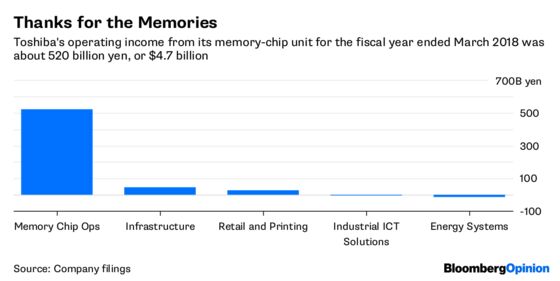

(Bloomberg Opinion) -- Toshiba Corp. shareholders may soon see a windfall from the electronics giant’s $18 billion chip sale, but they’re also faced with an unappealing prospect.

The 143-year-old company’s loss of its crown jewel means it must find a new source of growth, and must do so with a board stacked with salarymen who hold too little stock to care deeply about Toshiba’s direction.

Once the sale is complete, expected June 1, Toshiba will be left with a 40.2 percent stake in the memory-chip unit. Hoya Corp. will have an almost 10 percent interest, with the remainder held by foreigners including Bain Capital, SK Hynix Inc. and Apple Inc.

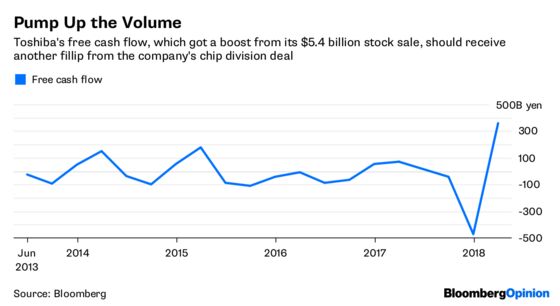

Fresh from a more than $5 billion stock sale and the divestment of its troubled nuclear arm, Toshiba may look like it’s found its way out of trouble.

But while it’s true competitors in China are doubling down on semiconductors, and Bain will probably be more effective at cutting costs, Toshiba must still work on finding a new direction.

It could bulk up in areas such as air conditioners and elevators, but there, it lacks scale. Newer sectors like lithium-ion batteries and logistics robotics, although promising, are years away from making any money.

There’s also more to do on the management front.

In February, Toshiba brought in the representative director of CVC Capital Partners Ltd. in Japan, Nobuaki Kurumatani, to replace CEO and 40-year veteran Satoshi Tsunakawa, who effective April 1 became the company’s chief operating officer.

As a former vice president of Sumitomo Mitsui Banking Corp., Kurumatani has arguably had more experience in public relations and dealing with regulatory authorities than running a business.

Jefferies Japan Ltd. analyst Zuhair Khan also says Toshiba’s board isn’t aligned with shareholder interests. “One factor for all the companies that have had scandals is that they score in the bottom 10 to 20 percent for shareholder alignment, i.e. the board members don’t own shares,” he said. With Toshiba board members since 2017 owning even fewer shares than the low level of the previous board, the concern about potential future scandals remains.

Tsunakawa, for example, owns about 72,000 Toshiba shares, which at a stock price of 304 yen are worth about 22 million yen ($198,100). The median share ownership of CEOs of Topix 500 companies is 65 million yen, while the top 25 percent hold a minimum 199 million yen of stock. Considering Tsunakawa joined the company in 1979, he doesn’t have many excuses.

If the parallel holds, Toshiba may need to be as attentive to avoiding another accounting scandal as to finding new sources of growth.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.