Fund said it expects emerging-market economies to expand 4.9 percent this year and 5.1 percent in 2019, while developed-nation economy growth rates decelerate from 2.5 percent this year to 2.2 percent in 2019.

That’s not to say investors shouldn’t be on their guards. Market crises often have a way of becoming self-fulfilling prophecies. Keeping a close eye on non-resident portfolio flows is key in this environment to see which markets may have trouble accessing capital. Emerging-market kingpin Mark Mobius perhaps said it best when he told Bloomberg TV that although “we still could have some downside in the emerging markets,” realize that “selectively, you have some good opportunities.”

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.