Companies Pay the Price for Ignoring Blankfein’s Debt Advice

They loaded up on borrowing but didn’t lock in for longer periods, and stock investors will take notice.

(Bloomberg Opinion) -- In late 2012, Goldman Sachs CEO Lloyd Blankfein advised corporate clients to watch out for the bond market.

There was a general complacency, he said, about low interest rates that was creating a risk that corporations would get caught behind the curve when they eventually did rise. He instructed corporate America to borrow as much as it could for as long as it could. It’s not clear how many executives took his advice.

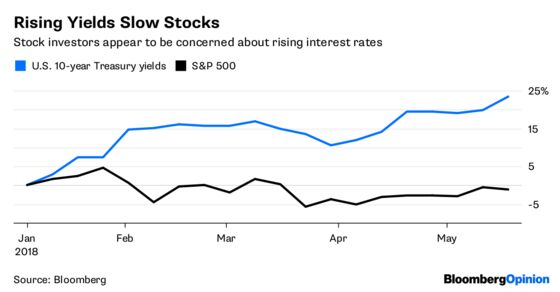

Corporate America has certainly borrowed a lot. But seven years later, few companies have followed Blankfein’s second piece of advice, to lock in low rates for as long as possible, and that is whipping up a headwind for stocks.

As of the end of the first quarter, the median company in the S&P 500 will have to pay back its debt in 97 months, or just more than eight years. That’s roughly the same time to maturity that the median S&P 500 company had when Blankfein made his comments in 2012. Now that interest rates are finally rising, some companies, and their investors, will perhaps wish that they taken the opportunity to lock in low rates for longer.

In fact, some companies have done the opposite — taken out shorter debt — which has temporarily lowered their borrowing costs but might set them up for a bigger bill when they have to refinance at higher rates in the next few years. For instance, in 2012, industrial equipment maker Pentair Inc. carried debt with an average maturity of about six years. Since then, Pentair has let its debt maturity shrink to just two years. The company has $1 billion in outstanding bonds. The biggest portion of that debt is a $622 million offering that has to be paid back or refinanced by September 2019. The bond, which was issued in 2015, has an interest rate of 2.45 percent. A similar bond issued issued today would have an interest rate closer to 4.5 percent.

In 2012, chipmaker Xilinx Inc. had until 2028 on average to pay back its debt, or 16 years. It has since refinanced, and its $1.75 billion in outstanding bonds now have a weighted average maturity of just less than four years. The first of three bonds, a $500 million deal that was issued in 2014 with an interest rate of 2.13 percent, comes due in March. In 2012, retailer The Gap Inc. had one $1.25 bond deal outstanding. It still has the same one outstanding, but its 2021 maturity is now less than three years away.

In all, 40 companies in the S&P 500 have debt that will on average have to be paid off or refinanced within four years. And 87 companies have debt that will on average mature within the next five years.

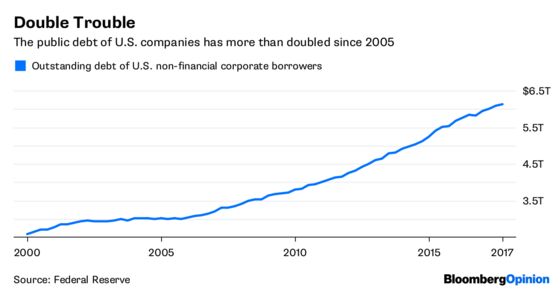

Rates have been rising over the past few months after a historically long low period. Investors for the first time in years are worried about rising interest costs. Most strategists believe public companies, despite having nearly doubled their amount of debt in just a few years, are not overleveraged and have the cash flow to service their debt even as rates rise. What’s more, most of that debt is still fixed, and with eight years to go, on average, the refinancing bill will be gradual. Despite rising yields, most companies have yet to experience higher interest costs.

Still, some companies will feel the pinch of higher rates quicker than others. And at a time of possible rising inflation and wage pressures, borrowing costs are another drag on stocks.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.