Elliott and the Art of Nonsense Hyundai Numbers

(Bloomberg Opinion) -- More often than not, beauty is in the eye of the beholder where valuations are concerned.

As Paul Singer’s activist investment firm Elliot Management Corp. circles Hyundai Motor Group, proxy advisory firms Glass Lewis & Co. and Institutional Shareholder Services Inc. have urged investors to vote against a restructuring plan put forward by the South Korean conglomerate. Glass Lewis said a planned spin-off and merger between two Hyundai units has “questionable business logic,” undervalues assets, and appears designed to benefit the founding family. ISS said the board had failed to articulate a clear business rationale for the transaction.

Elliott, responding to the chaebol’s underwhelming March proposal, has called on Hyundai to establish an efficient holding company structure, cancel treasury shares, and return more than 12 trillion won ($11.2 billion) of cash to shareholders. The firm has accumulated stakes of more than 1.5 percent each in Hyundai Mobis Co., Hyundai Motor Co. and Kia Motors Corp. Mobis shares have lost about 9 percent since the proposal to separate the company’s after-service parts business and merge it with Hyundai Glovis Co., a logistics provider.

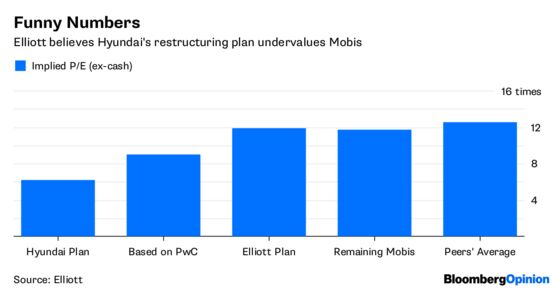

The disappointment stems from how Hyundai is valuing its assets. Elliott and others have said the plan doesn’t make sense. A point of contention is the spin-off and merger ratio — how many of its shares the acquirer offers in exchange for those of the target. The spin-off ratio looks like it has been engineered to diminish the value of highly profitable Mobis, which ultimately translates into a richer valuation for the post-merger entity.

That’s a win for Hyundai’s Chung family at the cost of Mobis shareholders, who will own 61.5 percent of the post-merger Glovis. Family shareholders currently hold a cumulative 7 percent stake in Mobis — that will rise to 30.2 percent after the deal. Mobis will retain 66 percent of its pre-transaction revenue.

Hyundai has laid out how it arrives at its numbers, but that’s only left investors with more questions. The company used a discounted cash flow model — a standard corporate finance tool — to justify the equity value of the spun-off Mobis business. This calculates the present value of future free cash flows, reflecting the principle that money to be received years from now is worth less than what’s already in hand.

Since you can’t forecast a company’s performance forever, the model estimates a terminal value after which cash flows are assumed to grow at a constant rate in perpetuity. Hyundai effectively low-balled this number by using a terminal growth rate of 1 percent, based on its reading of the long-term pace of expansion of the Korean economy and the auto industry.

That number is less than inflation, currently running at about 1.6 percent in Korea, let alone the long-term growth rate of the economy, which the International Monetary Fund has estimated at about 2.2 percent by the 2020s. Analysts often use the local 10-year bond yield, currently about 2.8 percent in Korea, as a proxy for the terminal growth rate.

Another key input to a DCF model is the discount rate, or weighted average cost of capital. The higher the rate, the lower the valuation, other things being equal. For instance, Hyundai uses 11.38 percent, the country risk premium for Korea as calculated by Bloomberg, which uses inputs such as sell-side analysts’ often-optimistic forecasts for equities. That’s far higher than risk-premium estimates of valuation guru Aswath Damodaran, a finance professor at New York University.

The use of such tenuous and inconsistent assumptions should cast even more doubt on Hyundai’s willingness to give minority investors a fair deal. Shareholders vote on May 29: The only ones left sitting pretty are likely to be the family, if these numbers are taken at face value.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

©2018 Bloomberg L.P.