Zillow Tumbles as Analysts Trim Targets on Persisting Challenges

Zillow Tumbles as Analysts Trim Targets on Persisting Challenges

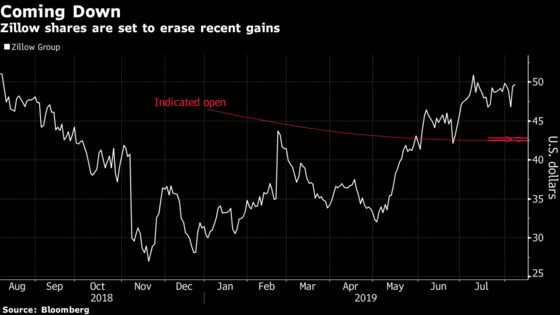

(Bloomberg) -- Zillow Group Inc. shares were poised to fall to a 6-week low after its results and updated forecasts suggested its entire “portfolio is faltering” at a critical time for the company looking to pivot its business, analysts said.

The mixed second-quarter report was headlined by a miss in adjusted earnings before interest, taxes, deprecation and amortization as the online realty platform predicted home-flipping losses. Analysts across Wall Street trimmed their 12-month price targets on the weaker expectations at both the premier agent and homes businesses.

Shares of the company sank 15% to $42.20 in trading before the U.S. market open as the broader market traded higher. The stock hasn't traded below $43 since June 26.

Here’s what analysts are saying about the results:

Susquehanna, Shyam Patil

Key challenges persist as “core IMT performance remains weak, Homes is burning cash at a rapid clip, and now Mortgages is experiencing serious issues… i.e., the entire ZG portfolio is faltering.”

The stock has typically garnered a premium because of secular runway and “supposedly ‘strong competitive positioning,’ but we see that changing.”’

Rates Zillow negative, lowered price target to $25 from $28.

Piper Jaffray, Jason Deleeuw

The second-quarter revenue beat was driven by stronger Homes segment revenue though “profitability was impacted by cost of revenue moving to 97% of revenue vs 95% in the first quarter, primarily due to a valuation adjustment lower to home inventory >60 days.”

“We remain neutral on ZG as we believe the pace and profitability of the Zillow Offers ramp is highly uncertain as iBuying is still a new market segment with numerous competitors competing heavily on price.”

Sees a slower and more volatile Zillow Offers ramp limiting upside scenarios.

Lowers price target to $43 from $48.

Wedbush, Ygal Arounian

Results reinforce view that Zillow’s current pivot has “plenty of bumps” and “is far from a straight path” to a larger market opportunity.

Rates shares at neutral, maintains $39 price target.

Deutsche Bank, Lloyd Walmsley

Weak results in most important core segment “seems unlikely to meaningfully improve through 2020 with a transition to Flex ahead and the associated execution risks.”

Maintains hold rating but cuts price target to $33 from $43.

Benchmark, Daniel Kurnos

“Homes, however, remained a bright spot, even if the increased success continues to drive incremental EBITDA losses.”

Still sees significant runway for Homes business which can more than offset near-term Flex disruption.

Maintains buy rating, raises price target to $55 from $52.

To contact the reporter on this story: Bailey Lipschultz in New York at blipschultz@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Courtney Dentch

©2019 Bloomberg L.P.