The Yield Curve’s Day of Reckoning Is Overblown

The Yield Curve’s Day of Reckoning Is Overblown

(Bloomberg Opinion) -- For having assets totaling more than $3 trillion, the U.S. corporate pension industry does an awfully good job of remaining a mystery to the world’s biggest bond market.

Ask Wall Street strategists about the impact of pension demand on the Treasury market, and a consensus will emerge: It has helped drive the relentless flattening of the yield curve over the past year. Citigroup Inc. estimates that the retirement funds’ purchases alone may have compressed the spread between five- and 30-year Treasuries by as much as 32 basis points since last September. That’s a staggering amount considering that the curve is only 30 basis points from inversion.

There is no agreement, however, about what to expect from pensions in the months ahead. After Sept. 15, companies won’t be able to deduct contributions at the 2017 corporate tax rate of 35 percent; instead, they have to settle for the new 21 percent level. As some tell it, corporations have plowed so much cash into their retirement funds ahead of the deadline to capture the tax advantage that purchases of long-dated Treasuries are destined to dry up. That would end the curve-flattening trend that’s captivated investors and Federal Reserve officials alike.

I’m not so sure Sept. 15 is the day of reckoning for the flattening yield curve, though. And neither are strategists at BMO Capital Markets, Citigroup, Morgan Stanley and TD Securities.

The trickiest part in determining whether it’s a make-or-break moment is figuring out how much pensions have thrown their weight around in the Treasury market. Citigroup’s flattening estimate, which strategists cautioned “is necessarily imprecise,” was based on total contributions so far this year of about $150 billion, compared with $146 billion for all of 2017. At a company-specific level, TD Securities noted that Lockheed Martin contributed $3.5 billion to its pension in the first half of 2018, compared with nothing in the period a year earlier. And based on a late 2017 announcement from General Electric, the company still has $5.1 billion of funding on tap before the end of the year.

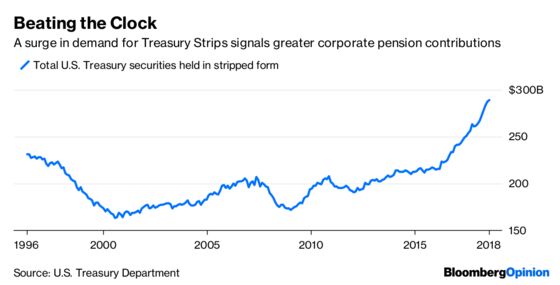

Of course, not all contributions are used to buy long-term bonds. One way to gauge demand is by looking at Treasury Strips, which are long-duration securities broken into their component cash flows. They’ve surged in popularity lately — the market has grown by $26.7 billion in 2018, the most ever for a seven-month stretch, Treasury Department data show. In part because of this, Citigroup concludes that “pension fund demand did exacerbate the recent curve flattening trend meaningfully,” though it doesn’t expect the tax advantage’s expiration to spur much steepening.

Morgan Stanley strategists led by Matthew Hornbach took a stab at sifting through data, including primary dealer positioning, in a Sept. 4 report. Remarkably, they “conclude that the evidence of strong demand from pension funds is weak.” Therefore, they say, Sept. 15 won’t reverse the curve-flattening trend.

By contrast, here’s what NatWest Markets strategists had to say in an Aug. 30 report:

“We think increased demand from pension funds has been a major contributor to the back-end’s outperformance this year … as this window closes on September 15th, we see corporate contributions slowing in Q4 and in turn expect pension fund support for the long-end to dip.”

How can these major Wall Street firms have such different views? For one, it comes back to the lack of precise data on what pensions are doing with their money. But, crucially, Morgan Stanley has been calling for the yield curve to flatten further, and Citigroup is positioned for continued modest curve flattening. NatWest, on the other hand, has been an advocate for steepening.

In other words, Sept. 15 is not necessarily a turning point for the $15.1 trillion Treasuries market but rather a moment to reaffirm views on the yield curve. If you’re a trader who has been waiting all year to time a reversal, then the prospect of a large buyer exiting the market seems like a good time to take the plunge. If you’ve been telling yourself not to fight the flattening, then you’ll point to other reasons pension demand will persist — like costly fees from the Pension Benefit Guaranty Corp. — and this will prove nothing but a bump in the road.

The truth, in all likelihood, falls somewhere in the middle. “It matters, but it isn’t going to turn the tide of the market,” said Ian Lyngen, head of U.S. rates strategy at BMO. Part of the reason the curve from five to 30 years has steepened by the most in months over the past week, he said, may have been people trying to get ahead of trades closer to Sept. 15.

Morgan Stanley says the real risk to the flattening trade could come later this month, when Fed officials update their projected path of interest-rate increases. Indeed, questions abound over how many more times the central bank can hike before it has to pause. For now, short-term yields are the highest they’ve been in about a decade, while the long bond has ample breathing room before testing its crucial 3.22 percent support level.

Traders probably wish Treasuries would break out from their quietest quarter since 1965. They very well still could. Just don’t expect the pension contribution deadline to be the catalyst.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.