XPO’s Buybacks Are Too Much of a Gas Guzzler

XPO's Buybacks Are Too Much of a Gas Guzzler

(Bloomberg Opinion) -- XPO Logistics Inc. may have shipped a bit too much of its cash to shareholders.

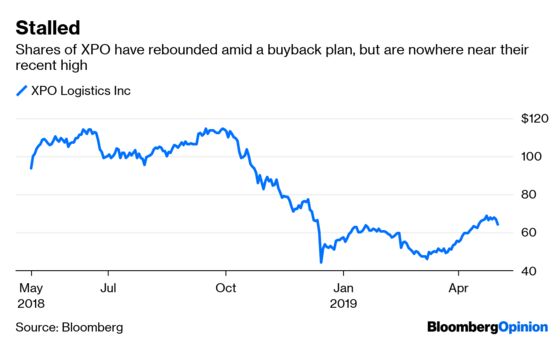

Since mid-December, the warehouse and transportation firm has spent nearly $2 billion purchasing its own shares, taking about a third of its stock off the market. Lowering shares outstanding should in theory raise the value of the remaining stock, which is one reason Wall Street tends to love buybacks. In the case of XPO, the shares did indeed respond, climbing some 26 percent over the past five and a half months. And yet, at $65 a share, the stock is still well below the $115 it traded for back in September, with many fewer shares outstanding. In a market that has been mostly buoyed by buybacks, XPO appears to be one of the few examples of companies whose stock repurchases may end up coming at too high a cost, by putting the squeeze on itself.

Lots of companies buy back their stock, and repurchases are hotter than ever. A study released this week by Moody’s Investors Service showed — as others have before it — that companies have diverted a good deal of the savings they got from last year’s tax cut to buy additional shares. But it was a shift for XPO, which hadn’t been a net buyer of its own stock for years, and has tended to use the bulk of its cash flow for acquisitions. Nonetheless, in February, XPO’s CEO Bradley Jacobs told analysts on a conference call, when asked about the sudden rise in stock purchases, that a swoon in the company’s stock price led him to believe the best investment the company could make would be to snap up its own shares.

There may have been additional incentive: to create a buyback-driven short squeeze, sometimes called an “infinity squeeze.” The idea is to quickly buy back enough stock, forcing short-sellers to pay increasing sums to obtain the shares they need to close out their bets against the company — in effect, to drive away critics and boost the shares at the same time. The most famous example of this is when Porsche in 2008 bought up nearly all the available shares of Volkswagen AG. More recently, the stock price of Restoration Hardware-parent RH more than doubled after the furniture retailer spent $1 billion in less than a year on buybacks, against a backdrop of circling short-sellers. Indeed, XPO’s buybacks started shortly after short-seller Spruce Point Capital Management released a report that claimed the company had “unreliable and dubious financials,” and others also began to pile on with bets against the company’s stock.

The company now has a stock float of about 90 million shares. But about 55 million of those shares are held by two large shareholders as well as index-fund companies Vanguard and Blackrock, none of which are likely to sell quickly. That leaves just 35 million shares available for those betting against the stock to use to cover the nearly 15 million shares that have been borrowed to sell shot, translating into an effective short interest ratio of 43 percent. The average stock in the S&P 500 has a total short interest of just 4 percent, but that’s including all shares, and not adjusting for index funds.

XPO’s buyback plan has only been able to do so much for the shares. The problem could be earnings. Earlier this week, XPO reported that its income, even after adjusting for some restructuring costs, fell 27 percent. Sales were also down. Worse, it piled on an additional $1.5 billion in long-term debt to its finances, bringing the total to $5.4 billion. The company’s tangible book value, or net worth, has sunk to negative $2.8 billion.

Now is exactly the time when XPO could use some cash cushion. The biggest threat is Amazon.com Inc., which is expanding its in-house logistics business, and used to be a customer of XPO, but doesn’t appear to be anymore. Paying down debt, instead of adding to it, in the past quarter likely would have led to a rising bottom line, rather than a dropping one. And while RH’s short squeeze worked, that is in large part because its operations have turned around as well. That’s something XPO still hasn’t figured out.

Buybacks are at an all-time high, and lots of companies these days are leaning on them to keep their stock prices up. If growth continues to downshift, lots more companies may too find out what a gas guzzler they can become.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.