Worst Yet to Come For Junk Debt as Defaults Loom, Goldman Says

Credit has been at the center of the financial market turmoil sparked by the worsening pandemic.

(Bloomberg) -- The worst is likely yet to come for high-yield bonds as more defaults loom, according to Goldman Sachs Group Inc.

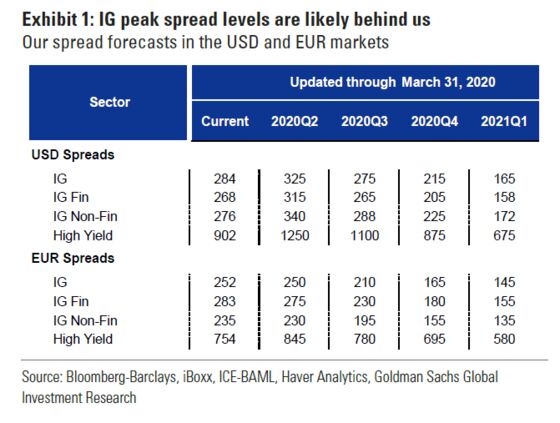

Such debt faces numerous headwinds, analyst Lotfi Karoui wrote in a note dated April 1. That’s even as the Federal Reserve’s unprecedented steps to pump liquidity into a financial system reeling from the coronavirus pandemic mean investment-grade bond spreads have likely already peaked, according to Karoui.

“Despite the strength of the policy support, the cyclical challenges for corporate borrowers remain substantial,” he said. “As has been the case in past downturns, financial distress will continue to increase, leading to higher defaults and downgrades.”

Credit has been at the center of the financial market turmoil sparked by the worsening pandemic, as unprecedented lockdowns and travel bans leave scores of businesses grappling to build out cash buffers. That’s sent the cost of money surging. Average spreads on high-grade dollar bonds jumped 179 basis points in the first quarter, the most ever in a Bloomberg Barclays index going back to 1989.

During 2020, Karoui expects the 12-month trailing default rate to increase to 13%. Over the next six months, he forecasts about $555 billion worth of bonds will likely be cut to high-yield from investment-grade, in addition to the $149 billion that have already been downgraded year-to-date.

©2020 Bloomberg L.P.