(Bloomberg Opinion) -- The stronger dollar may have taken its toll on Turkey and Argentina but there is one notable exception to the stresses plaguing emerging markets — Russia.

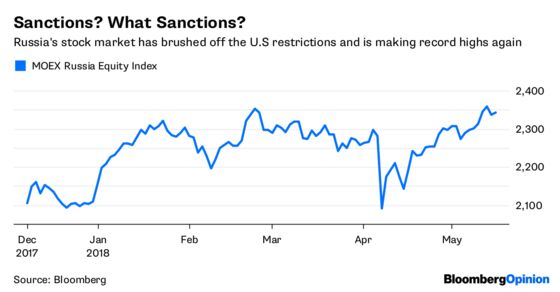

Investors have largely shrugged off the shock from U.S. Treasury sanctions being imposed for the first time on specific Russian companies, notably aluminum producer United Co. Rusal. The MOEX Russia Index, the country’s benchmark, just hit a record high.

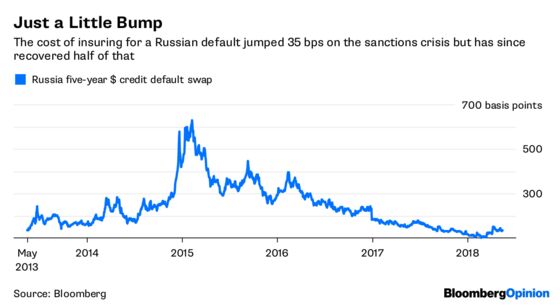

The creditworthiness of Russia took a knock, but in the greater scheme of things it is just a blip. S&P Global Ratings in February lifted the sovereign back into investment grade, at BBB-, and it has not revised its view since. Moody’s Investors Service, which has a Ba1 rating with a positive outlook, said April 19 that Russia’s economy can weather the new sanctions.

Another Moody’s report on Wednesday said Russian corporate liquidity “remains strong.” Economic stability, higher oil and commodity prices, lower interest rates and the weaker ruble all contributed to a broad picture of corporate health.

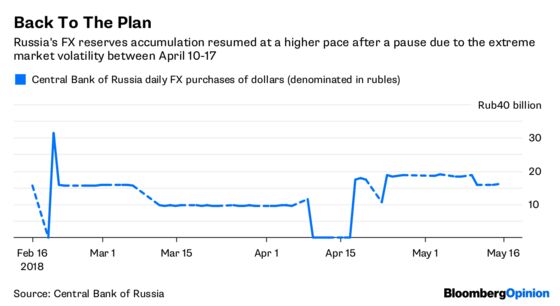

Central Bank of Russia Governor Elvira Nabiullina said soon after the U.S. announced sanctions that “systemic measures” weren’t needed to support the ruble, and she was right. Though the Russian currency has not recovered much from its sharp selloff, it has at least stabilized. And that has enabled the CBR to resume its normal practice of buying about $200 million a day in dollars to rebuild its currency reserves.

It is not all sunshine and roses. Russia has yet to respond to the American measures in a meaningful way, and there’s scope for President Vladimir Putin to escalate tensions. There is still a bill rumbling through nation’s parliament, the Duma, which would impose counter-sanctions on Western countries and companies. Though some of the more extreme elements have already been watered down, officials could ratchet them back up.

The U.S. Treasury could also opt for a wide interpretation of sanctions violations that would catch parties not named in its April statement, such as banks. As I have argued, it’s easy to see how the taint of the new edict can spread. So far this hasn’t happened, but it can’t be ruled out.

Russia’s economy grew 1.3 percent in the first quarter, at the low end of the central bank’s forecasts. It’s not a disaster — it’s up from 0.9 percent in the fourth quarter, and in line with the slower pace of expansion seen in Europe. The sanctions came at the start of the current period, but that doesn’t need to imply a slower pace of growth, as some analysts argue. The oil price rise will take a lot, perhaps all, of the sting out of their impact.

The Russian economy has come a long way. Inflation and interest rates were both at 17 percent three years ago, and they’re now at 2.4 percent and 7.25 percent. The CBR had forecast rates to become neutral this year, which it says is toward the upper end of its 6-7 percent range, but it is now a crossroads. The weaker ruble looks to have stayed its hand from further reductions at its April 27 meeting, and it could also hold steady at its June 15 policy decision.

That shouldn’t bother stock markets. It’s more complicated for fixed income. The central bank’s expectations for its key rate didn’t account for the drop in the ruble and the gain in oil. And these factors, and the surprising strength of wage growth, look likely to stoke a probable rebound in inflation. This is a problem the bank can set aside for now.

Most of the world has been throwing rocks at Russia for months now. Its markets seem largely immune, and if politics remain as — relatively — peaceful and calm as this, stocks can keep climbing. With a price to earnings ratio of 8.6 percent, on a value basis, the MOEX Russia Index looks hard to beat.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

©2018 Bloomberg L.P.