The Yield Curve Is Regaining Some Forecasting Powers

The Yield Curve Is Regaining Some Forecasting Powers

(Bloomberg) -- The bond market in the U.S. and U.K. is regaining some of its forecasting mojo, according to a Bank of England blog post.

It says the gap between short- and long-term yields remains a valid indicator for the growth cycle -- but the cherished 10- to two-year gauge may not be best one to watch.

“The yield curve slope appears to have regained some of its predictive power, as policy rate expectations are again positively and significantly associated with future GDP growth while the term premia has stopped obscuring their signal,” according to an article posted on Bank Underground this week.

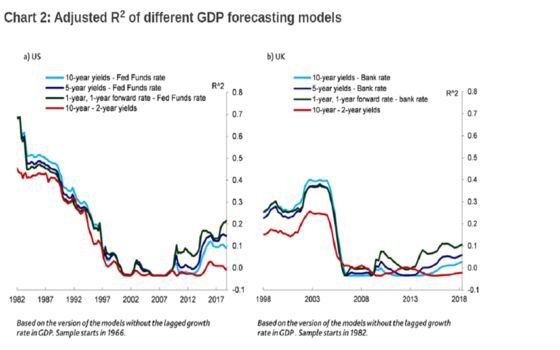

The post doesn’t necessarily represent the view of BOE policy makers. It cites the 10-year yield relative to policy rates -- and right now, the gauge is ringing alarm bells in America and the U.K.

“While the warning sign from the yield curve slope should be taken with caution, it should not be discarded completely,” researchers Carlo Favero, Sebastian Vismara and Iryna Kaminska wrote.

It’s a sobering conclusion. Wall Street pundits warn the risk of a U.S. recession has risen, citing everything from tensions in global commerce and late-cycle excesses to fierce hedging demand for ever-falling bond yields.

The research suggests a shift in term premiums, the relative compensation investors demand for holding longer-term bonds, as one of reasons why the yield curve has probably become more accurate in forecasting growth.

In the early 2000s, the relentless search for safe assets by foreign-official investors became a key factor that flattened the gap between U.S. rates, muddling signals on economic prospects.

The yield curve’s powers of economic prognostication are weaker compared with its storied history, according to the research. But wonks should take note of the forecasting potential flashed in this model by the gap between interest-rate swaps for expected one-year borrowing costs in one year’s time and the policy benchmark.

“Our results show that the policy rate expectations component of the slope tends to be positively correlated with future GDP growth over the whole sample,” the post concluded.

To contact the reporter on this story: Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Anil Varma

©2019 Bloomberg L.P.