Zoom Video Analysts Like Its Growth But Caution on Valuation

Zoom Video Analysts Like Its Growth But Caution on Valuation

(Bloomberg) -- Zoom Video Communications Inc. analysts started coverage on the company on Monday, and while there was unanimous optimism over its growth potential, a number of analysts also said this was already reflected in the surging stock.

Valuation was the key factor holding back some analysts from assigning buy ratings, although others were able to look past the issue. JPMorgan wrote that Zoom’s outlook “provides a foundation for growth and profitability at a scale not seen in software before.” The firm issued a Street-high price target of $113. But in a reflection of the company’s wide expectations, Goldman Sachs -- which wrote that Zoom’s growth prospects were “very attractive” -- has a target below $50.

Currently, there are six buy ratings on Zoom and nine hold ratings. Only one firm recommends selling the stock, according to data compiled by Bloomberg. The average price target is $71, which implies downside of almost 4%.

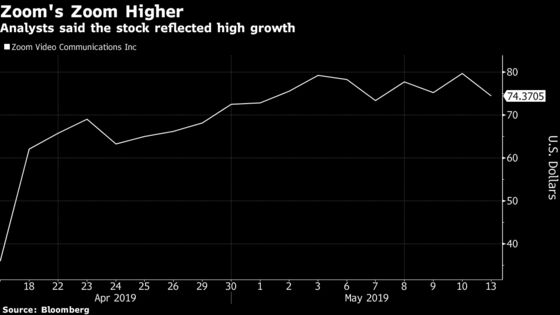

Shares fell as much as 7.8% on Monday, in a broadly negative session for U.S. stocks. The decline comes after it closed at a record on Friday; the stock has more than doubled since it went public.

Here’s what analysts are saying about the company:

JPMorgan, Sterling Auty

While the stock appears expensive, the technology will “will help fundamentally change the way that business is conducted going forward.”

The company’s potential to expand into new businesses “provides a foundation for growth and profitability at a scale not seen in software before.”

Overweight rating, $113 price target. Added to JPMorgan’s Analyst Focus list.

Piper Jaffray, Alex Zukin

Zoom’s “triple digit growth and profitability profile makes the company, in our view, a unicorn among unicorns that should lead to a sustained premium multiple.”

“The brand is becoming synonymous with the mode of communication.”

Overweight rating, $90 price target.

Goldman Sachs, Heather Bellini

Zoom’s growth outlook is “very attractive,” and Goldman’s estimates have the potential “for considerable upside.” However, “this is factored into the valuation at current levels.”

Neutral rating, $47 price target.

KeyBanc Capital Markets, Alex Kurtz

Zoom has generated “best-in-class revenue growth” and free-cash-flow margins compared with its software-as-a-service peers, “yet the growth opportunity is still early.”

But the valuation reflects those bull-case expectations.

Sector weight rating.

Morgan Stanley, Meta Marshall

Zoom “will have success becoming a central unified communications platform, something built into valuation today.”

The company’s financial model is “extremely conservative” as it’s in the early days of new products and its margin profile is “very attractive.”

“Near triple-digit growth” in Zoom’s upcoming fiscal year could support the stock trading towards Morgan Stanley’s bull-case scenario.

Equal-weight, $75 price target

To contact the reporter on this story: Ryan Vlastelica in New York at rvlastelica1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm, Scott Schnipper

©2019 Bloomberg L.P.